Signposts triggers - March 17, 2023

As people start to pull their money out of banks or "deposit outflows" start to happen, things will get tough for them.

Deposits outflows refer to this context when a large amount of money is withdrawn from banks and or other institutions or a decrease in the total deposits held by a bank.

Considering what happened to Silver & Silicon Valley bank, that's understandable.

When a large amount of money is removed from a bank’s deposits, the bank’s balance sheet is negatively impacted.

Tip: Use the play button to listen to the article instead of reading!

Especially if they put customer deposits into bonds with a long maturity date. This is what happened to Silicon Valley Bank. I wrote about it the previous time. I don't like to repeat myself and explain everything again.

This post is publicly for free publicly usually these posts are for premium subscription members only. Consider this as a teaser.

The implication of Fed Easing and Credit Tig

Okay, maybe a small toggle button about the Federal Reserve bailing out the banks (or "Special Financial Operation)

Federal Reserve to the rescue: Treasury & FDIC Bank Term Funding Program

It's all so tiresome, but... here we go again.

In response to the failure of Silicon Valley Bank and the potential of further damage to the US banking systems, the Federal Reserve, Treasury, and FDIC announced a new sort of "bailout package" (from the looks of it, correct me if I'm wrong).

This includes the Bank Term Funding Program (BTFP), which provides loans to eligible depository institutions using US Treasuries, agency debt, mortgage-backed securities other qualifying assets as collateral.

The Department of the Treasury has committed up to $25 billion to backstop.

The FDIC insures people's money into Signature Bank and Silicon Valley Bank so that this program will protect their money. However, shareholders and certain unsecured debtholders, however won't be protected.

The BTFP might have an impact on the US equity markets. With access to additional liquidity, BTFP and other depository institutions may have more resources available to invest in the markets.

I'm not sure yet how this can impact the US dollar (as I'm writing this article at 4 am right now), but there might be an increased demand for US dollars again. I'm not sure, and I need some sleep and further reading.

BTFP can affect the Federal Reserve's plan to hike interest rates further.

I'm not sure, but BTFP loans, provided at a lower interest rate, could lead to lower borrowing costs for banks and other depository institutions. Also, the collapse happened because the Federal Reserve decided to hike rates so aggressively (I was expecting something to break or a credit event)

It's worth asking: $25 billion backstop for $18 trillion deposits?

This decrease in deposits, as well as liquidity, can result in a threat to the financial stability of the bank.

As a result, the banks have to look for higher funding costs to acquire new funds.

This often raises interest rates banks must pay on loans, credit cards, and mortgages when banks are forced to pay higher interest rates on their loans, credit card interest and mortgage interest. Bank customers usually bear the burden in the form of higher rates on the loans and consumer credit products they use.

This means a rise in funding costs and so the rates that customers have to pay for services and money to borrow from the banks too.

As people are starting to doubt the US banking system and their financial situations. They are less willing to take extreme risks. Investors become risk-averse, and companies, startups, etc., will have difficulty finding investors willing to back them.

Also, they are more careful and less likely to invest in stocks, bonds, etc.

That sentiment of caution may lead to an overall tightening of credit conditions as the risk of default rises. Lenders may demand higher risk premia.

Meaning they will charge the bank a higher interest rate on their loans to compensate for the additional risk they're taking).

The FDIC, which stands for Federal Deposit Insurance Corporation, provides up to a certain amount of insurance to depositors in their member banks and credit unions. This helps to protect depositors by guaranteeing the return of at least some of their deposits up to the insured limit.

However, the FDIC’s insurance does not cover the losses of equity or debt investors in the bank. This means that capital market participants may take a significant financial hit.

The FDIC recently stepped in and guaranteed the deposits of the failed banks (i.e., Silicon Valley Bank). Unfortunately, equity and debt remain unsupported, and capital market participants are taking a huge hit.

If you're enjoying this newsletter, consider signing up for a premium subscription, a discord discussion server will be launched soon as an extra for premium subscribers.

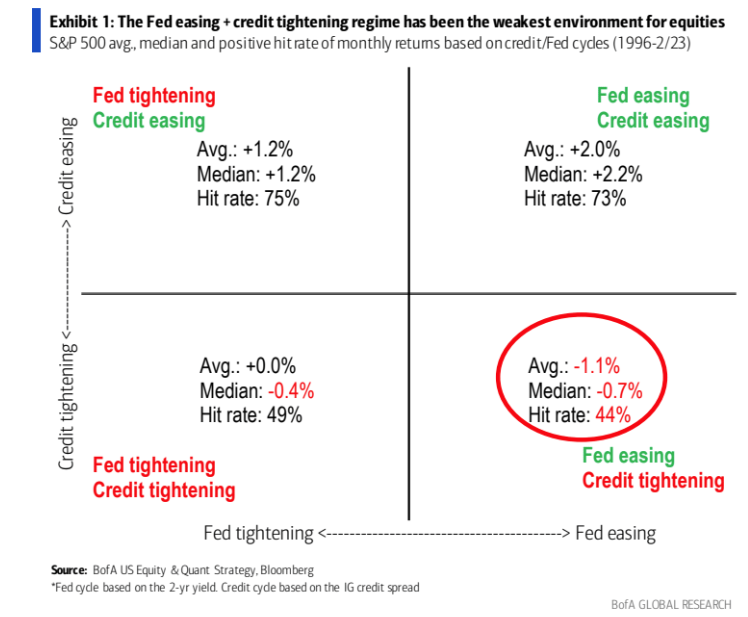

The implication of Fed Easing and Credit Tightening

Okay, here it gets a little bit tricky, but let's go over it. I can't promise this will be well explained, but I'll try. I may also be completely wrong.

The relationship between the Federal Reserve's policy position and the equity market's performance is complex and dynamic. Let's make that clear.

Generally, the Federal Reserve's easing of policy (lowering interest rates) is usually seen as a bullish sign for stocks.

While tightening policy (raising interest rates) is usually seen as bearish.

But when coupled with tightening credit conditions, these easing and tightening policies can have a large but different effect on the equity market.

As of last week, the market was anticipating 3 rate hikes by the end of the year, but shit has changed this week, and the market now anticipates 2 rate cuts by the end of the year.

Before equity bulls get too excited about a Fed change, they should remember that easy Fed policy and tightening credit conditions have been the worst time for stocks.

This is because when the Federal Reserve changes policies, such as lowering 2-year yields, it may seem like a good thing for stocks.

But, in reality, it is often the worst time for stocks. This is because when the Federal Reserve lowers yields and credit spreads become wider, and it means that businesses have less money to invest, while consumers may spend less due to lower borrowing costs.

As shown in Exhibit 1, history has proven that tightening credit conditions, combined with easy Federal Reserve policy, results in losses for the S&P 500 index.

Widened Risk Premia

Recent market developments indicate that risk premia have been widening.

Risk premia measure the extra return investors demand, taking on additional risks. During March, we saw this risk-premia widen. This means that investors have been asking for more returns from their investments to make up for the risks they’re taking on.

One way we can measure this is through the spread between corporate bonds and US Treasury bonds (known as credit spreads).

We’ve also seen an increase in the spread between stocks and US Treasury bonds (known as equity spreads).

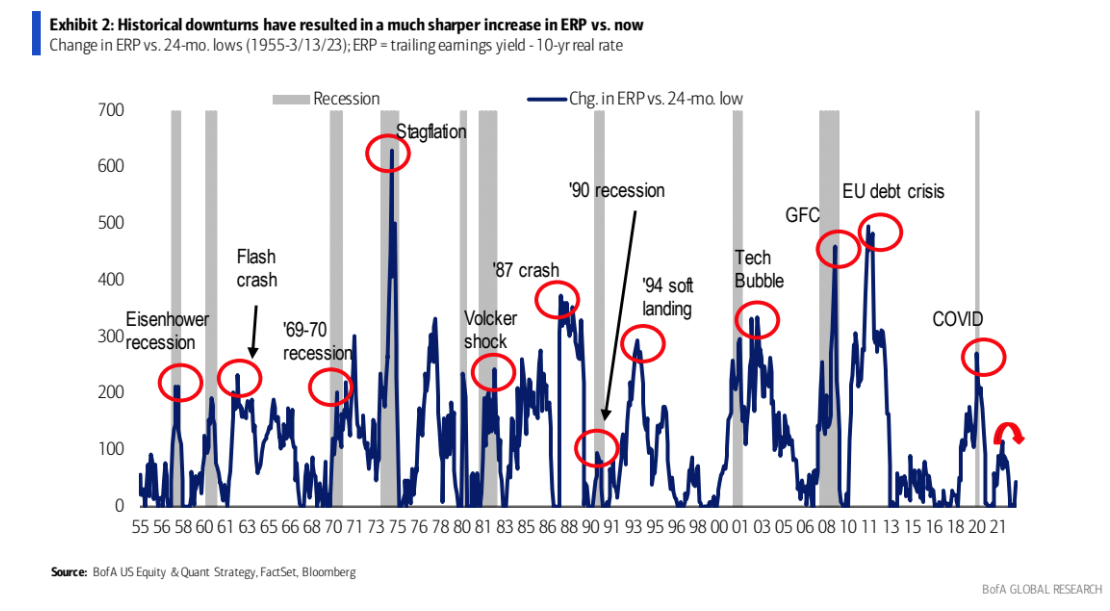

This measurement is called the equity risk premium (ERP), which measures the expected return on stocks minus the expected return on Treasuries.

Equity Risk Premium (ERP)= Trailing earnings yield - 10-yr real rates

From the beginning of march alone, we saw ERP increase by 40bps.

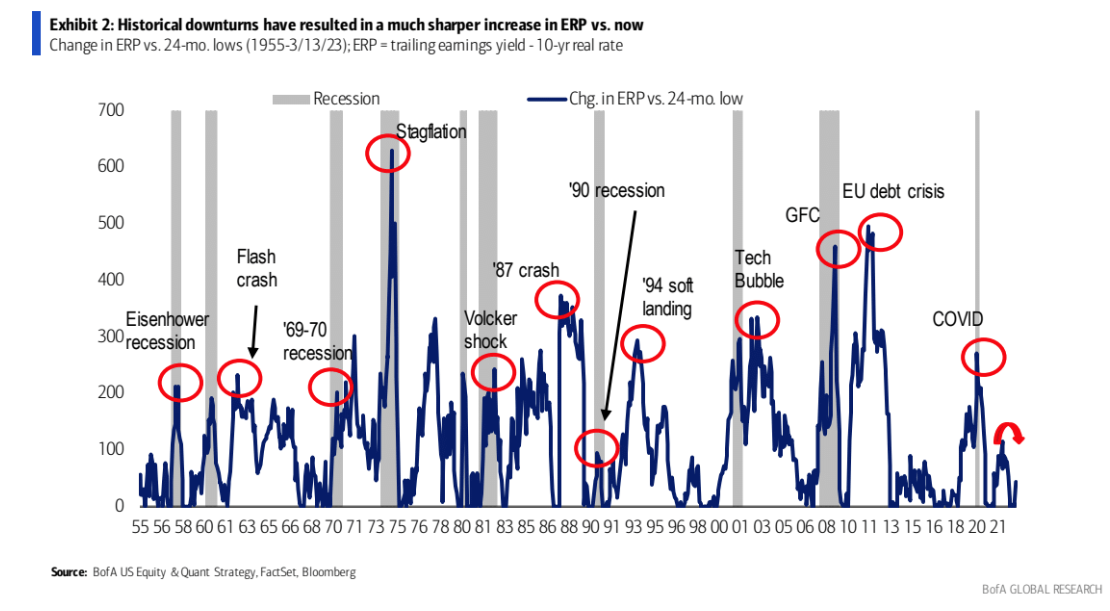

During economic downturns such as recessions, investors tend to be more cautious with their investments because they consider the risk of owning equity to be higher. As a result, the Equity Risk Premium (ERP) widens significantly (Exhibit 2).

This means that investors accept a lower return for taking on the greater risk of equity investments. We anticipate that the next recession (May start in the 3rd quarter of 2023) will cause ERP to rise even further, which could more than compensate for the beneficial effect of falling interest rates.

The widening of the risk premia has implications as it indicates that investors may require higher returns for taking additional risk, and the performance of risky assets may be more sensitive to a recession.

So, risk premia have been widening recently, with ERP up 40 basis points up this month, suggesting that investors may require higher returns for taking on additional risk.

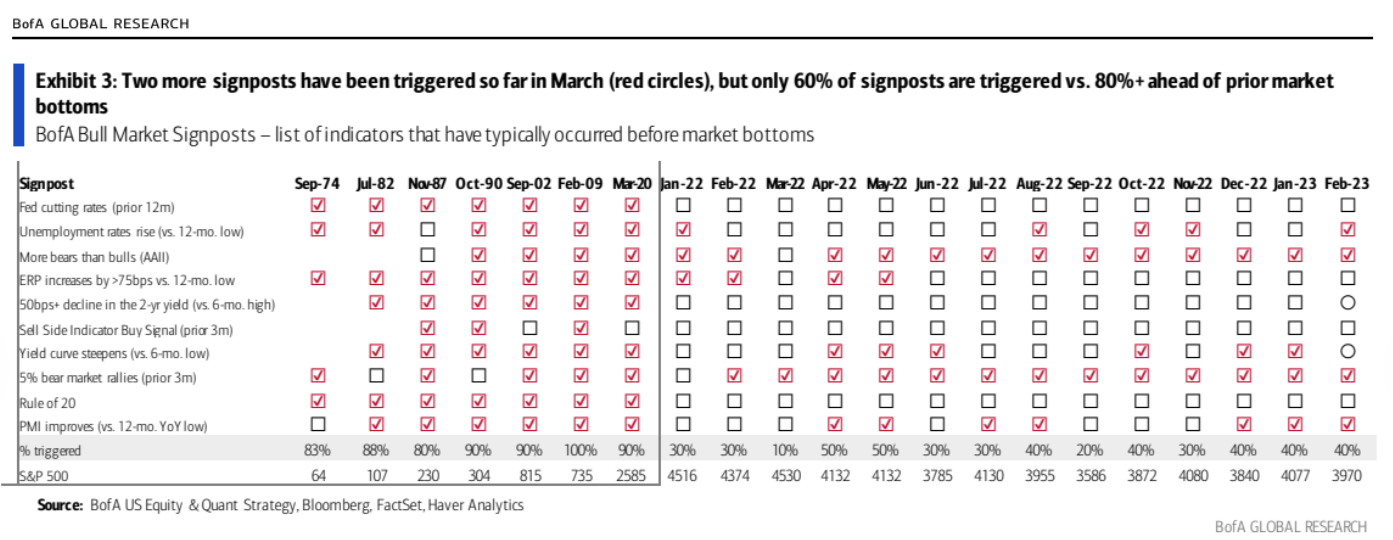

Understanding signposts that signal a Market Bottom in a Bear Market

We are currently in a bear market, and the total number of signposts that signal a bottom can vary depending on the market environment. Typically, there are more than 80% of signposts signify a market bottom.

You may wonder what a signpost is.

A signpost is an indicator that signals a bottom in a bear market. These signposts can take different forms depending on the financial market environment, but they all provide clues that the bear market may be reaching its end.

Examples of signposts include lower yield on 2-year bonds or a steeper yield curve.

The total number of signposts that suggest a bottom, and the percentage that have been triggered, can be used to gauge how close the market is to reach its bottom. The number of signposts triggered is one such indicator. The total number of signposts indicating a bottom can vary depending on the market environment but typically is greater than 80%.

(Yeah, okay. Not going to lie. That already sounds difficult to understand)

As of the end of February, only 40% of these signposts had been triggered, which was lower than the number of signposts seen in prior market bottoms.

However, two more signposts were triggered in the last week: the lower yield on 2-year bonds and a steeper yield curve. This brings the total percentage of triggered signposts up to 60%, the largest number seen in this bear market (so far).

That may suggest we are getting closer to a market bottom.

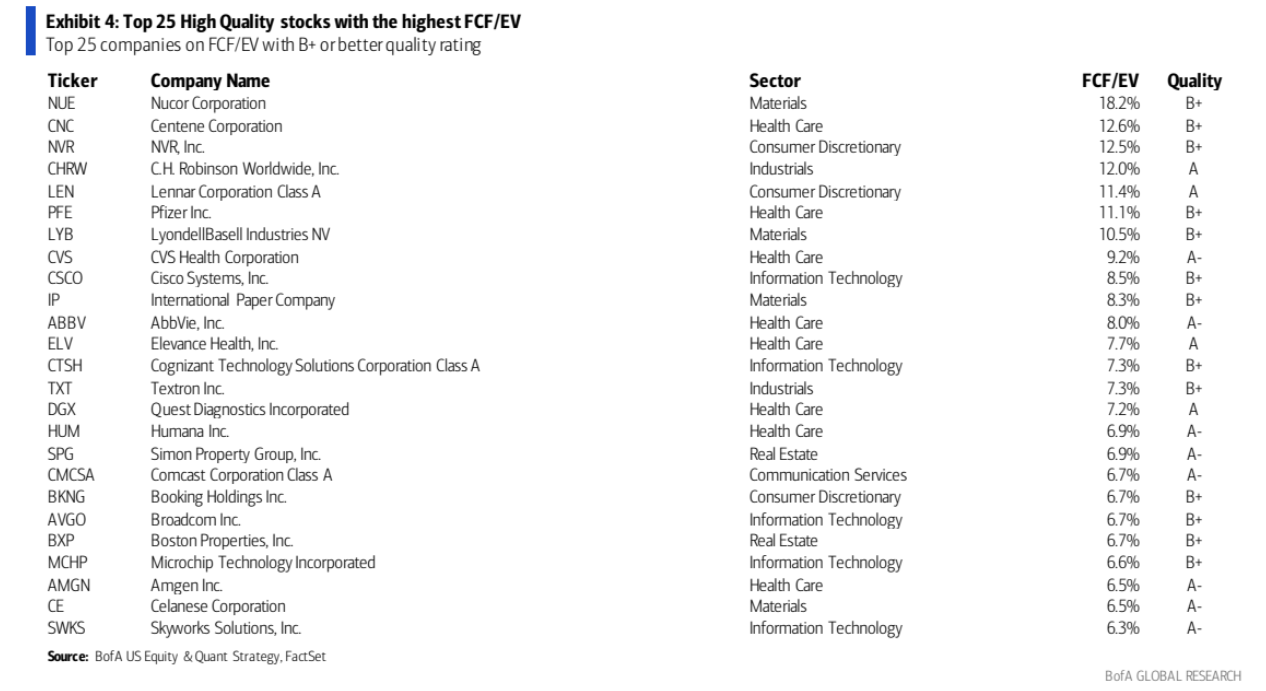

Investing in stocks rated B+ or higher according to S&P's quality rating system is beneficial for both short-term and long-term reasons.

The market's current instability, decreasing profits, and the ending of easy fiscal or monetary policies all suggest that having high-quality stocks would be beneficial.

Additionally, larger financial firms now offer a great opportunity for those in the industry, and smaller regional firms and other financials have also seen an improvement in their ratings.

According to Bank Of America, having these stocks is important for the company as it can provide self-funding and offer the opportunity to distribute free cash to shareholders.

Newsletter Premium Subscription

Premium subscription

Tired of seeing low-effort content on Twitter with random people posting lines on a chart?

Maybe subscribing to this newsletter is something for you to gain an edge over the market.

Also, read my free medium articles: https://medium.com/@romanornr/

Full access to exclusive premium content

Subscribe, and get a competitive edge over the market.

Take the first step to kick your wife's boyfriend out of the house & stop getting liquidated.