Global equity market newsletter - 24-04-2024

Yesterday, the S-word was mentioned—yes, "Stagflation." The economy isn't growing as much as it should, but prices are still going up, which is not the best combination. The latest Purchasing Managers' Index (PMI) reports show warning signs, especially in manufacturing.

Manufacturing is having a tough time in some parts of Europe. Germany's PMI is currently at 42.2, France's at 44.9, and the entire Eurozone is sitting at 45.6. When the PMI score falls below 50, it indicates that manufacturing is contracting, which is not a good sign, On the other hand, the service sector seems to be holding up better. The Eurozone service PMI is at 53.3, which is not much growth.

However, the EU has some more issues. A pile-up of unsold Chinese electric cars at the ports and disruptions from a blockade in the Suez Canal by Houthi forces. These issues could further strain Europe's economic stability.

Looking over at the UK and the US, it’s a mixed bag. The UK's manufacturing is a bit sluggish at 48.7, but services are looking up at 54.9. The US is pretty much balanced, with both manufacturing and services at 50.9. The US manufacturing sector is facing a sharp price increase due to rising raw materials and fuel costs, shifting from the wage-driven pressure that dominated the service sector last year.

I did not finish writing this newsletter completely. I wanted to cover Bitcoin and some long-term stock investment plays, but I didn't have enough time. I have an appointment in the morning, and today was busy. Normally, my newsletters are a 15-30min read

ECB's Panetta delivered a speech outlining a strategy for the EU to prosper through a national-security-focused economic strategy driven by politics. In his speech, Panetta echoed Mario Draghi's call for "radical change"

- Reducing reliance on foreign markets means the EU should decrease its next exports. This shift is important for export-heavy economies like Germany and the Netherlands

- Increasing energy security through "green protectionism", promoting environmentally friendly domestic energy sources to reduce dependence on foreign energy.

- Boost tech production through industrial policies that support domestic tech industries and innovation.

- Rethinking involvement in global value chains, implementing tariffs and subsidies to protect local industries.

- Strengthen external flows, which can lead to higher labor costs if results in less labor supply

- Encouraging joint investments in European public goods, potentially financed by Euribonds that might be bought by the ECB as a 'strategic bond portfolio'

Surprisingly, despite the profound implications of this speech that could fundamentally alter the EU’s economic and market framework, those who usually hang on every word from the ECB—especially when it concerns minor rate adjustments—were notably silent about these transformative proposals."

Global markets saw an uptick, driven by the strong earnings reports of companies such as Tesla, Texas Instruments, and Visa. As a result, those companies' stocks rose higher in after-hours trading. This positive trend was also supported by the impressive performance of Asian semiconductor companies, which boosted Japan's market, especially with the excellent results from ASMI and TXN.

Stocks had been beaten down into oversold territory, and weaker-than-expected PMI data in the U.S. gave investors a break from the recent drop in fixed-income markets. The last two-year bond auction was better than expected. Geopolitical issues are not causing much trouble (right now), the VIX is at 16, and interest rates aren't causing any shocks.

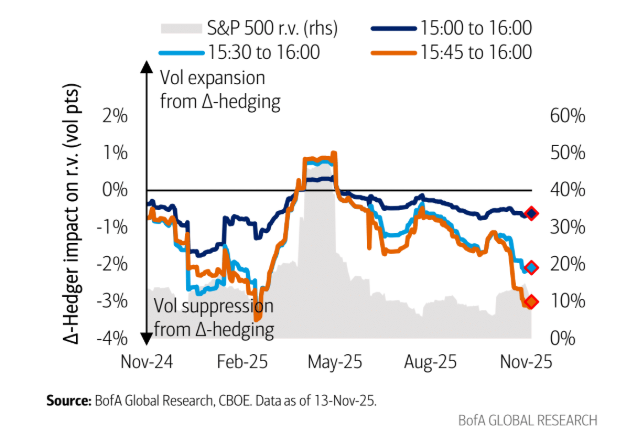

As we move further from the mid-term trigger points, the concerns about CTA supply are easing up. When the spot prices rise, the markets receive a fresh supply of gamma, which naturally lowers the spot volatility.

Commodity Trading Advisors (CTAs) are fund managers who employ systematic trading strategies based on technical signals and trends. When market conditions reach certain trigger points or thresholds, CTAs adjust their positions en masse, which can lead to volatility or sudden changes in supply and demand for assets.

As spot price increases, it often leads to increased trading activity and, in some cases, more options being bought and sold. The uptick in options trading can lead to more "gamma" added to the market. More gamma in the market means that market makers/dealers are adjusting their delta in a more stabilizing fashion. Within a positive gamma environment, dealers buy when equity prices fall and sell when equity prices go up, all to stay delta-neutral. In a negative gamma environment, dealers have to sell when the underlying asset or equity goes down and buy when the underlying goes up, all to remain delta-neutral.

More info about delta hedging here: https://romanornr.medium.com/options-trading-part-2-delta-hedging-9fa6f981883f

As spot prices rise and more gamma is added, those assets' price fluctuations (or volatility) tend to stabilize. Replenishing gamma through rising spot prices naturally reduces spot volatility, adding some support to the market.

But we aren't safe just yet, as we don't know how Meta today and Microsoft and Google will do tomorrow since they haven't announced their earnings reports yet.

The PMIs (Purchasing Managers' Index) have not been a reliable tool for predicting future trends over the last 18 months (or ever). However, the latest reports on the U.S. labor market have some interesting insights to offer. It appears that companies are being more cautious with their hiring in Q2. Many businesses have mentioned that they are not in a hurry to replace employees who have left, resulting in a drop in employment. This is the first such decline since June 2020.

It's much better for NDX to stay above the 100dma. However, there's still a lot of work to be done to get back into the upward trend channel.

CTAs

The market seems to be concentrated on the recent 5% fall in the SPX500 and its effect on systematic traders. Systematic investors, such as Commodity Trading Advisors, sold about $31 billion in global stocks last week, including an estimated $11 billion from the SPX500. The overall position of global net investments is down by 3% from the recent SPX500 peak.

Despite this recent price crack, it didn't hit critical CTA thresholds that would trigger more widespread selling. With these market conditions, CTAs will likely continue to sell more. Based on the current trend, the expected selling volume is roughly $36 billion.

Right now, for the coming week, it's a sell for them in all scenarios

- $36.6 billion worth of selling if the market doesn't change (-$9.5 billion SPX500)

- $22.6 billion worth of selling if the market goes up a lot (-$10 billion SPX500)

- 70 billion worth of selling if the market falls a lot (-$24 billion SPX500)

Over 1-month

- $43 billion worth of selling if the market remains stable (-$9.2 billion to SPX500)

- $45 billion worth of buying if the market jumps up a lot

- $236 billion worth of selling if the market drops a lot