Walmart stock analysis FY23 - FY26

After Walmart shared its earnings for the third quarter, its stock dropped more than 8%. That's a lot compared to the SPX500. Investors were hoping for better news for the financial year of 2023 (FY23), but Walmart's forecast was disappointing and not what everyone was expecting.

Financial year 2024 (FY24): there's a bit of worry about prices going down across markets due to deflation risk. If prices drop, Walmart might not make as much money from selling goods, impacting sales revenue.

Despite these setbacks (it's not over), the negative market reaction to Walmart's stock price was overblown.

TLDR SIR??!!?? CALL SIR?!!?! MY FAMILIA SIR!!! TARGET????!!! ENTRY???!!

TLDR

Walmart has some strengths that can offset these challenges.

- Growth in third-party sellers and increased fulfillment capacity in e-commerce

- Expansion in product assortment

- Benefits from store remodels

Anticipating increased profits from alternative sources like ads and third-party sales in the coming years is reasonable.

Stock ticker: WMT

🚀 BUY: $156.06

🎯 TARGET 1: $158

🎯 TARGET 2: $164

🎯 TARGET 3: $180

❌ STOPLOSS: 0 or valhalla

⚖️ LEVERAGE: Not needed

Sir? Where to trade, sir? My familia, sir?

At Interactive Brokers: https://ibkr.com/referral/romano169

BUT THERE ARE RISKS SO CONTINUE TO READ. THIS IS A RESEARCH ARTICLE SO RISKS ARE ALSO CONSIDERED

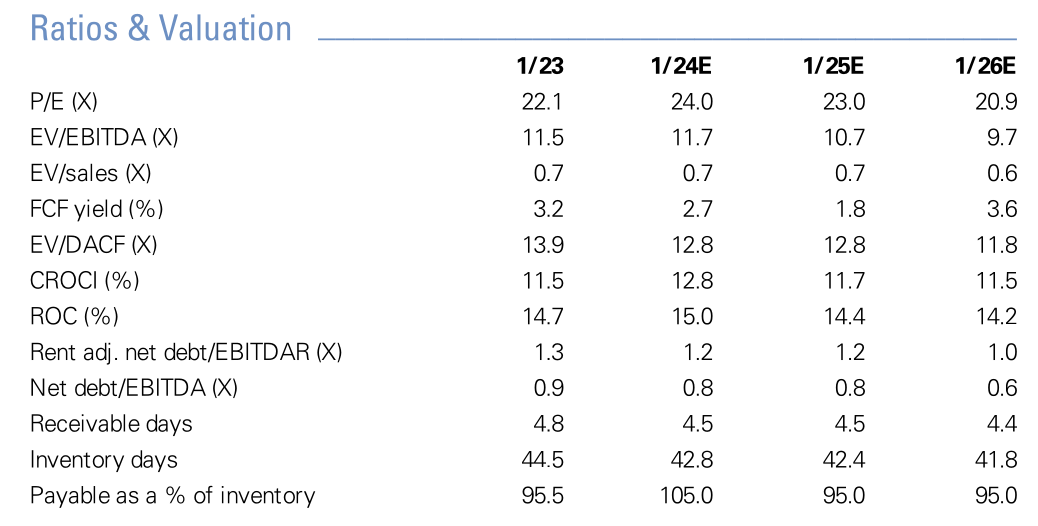

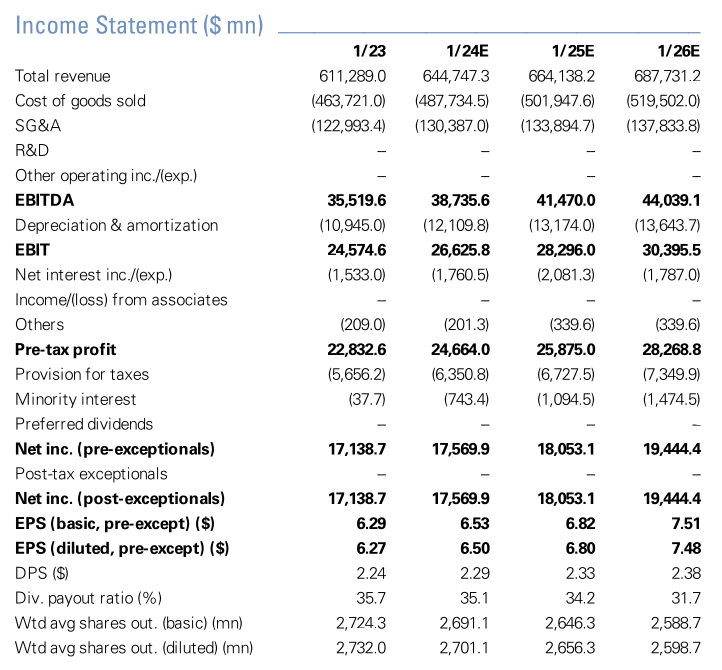

Ratios & Valuation

PE Ratio

The price-to-earnings (P/E) ratio is a crucial metric to evaluate a company's stock price in relation to its earnings. A higher P/E ratio generally indicates that investors are willing to pay more for every dollar of earnings. This is because they have higher expectations for the future and are willing to pay a premium.

The P/E ratio is expected to increase from 22.1 to 24 in the fiscal year ending in January 2024

First of all, let's cover Enterprise Value (EV). It measures a company's total value, calculated by adding the market cap to its debt, minority interest, and preferred shares and subtracting any cash or "cash equivalents." It shows a perspective of the total value of a company from both equity and debt.

EV/EBITDA

EV/EBITDA (Enterprise Value to Earnings Before Interest, Taxes, Depreciation, and Amortization) is a financial ratio to evaluate a company's value of probability.

The EBITDA Earnings Before Interest, Taxes, Depreciation, and Amortization. It's a way to look at a company's profits without the effects of financing (interest), tax regimes (taxes), and accounting decisions (depreciation and amortization)

The ratio starts at 11.5 in the fiscal year ending January 2023 (1/23), meaning the enterprise value is 11.5 times the earnings before interest, taxes, depreciation, and amortization.

The estimated EV/EBITDA for the next fiscal year (1/24E) is expected to rise from 11.5 to 11.7. A higher EV/EBITDA indicates that the market values the company more than its core profits.

EV/sales

First of all, since we already covered "Enterprise Value", let's now cover sales of revenue. Sales of Revenue is the total income a company generates from its business operations, usually reported quarterly or annually.

Calculating the EV/Sales ratio The EV/Sales ratio is calculated by dividing the Enterprise Value (EV) by the annual sales revenue or EV/Sales Ratio = Enterprise Value / Sales of Revenue.

- Lower EV/Sales Ratio: The company is undervalued relative to its sales. You're paying less for each dollar of sales in relation to the company's total value.

- Higher EV/Sales Ratio: The company is possibly overvalued relative to its sales, meaning for every dollar of sales, the market is assigning a higher value of the company.

Usually, a company with a lower EV/Sales ratio compared to its competitors in the same business might be more attractive to invest in.

However, this doesn't consider the company's profitability or efficiency. A company can have high sales, but if it's not profitable, the lower EV/Sales ratio might not be a positive indicator.

EV/Sales ratio of 0.7 for FY 2023 through a projected FY 2025 means that the market valuation of Walmart relative to its sales is stable during these years. 2026 a slight decrease, and that projection, which shows a stable market valuation relative to sales, might be an improvement in valuation efficiency for FY 2026.

Free Cash Flow (FCF) yield

Free Cash Flow (FCF) yield is a financial ratio that measures how much cash a company generates compared to its share price. As investors, we can use it to evaluate the value or yield we might expect for each dollar invested in the company's stock or shares. It's calculated by dividing a company's free cash flow per share by its market price per share.

FCF Yield = Free Cash Flow per Share / Market Price per Share

but it can also be represented as a percentage of the company's Enterprise Value (EV)

FCF Yield = Free Cash Flow / Enterprise Value

- A higher FCF yield: A company is generating a significant amount of cash relative to its share price, which might attract investors seeking cash-efficient businesses.

- A lower FCF yield: A company is generating less cash relative to its stock price, which might not be ideal.

The projected FCF yield of Walmart shows a decrease between the years 2023 and 2025, which means either the company's free cash flow is decreasing, its stock price is increasing, or both. This could be due to different reasons, such as increased capital spending, acquisitions, or other factors that reduce cash flow or a result of the increasing valuation of the company by the market.

In FY 2026, Walmart's forecasted cash flow efficiency increased to 3.6%, indicating a positive signal for investors. This might be because Walmart generating more free cash flow or its stock price is adjusting to a better level compared to its cash generation capabilities.

Enterprise Value/Debt-Adjusted Cash Flow (EV/DACF)

Enterprise value is already covered, so let's go over Debt-Adjusted Cash Flow (DAFC)

DAFC is a way to measure how much cash a company generates while also considering its debt. This helps to better understand a company's ability to generate cash while also accounting for its debt obligations.

EV/DACF Ratio = Enterprise Value / Debt-Adjusted Cash Flow

- A lower EV/DACF ratio: A company is generating more cash relative to its total value, which could be a positive sign

- Higher EV/DACF ratio: A company's valuation is high relative to its debt-adjusted cash flow. It's not a great sign as it may raise questions about their valuation or cash generation efficiency.

Walmart's valuation in relation to its debt-adjusted cash flow has become more favorable from FY 2023 to FY 2026, as indicated by the decreasing trend in the EV/DACF ratio. This suggests that either the company is generating cash more efficiently or its valuation has become more conservative. In simpler terms, the company's worth is improving compared to the amount of money it generates from debt and cash flow.

Walmart is expected to either decrease its total value or increase its cash flow with debt adjustment. This is indicated by a decline from 13.9 in FY 2023 to 11.8 in FY 2026.

AYO, FUCK THIS SHIT. I RAGE QUIT COVERING THIS. I CAN WRITE A SEPARATE EDUCATIONAL ARTICLE ABOUT FINANCIAL STATEMENTS

Let's skip this for now and get into the more important stuff. Otherwise, this will take forever to write about. Here's what matters most anyway

Headwinds

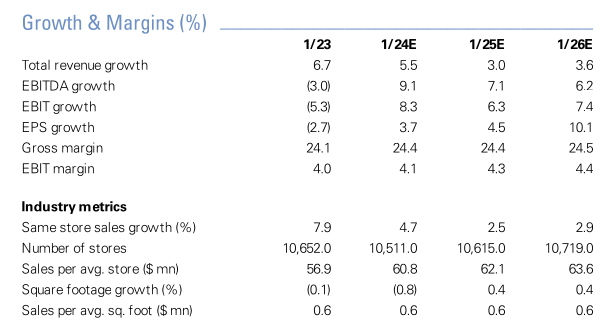

In the next fiscal year, Walmart is expected to face challenges related to pricing, especially in its general merchandise segment. Prices are predicted to decrease, making it harder for the company.

Despite this, Walmart has plans in place to help it succeed. These include expanding its third-party network, improving e-commerce fulfillment capabilities, increasing its product variety, and using the impact of store remodels to its advantage. These actions help Walmart gain more of the market and increase its revenue.

So... about these "challenges", let's cover that first.

Pricing and inflation trends

- Prices for general merchandise are expected to slow down, ranging from low to mid-single digits.

- Inflation in food and consumables is decreasing, with rates ranging from 2.5% to 4%, indicating a disinflation of over 300 basis points over the quarter.

- So, deflation is expected to affect the businesses more next year, especially in the general merchandise sector.

Strategic positioning against pricing pressure

- Walmart plans to increase its market share by expanding its e-commerce fulfillment capabilities and partnering with more third-party sellers. This strategy aims to meet their target audience's needs and improve their overall customer experience.

- As part of its strategy to combat potential pricing pressure, Walmart has a plan to expand the variety of products they offers and improve its stores. This includes remodeling stores to make them better for customers.

- Walmart has noticed that sales have increased in certain categories such as tires, batteries, and home products due to a fall in prices.

- Sales in categories such as media and gaming have not been doing well, whereas sales in other categories have been better.

Operating income

So, when looking at Walmart's recent financial performance, an interesting story unfolds between how much Walmart is making from its everyday business (operating income) and its overall sales.

Walmart's sales growth increased by 5.3% during the third quarter, while the operating income went up by 3.3%. Although this sounds positive, it is less impressive than the sales growth.

Walmart faced extra costs during a certain period. They had to spend an additional $100 million on legal fees and also spent more to renovate many stores at a faster pace. These additional expenses not only impacted the third quarter but also had lingering effects into the next quarter.

Walmart predicts that the money they make from its core business will start growing faster even double the are of their sales growth. That means they're getting back to their usual way of doing things, where they make more money again.

For the upcoming fourth quarter, Walmart expects to see better profit margins. They're not planning to slash prices as much as they did last year, especially in areas like electronics and home goods where they had a lot of stuff in stock. They think they can save money on moving goods around (supply chain costs) which also helps boost their profits.

Even though Walmart has been dealing with some extra costs lately, it looks like they've got a plan to "We're so back" and keep their profits growing.

Estimated changes

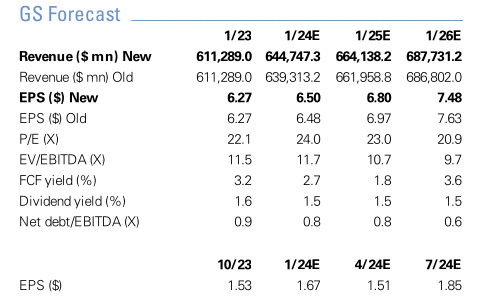

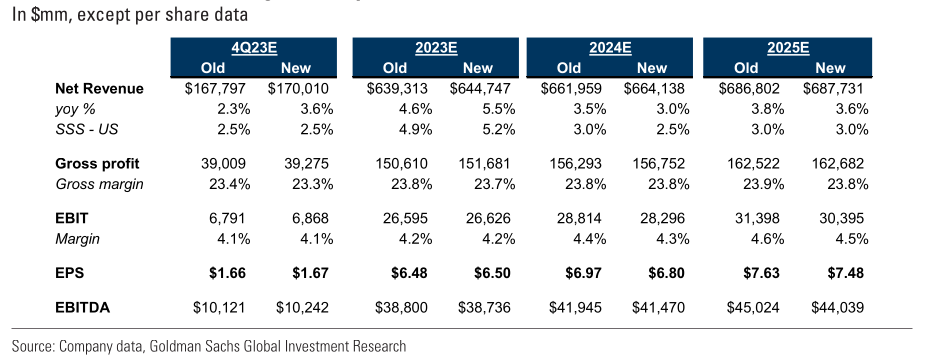

So, the Adderall-fueled quants at Goldman Sachs have adjusted their predictions a bit for Walmart's Earnings Per Share (EPS).

For the fiscal year of 2023, they're nudging their estimate up to $6.50 from their earlier $6.48, mainly because Walmart did better than expected in Q3.

For the next couple of years, fiscal year 2024 and 2025 they're actually lowering their EPS estimates. Now they think it'll be $6.80 and $7.48. That drop in expectations is because they think Walmart won't be making as much money from selling stuff in the first half of 2024. They forecast the prices won't be going up as much due to lower inflation. Walmart won't have that extra boost from higher prices to pump up their sales figures.

However, beyond the doom and gloom, they think Walmart will still manage to squeeze out a bit more profit thanks to making money in other ways like advertising and offering services to fulfill online orders (alternative profit streams) - Walmart's side hustles

Walmart will make more money from new areas even though they might not rake in as much from just selling products due to inflation calming down.

Become a Premium member. Premium newsletters & Discord community access

ALSO, THE ARTICLE DOES NOT END HERE

Join Discord to get the full value out of the newsletter. There's no extra cost associated with Discord. Yes, options data, such as dark pools, options gamma, unusual flow, etc., are also included. Also, educational content, reports, and direct questions to me, and often, I share my trades & thoughts in real-time as the market moves.

However, I want you to understand rather than copy a trade.

Become a premium member. Besides crypto, if you cashed out a lot or are planning to. I highly recommend "stocks" section for long-term plays.

Valuation & Risks

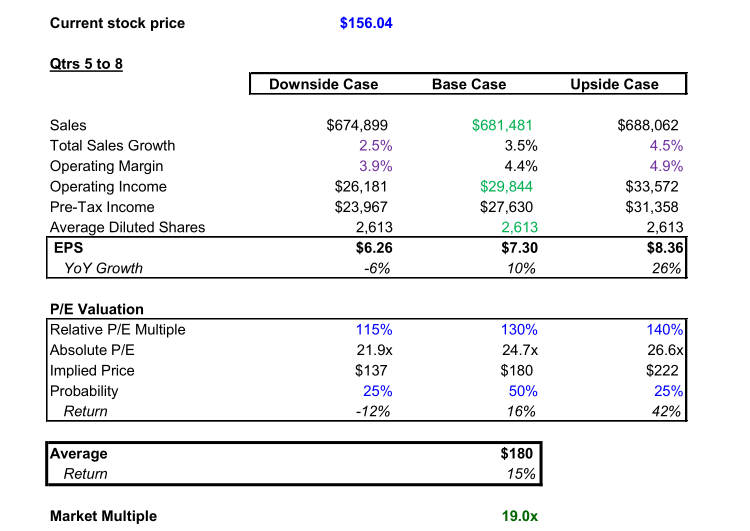

Goldman Sachs' stance on Walmart is basically positive, recommending it as a 'Buy' (which I agree on). They made a small adjustment to their price target for Walmart stock, dropping it from $182 to $180 for the next 12 months.

There are some reasons for the price adjustment. They're a bit less optimistic about Walmart's future earnings. They're also changing how they compare Walmart's stock price to its earnings relative to other companies: 115%/130%/140% instead of 120%/135%/145%. They've done this because they're worried about deflation, which could mean lower prices and profits.

There's a silver lining, overall stock market will value companies more generously than before as they think the increased deflation risk is partially offset by a higher market multiple (19.0x vs 18.6x prior)

Potential risks

- If the economy hits the brakes, it could spell trouble for big retailers like Walmart.

- A competitive environment where prices are constantly being slashed could hurt Walmart's profits

- Unpredictable global economic conditions and currency risk add up to the uncertainty

- If Walmart can't balance its spending on e-commerce and competitive pricing with savings in other areas, its finances could take a hit

- Rising costs for things like employee wages or shipping could also put pressure on Walmart

- Impact of tariffs (taxes on imported goods, could also be a risk factor)

ApeX DEX

ByBit has made KYC mandatory as many other exchanges. Why not try out ApeX DEX? You can use your wallet or social account to use the DeX. No gas fees are required for trading & the fast trading experience is like a CEX.

You don't even need metamask, using social logins such as facebook, discord, Gmail is an alternative option. That way, you can access ApeX anywhere.

Consider ApeX DEX

By the way, ApeX added a lot more altcoin futures such as Celestia $TIA

Instructions:

https://twitter.com/RNR_0/status/1652360705331347461

For a lifetime fee discount, check the link.