Monthly report - Recession Bells & Commodity Shocks: Is the Soft Landing Just a Hoax?

Central banks had a big say in how the economies and financial markets operate for the last year and a half. After a long stretch of loose monetary policy, politicians were shocked by inflation not being transitory, and politicians suddenly started pointing fingers at the central banks. Central banks worldwide made a complete 180 and started with heavy-duty programs and aggressive interest rate hikes.

It seems like we've hit the highest point with rates, inflation has peaked, and maybe we've achieved this without crashing into a recession since unemployment rates are low.

So, time to party? You may want to hold off from popping the champagne bottles.

The Big 5 Central Banks

Each big 5 banks, the Fed, ECB, BoE, BoJ, and PBoC, have unique stories and challenges.

The Federal Reserve, for example, has seen a drop in inflation while the economy stayed strong. But there could be a hiccup in inflation coming, so they might hit the pause button on rate hiking.

On the other hand, the ECB has been more careful about the economy because their previous tightening is doing its job. They've hinted they might pause in September, but they're unsure as they're still wrestling with inflation.

The BoE is stuck between a rock and a hard place. They're trying to bring inflation down without sending the economy into a recession. They've made some progress regarding inflation, but inflation is still too high, so that they might be more aggressive than the Fed or ECB.

Last Friday, the BoJ threw a curveball by deciding to be more flexible with its yield curve control policy. Even though the bank governor insists this doesn't mean they're changing their easy-going monetary policy. It's clear that the days of Japan's super-loose policy are numbered as inflation makes a comeback.

As for the PBoC, they have a new Governor, Pan Gongsheng, who's been warning about a real estate bubble in China since 2014. His appointment signals Beijing's growing worry about a weak recovery and the need for easier money in the next few months alongside additional government spending. Unlike the rest of the world, China is dealing with deflation, especially with producer prices falling rapidly and consumer prices not changing much from last year.

It looks like central banks might have hit the peak of their rate-hiking game, or they're almost there. Even if the Federal Reserve and European Central Bank have made their final rate hikes, don't expect them to send a memo about it.

Polcity makers may choose never to confirm the final rate hikes officially. Central banks might prefer to keep their plans for future monetary policy vague and ambiguous. They can't have too much conviction. Remember BoC? Their hands were forced to continue hiking interest rates after their short break. Given recent inflation surprises and ongoing uncertainty, it is difficult to predict the end of this economic cycle confidently.

The more the market expects easing, the less effective the previous tightening becomes. This might force policymakers to hike rates even further than they'd like. The Bank of England all knows this too well.

Even when Central Banks were hiking rates, they struggled to convince traders they wouldn't jump straight to rate cuts. The markets kept betting on a pivot from the Fed despite Powell's effort to dispel this notion.

Historically, high rates don't stick around long. It makes sense the market was betting on a pivot from that point of view. However, the previous inflation situations from the past are different.

Like the Federal Reserve, ECB officials have been unsuccessful in postponing the market's expectations for a rate cut. Market participants tend to price in rate cuts shortly after the ECB hits the cycle's peak, even if they've slowed their pace.

How can policymakers convince the markets that keeping rates unchanged isn't a signal for immediate rate cuts?

One way to tackle that is by never officially ending the hiking cycle and making traders consider another hike. We probably won't know whether we've seen the last hikes until way later.

In her July press conference, Lagarde of the ECB tried this first. She hinted at a possible hold in September and stressed that each policy decision would be independent of others. That suggests an unchanged rate in September doesn't mean rates won't be hiked later.

Both Lagarde and Powell tried to keep the possibility of rate hikes on the table for each upcoming meeting but haven't managed to change early-2024 rate cut expectations. Even though the market expects ECB rate cuts in the first half of next year, I think that's premature, given the slow disinflation process. Central Banks might have to play it cool for longer.

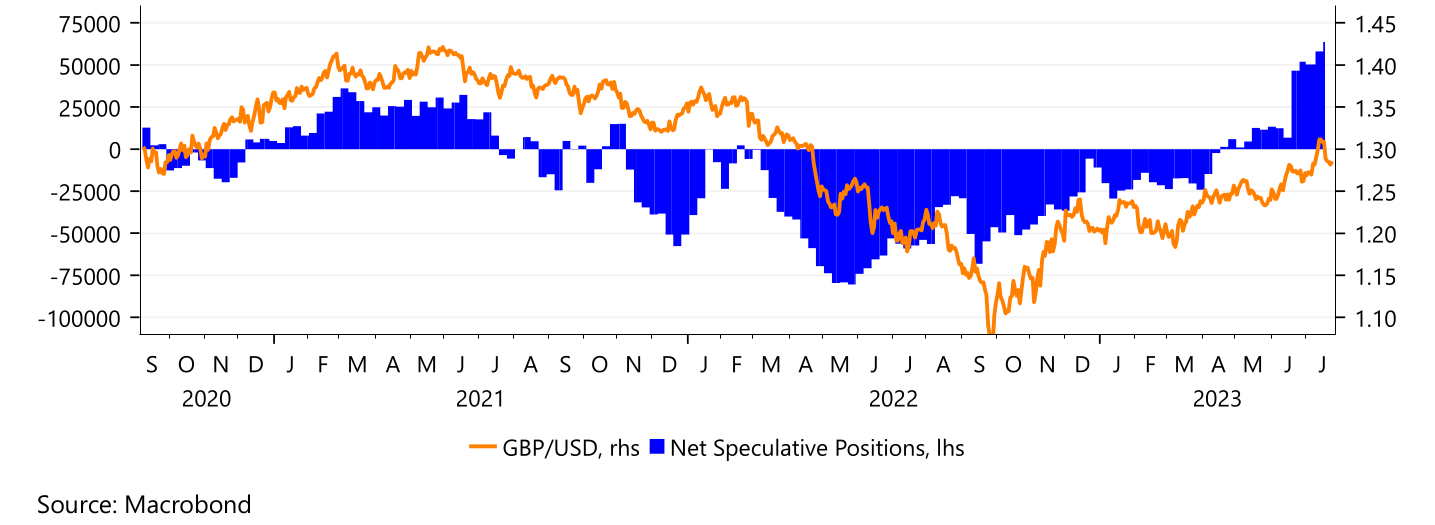

EURUSD

In late July, market participants started to rethink where the US Dollar (DXY) would be heading. Earlier in the month, June's lower-than-expected US inflation number made the dollar dive slightly.

Market participants then thought the Federal Reserve's (Fed) rates might have hit their peak after the expected 0.25 rate hike in July, but recently US economic data has got people questioning.

The possibility of another 25 bps hike rate from the Fed is back on the table, and it looks like the Fed might wait a while before cutting rates to ensure US inflation is truly under control. Other central banks' policy rates are about to hit the peak, and some emerging markets will likely cut their rates before the Federal Reserve does. That makes the dollar a bit better.

In her July press conference, ECB president Lagarde stressed that future policy decisions would depend on the data and be made one meeting at a time. She also hinted at a possible pause in rate hikes come September. The Eurozone has shown some of the challenges the region is facing. Germany's PMI dropped to 48.3, and France's was even lower at 46.6. Both came out lower than expected.

That data and slower credit growth in the Eurozone will likely feed the ECB's concerns. While a lot of expectations around further ECB rate hikes come from persistent core inflation, there are signs that some policymakers think these pressures are easing up.

Recent data shows that net long EUR positions aren't far below their Mat highs. Given the worse economic data, these long EUR positions could be at risk if the ECB takes a more dovish approach. Assuming ECB rates are near the peak. EUR/USD could drop and trade around 1.08 in the next 3 months.

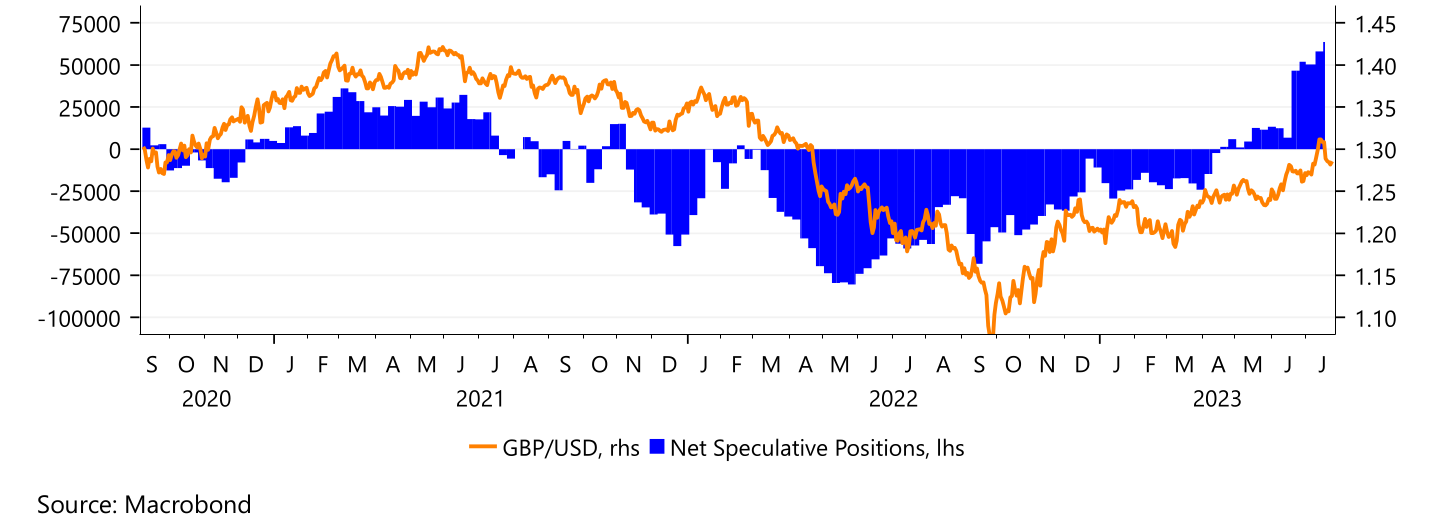

EUR/GBP

Both the Euro and the British Pound currently face balanced risks. There are signs of a potential recession on either side of the English Channel, and the market has long positions in both currencies. These positions were initially established because the UK and Eurozone economies performed better than feared at the end of the previous year.

As energy prices fell from their 2022 highs, Europe's economic obstacles eased, and the markets were encouraged by less negative outlooks. These long positions were extended further this year due to the hawkish tones from both the European Central Bank and the Bank of England.

Recent data suggests that Germany entered a mild recession in the last quarter of 2022. Although the UK has not been affected by an economic downturn, there are signs that economic challenges are rising.

In the July policy meeting, ECB President Lagarde introduced the possibility of a pause in rate hikes at its next decision in September. This prompted the market to reassess its outlook for ECB policy, resulting in an initial dip in EUR/GBP.

Although it's assumed that the BoE has further room to tighten its policy, expectations were tempered by softer-than-expected UK inflation data for June. Despite ongoing high price pressures in the UK, recent comments from BoE Governor Bailey emphasized the Bank's belief that inflation will continue to drop in the coming months.

Year-to-date, the EUR has underperformed the GBP. However, there's been little net movement in EUR/GBP compared to late last year. Fears that the UK economy could be pushed into recession due to tighter monetary policy suggest there's room for the market to reduce its long GBP positions in the coming months.

Simultaneously, the headwinds facing the Eurozone imply that long positions in the EUR may also be unwound. We might see both currencies lose some ground against the USD in the coming months and for EUR/GBP to remain close to the defined activity ranges this year. We predict that GBP/USD will fall back to 1.26 over a 3-month horizon.

Are you a premium member of the newsletter but still didn't join Discord? (Also article does not end here)

Join Discord to get the full value out of the newsletter. There's no extra cost associated with Discord. It's included. All service ;)

Yes, options data such as dark pools, unusual flow, etc, are also included.

Agricultural Commodity

The agricultural market has been experiencing volatility. The S&P GSCI Agriculture index jumped over 8% in July due to geopolitical complications and changing weather conditions.

The cancellation of the Black Sea Grain Initiative and subsequent Russian missile attacks on the port of Odessa and the Dunabe River (the only alternative waterway) brought geopolitics to the forefront. This led to the surge of wheat futures, which have found strong support thanks to the uncertainties.

On top of these geopolitical developments, adverse weather conditions have further impacted agricultural yields. Earlier in the month, extreme heat and dryness in the US, followed by late rains, have likely failed to improve disappointing soy and corn yields. Additionally, a severe drought is ongoing in Southern Europe, raising concerns for Grain and Oilseeds (G&O) production in the region.

For commodities such as sugar, cocoa, and robusta coffee, the El Niño weather stays important to watch. It's especially important for sugar production in Thailand, cocoa production in West Africa, and robusta production in Southeast Asia.

These supply-side concerns are having a widespread impact on agricultural commodities, with many prices increasing along their futures curve. We could continue to see persistent food inflation, adding to the already elevated global inflationary pressures.

Corn Prices & Supply-Demand Dynamics

Last month, corn prices in the Chicago Board of Trade (CBOT) hit a 21-month low at $4.81 per bushel.

Why? It was mainly due to the U.S. Department of Agriculture announcing the third-largest corn planting in U.S. history, which happened just as rain was helping to replenish Midwest soils. Buyers jumped on these lower prices.

Things took a turn with Russia's aggressive actions in Ukraine. Russia blocked the major grain trade route and bombed a key grain infrastructure around the Black Sea and the Danube River. The Danube River was a sort of backup route, so this was a major blow. Goods are still getting through on the Danube, but it's still more costlier and riskier.

With Ukraine isolated, the usual harvest pressures from this typically affordable source is missing. The situation has pushed demand towards other, pricier suppliers like the U.S., which has helped push CBOT corn prices above their 100-day average to $5.48. We will most likely see higher prices if we have to account for ongoing supply issues across the grain and oilseed market.

In the medium term, the impact of Russia's actions on Ukrainian farmers could seriously limit Ukraine in the agricultural world. Meanwhile, hot weather is making a comeback in the Midwest. While the U.S. has more corn fields to help offset lower yields, the redirected demand from Ukraine further reduces the U.S. ending stockpiles from 2.3 billion bushels to 1.8 billion.

Despite a 30% year-over-year improvement and rainfall helping to stabilize yields, I don't expect corn prices to shoot over $6 per bushel. Still, with Ukraine and Argentina largely out of the picture, producers' costs rising, high soy and wheat ratios, and expecting declines in U.S. acreage/hectare in 2024, prices under $5 per bushel are looking increasingly unlikely.

Brent Crude Oil

Brent crude oil had quite the month in July, climbing from $74 per barrel all the way up to $85. This price jump came from Russia cutting back on exports to Saudi Arabia, trimming all their oil production. Still, I don't think the price is going to burst out of its range of $72 - $88 per barrel yet.

What's interesting is the strengthening of "crack spreads"

Now you may be wondering what "crack spread" is. It's basically the difference between the buying cost of crude oil and the selling price of the final products, such as gasoline and diesel. There has been a significant increase in the crack spread for RBOB gasoline due to a production mismatch with the total demand and exports.

Although there was a decrease in demand in July, the low inventories of gasoline at a five-year low and diesel at a multi-decade rock-bottom level have helped maintain prices for refined products. Add to this mix a hike in jet fuel demand, mostly driven by China's international travel sector.

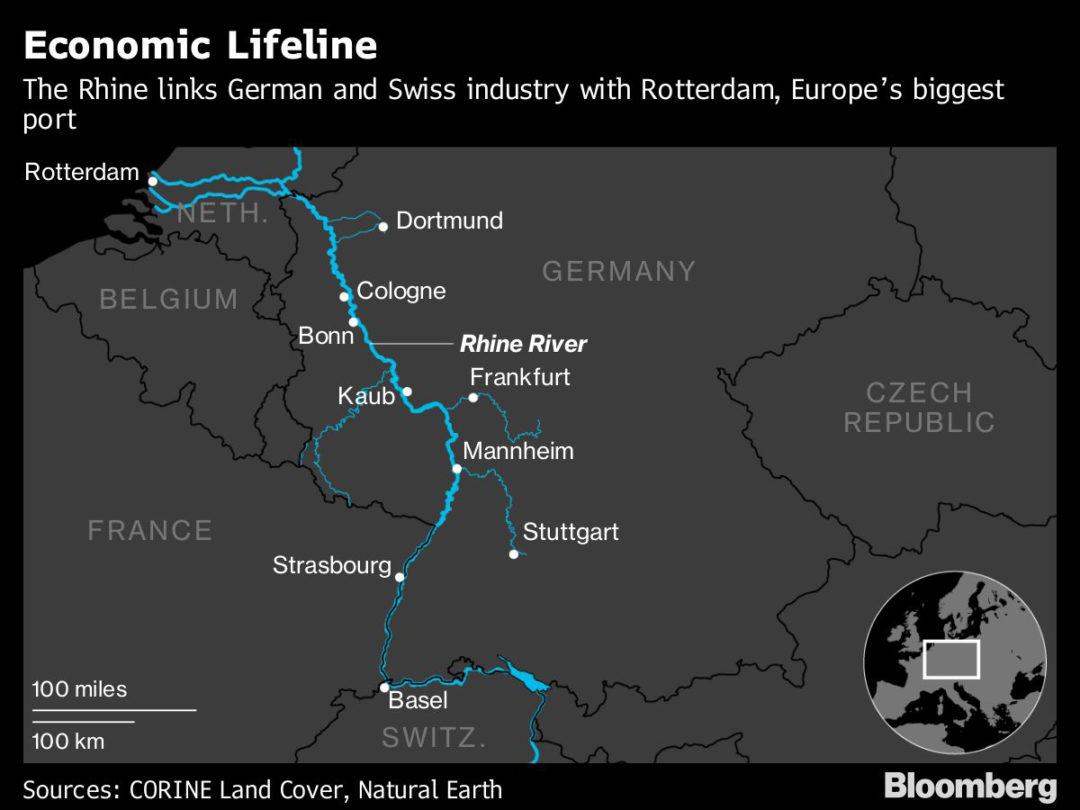

There's more. Due to the hot summer heat reducing shipping capacity along the Rhine River, European refineries might need to cut back production. This could prompt the U.S. to ramp up the export of key industrial fuels.

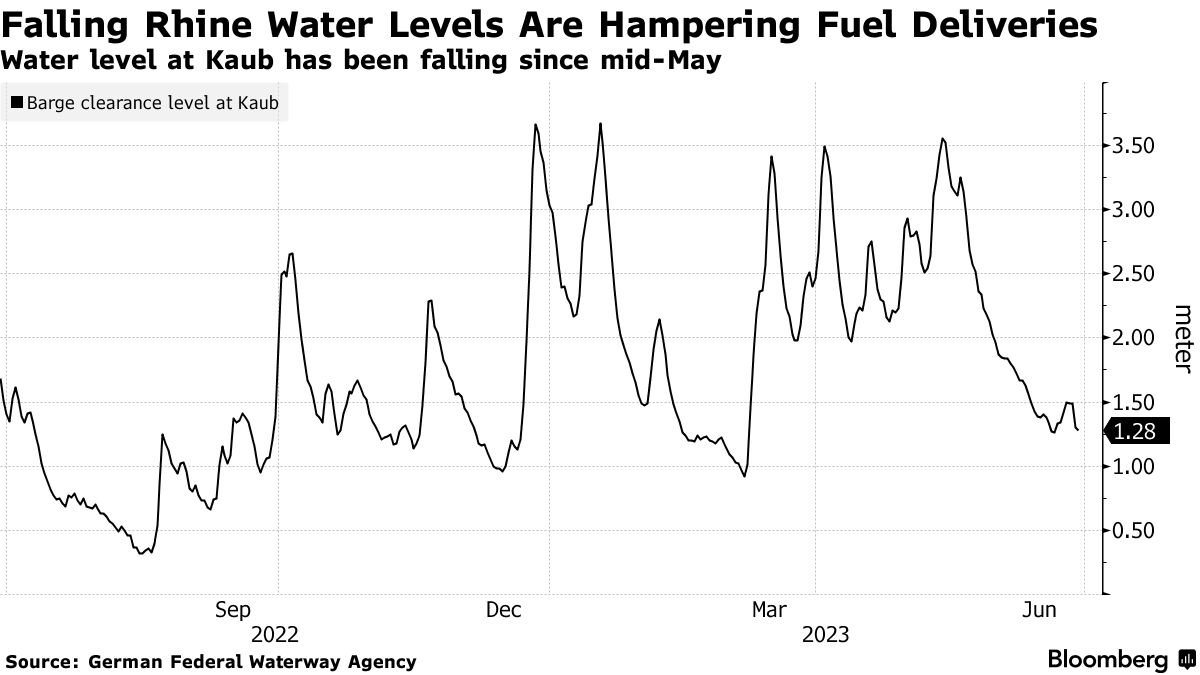

Okay, a quick run on the Rhine River (I tweeted about this before a month ago)

The Rhine River in Europe, vital for transporting fuel & goods, is running into some trouble. Water levels in a part of the river (Kaub chokepoint) are the lowest they've been in 30 years. That's not good because if the water's too low, the big boats (barges) can't get through.

Low water levels halted the barges last summer & may happen again without adequate rainfall. This impacts the delivery of critical goods (heating oil fuel)

Barges moving heating oil fuel from Rotterdam saw their cargo loads nearly cut in half from 2000 to 1200 tons within a week. Less water and harder access mean using barges is getting more expensive.

So a river that's too dry for boats to pass through properly could cause many problems with getting goods around Europe & might even make things more expensive. The inflation battle isn't over in Europe.

Now for those keeping an eye on inflation. As gasoline prices rise in tandem with crude oil, it inevitably drives up the price of pretty much everything. Diesel demand reflects the overall economy's well-being but has fluctuated throughout this year.

If there continues to be poor economic data from the US, China, and the EU, we could very well be starring down the barrel of a recession (pun intended ).

This is why limit the current price ceiling to the high $80s for crude oil.

The strength of crude has reached the upper limit of our forecast range and is still within the range of $72 to $87.

If it breaches $88, it may reach $95 and have a greater impact on refined products. However, concerns about a recession will likely keep a limit on the price for now.

The long-term impact of refinery shutdowns over the past 3 years and the current state of inventories is worth noting. If a recession hits and refinery runs dip, rebuilding inventories will be a severe challenge unless demand drops off a cliff.

There's a catch-22; central banks are trying to cause that drop by hiking interest rates. The downside is that these higher rates can deter drilling and exploration for new oil and gas, further compounding the problem down the line.

This is a vicious cycle. Destroying your economy to tackle inflation is like cutting off your arm because a paper cut is not something I would recommend.

I expect Brent will trade between $72 and $88 per barrel until Q4. After that, don't be surprised if it creeps close to the $90 mark.

Before continuing to read, subscribe to the premium newsletter. The premium package also includes full access to my Discord.

Anyways you can continue to read further. The article does NOT stop here.

Bitcoin

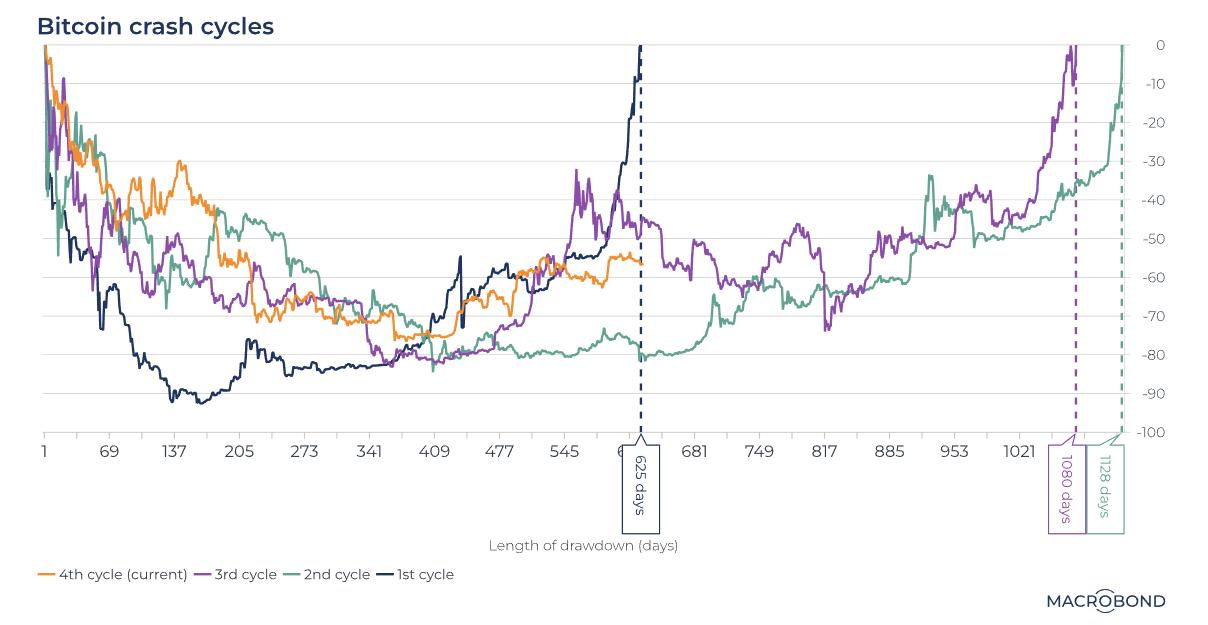

Since 2011, Bitcoin's been on four big dips, or "crashes," as we call them: in 2011, 2013, 2017, and 2021. Each of these rides down and up again varied in length and intensity. The 2011 ride (shown in blue) was the most intense.

It went down the steepest but also shot back up the quickest – taking about 625 days to get back to the top. If we look at the current situation (post-2021, shown in orange), we've just hit that 625-day mark.

But history shows we might be on this ride for a bit longer. If we follow the pattern of the 2013 and 2017 crashes, it might take 2 years to reach those heights again.

Is a recession on the cards?

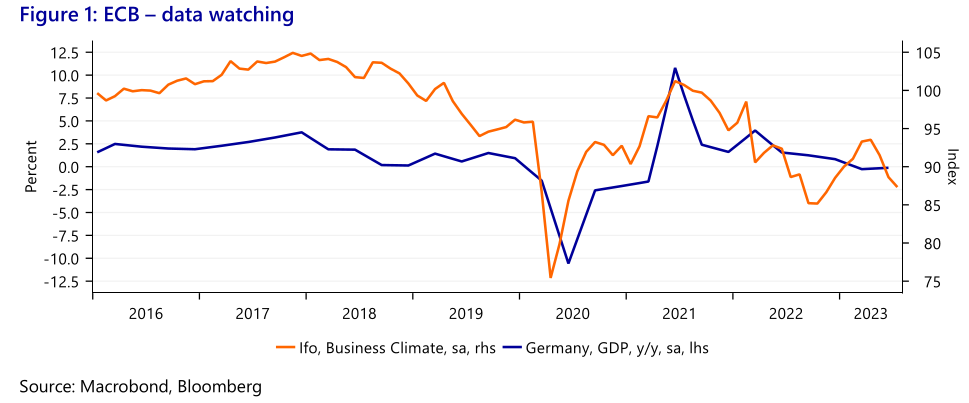

Historically, a slump in the manufacturing sector has been a bit of a crystal ball for a wider economic downturn. That's why PMIs for this sector, like Germany's alarming low 38.8 points, make many nervous. However, this time it might be different (things I say before it isn't different lol)

You see, both during and post-pandemic, the production and demand for industrial goods have been a bit out of wack. First off, production was kneecapped by supply chain issues due to shuttered ports and sick orders. Then, we saw a sudden surge in demand for goods thanks to hefty support schemes and the fact that people had less opportunity to spend their money on services. Naturally, businesses responded by cranking up production and stockpiling inputs to keep the production machine humming.

You see, both during and post-pandemic, the production and demand for industrial goods have been a bit out of whack. First off, production was kneecapped by supply chain issues due to shuttered ports and sick workers.

We saw a large increase in demand for goods due to generous support programs and limited options for spending on services. As a result, businesses increased production and stored resources to maintain a steady production flow.

It can be complicated when a business begins to hoard inputs because it can create a chain reaction throughout the supply chain. This is called the "bullwhip effect," which can cause output levels to become unsustainable in the long term.

It is not surprising that the manufacturing sector is currently experiencing a decline. However, production has not yet reached its lowest point, as it still exceeds pre-pandemic levels.

While the manufacturing sector may not be doing well, we do not anticipate a significant impact on the labor market or a major slump in services. So I'm not predicting a recession for the Eurozone. However, this does not mean that everything is going smoothly. Expect growth to be relatively lackluster in the upcoming quarters.

The main culprit? The restrictive policies of the ECB and its global counterparts are starting to take a toll.

An example is the prediction that the US will enter a recession during the latter half of this year. Additionally, China's growth statistics have been underwhelming. These circumstances do not indicate a promising outlook for a strong economic recovery or rebound.

Inflation

The latest inflation figures are looking good. In June, CPI inflation decreased to 3.0% year-on-year, down from May's 4.0%, and core inflation dropped to 4.8% from 5.3%. Since January's 6.4%, there has been a significant decrease in inflation. This supports Powell's recommendation to move cautiously with interest rate increases. It is possible that the Fed will not implement any changes during the September meeting.

It's important to remember that the decrease in inflation figures for May and June was partly due to base effects. However, these effects are expected to reverse in the upcoming July and August reports. I think headline CPI inflation will begin to rise again in the next few months, starting with July.

On the other hand, we may see core inflation continue to decline but at a slower rate. Nonetheless, it's likely to remain relatively high for the rest of the year. It's worth noting that nominal wage growth, as measured by the Atlanta Fed, was still at 5.6% year-on-year in June.

It's possible that by the end of 2023, the headline CPI inflation could reach 3.6%, while the