Pedal To The Metal?

The FOMC held rates at 4.25 - 4.5% as expected. Governors Waller and Bowman dissent in favor of a 25-bps cut. That's the first time since 1993 that two Governors dissented from the policy decision.

The Fed lowered its growth outlook, saying that “growth of economic activity moderated in the first half of the year,” instead of the earlier phrase “continued to expand at a solid pace.”

This came despite Q2 GDP printing at 3.0%, after a 0.5% contraction in Q1. The Fed might be reacting more to underlying demand than to headline growth.

The statement removed the phrase "has diminished but" from the sentence on uncertainty, now reading “uncertainty about the economic outlook remains elevated.”

Btw this part may be boring, you can skip this part and head to the next section

Powell addressed the unusual dissents, stating the current supply shock environment creates dual-sided risks, making internal disagreements understandable. However, he also noted that Waller and Bowman are Trump appointees.

Everyone knows Powell is on his way out. Just like players stop listening when a coach loses the locker room, the Fed's internal discipline is weakening. This tug-of-war shows the Fed will move slowly and carefully, favoring modest adjustments over aggressive actions.

Perhaps we see just 1 rate cut at the end of the year, possibly the September meeting, but the risk of a later move can increase depending on incoming data.

Expect Trump's influence on monetary policy to grow in 2026, starting with Governor Kugler's replacement and followed by the anticipated appointment of a Trump-aligned Fed Chair in June.

With Waller and Bowman already establishing a foothold on the Board of Governors, a Trump-loyalist leading the way would likely form a policy bloc in favor of aggressive rate cuts. Expect them to push for a 25bps cut each quarter throughout 2026.

Not calling for chaos or full politicization, but skewed decision-making due to ideological alignment. The idea that Trump wants to push for an extreme 300bps in cuts while the Fed only delivers a more moderate 100 bps (1 cut per quarter) doesn't seem that far off.

However, it might not be as straightforward. We could see public speeches from regional Fed presidents pushing back against cuts, arguing to preserve credibility.

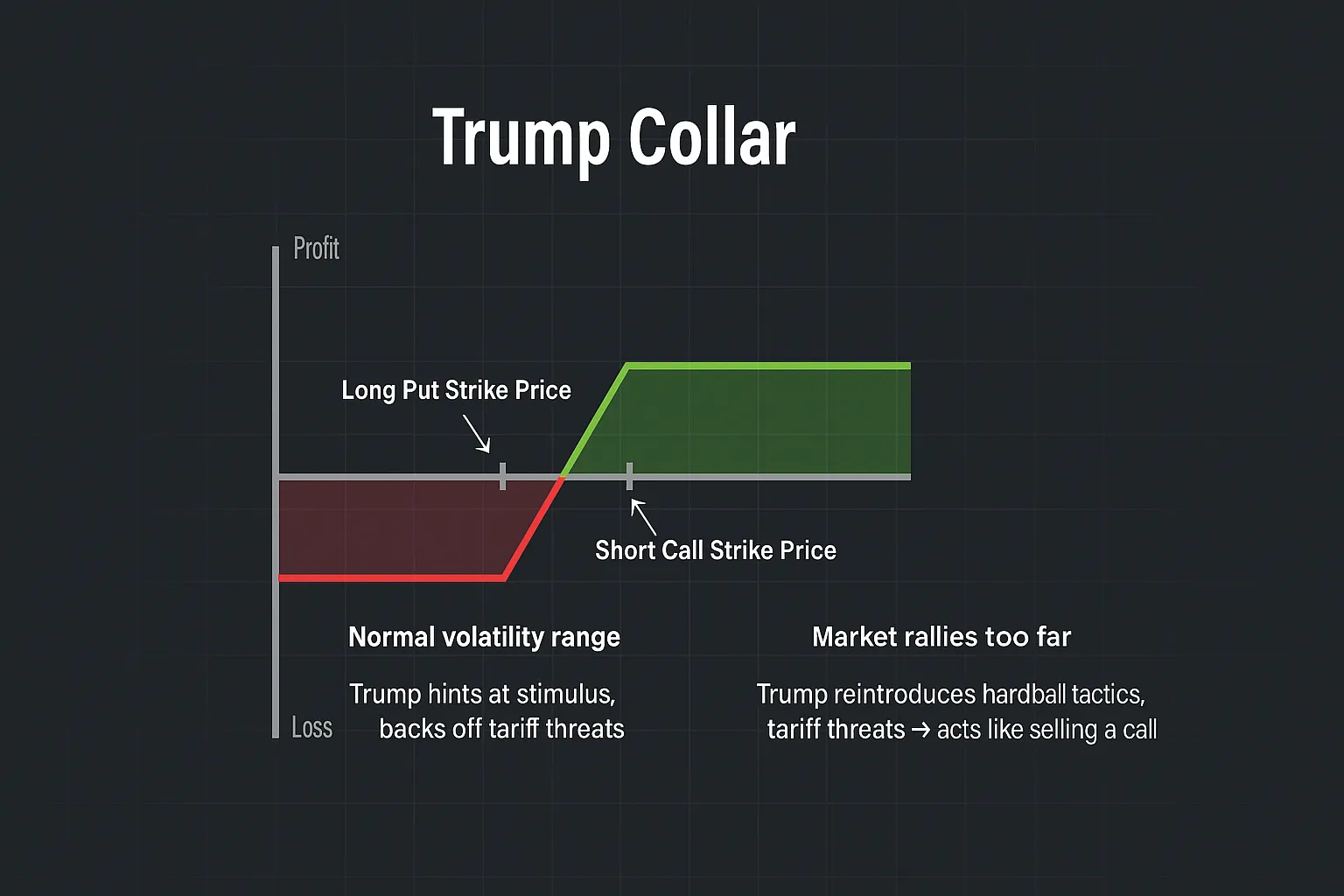

The Trump Collar trade

The broader microenvironment been a textbook case of what as a shift from left-tail to right tail.

For several months, this has captured how the market became over-fixated on extreme downside risk (especially around the tariff tantrum) while massively underpricing any right-tail outcome.

This skewed focus on risk ignored mechanical reallocation flows from positioning dynamics that were bound to unfold as the collapse in realized volatility happened.

Volatility-targeting strategies (e.g., risk-parity funds, vol-control funds) that increase exposure to equities when realized volatility falls. Rebalancing flows from pension funds or 60/40 portfolios that buy stocks after a sell-off to maintain allocation targets. CTA strategies that mechanically long risk-assets as momentum continues.

Volatility compressed, opportunity narrowed, not towards chaos but towards stabilization and an incredible melt-up, while market participants positioned for disaster and were left sidelined.

Trump's policy signal created a structure for volatility containment. When the markets were rallying, Trump would inject tariff threats or hawkish trade rhetoric to cap the inside.

During the drawdowns, he would walk back to the aggressive stance or hint at stimulus, cushioning the downside.

These actions started to compress volatility because markets began to anticipate his reaction

“If we go up too fast, Trump gets emboldened and starts reintroducing hardball tactics. If we fall too much, he backs off and softens the stance.”

- Injecting tariff threats or hawkish rhetoric when markets rallied

Trump caps the upside with risk-off signals. - Backing off or hinting at stimulus during drawdowns

Trump cushions the downside.

Do you see the pattern?

Markets began to anticipate this reaction function, which was gradually priced in as traders realized, leading to more volatility compression.

Pedal to the metal

This initial volatility compression from Trump's predictable moves turned into a full-blown volatility collapse, as his policy removed both the downside far and upside contraint with a final catalyst came with the administration's pivot back to Trump 1.0 pedal-to-the-metal stimulus regime with the passage of the One Big Beautiful Bill which abandons Trump 2.0 spending cuts.

The market has moved past its tariff PTSD, which was a source of left-tail risk and is now seen as mainly neutralized or negotiable, as trade deals get rolled out and worse-case tariff outcomes are increasingly being priced out. Fears of stagflation and trade-induced slowdown have faded, by now, replaced by a right-tail fear of the upside supported by fiscal stimulus and a strong consumer.

No more "sell calls", with him capping the upside with tariff threats has been replaced by full-throttle pro-growth.

5 downside beats in Core CPI lit the match under for explosive upside. Dismantling the stagflation narrative. With inflation cooling faster than expected, the market has been forced to reprice disinflation.

Anyone who was fixated on the left-tail got left behind. Positioning that was once heavily skewed toward left-tail protection has flipped as underexposed market participants are now forced to chase the upside, creating a squeeze in the market.

Massive leveraged ETH demand from retail added fuel to the fire. Not from conviction but from forced participaton

Become a Premium member. Premium newsletters & Discord community access

What about my long-awaited dip?

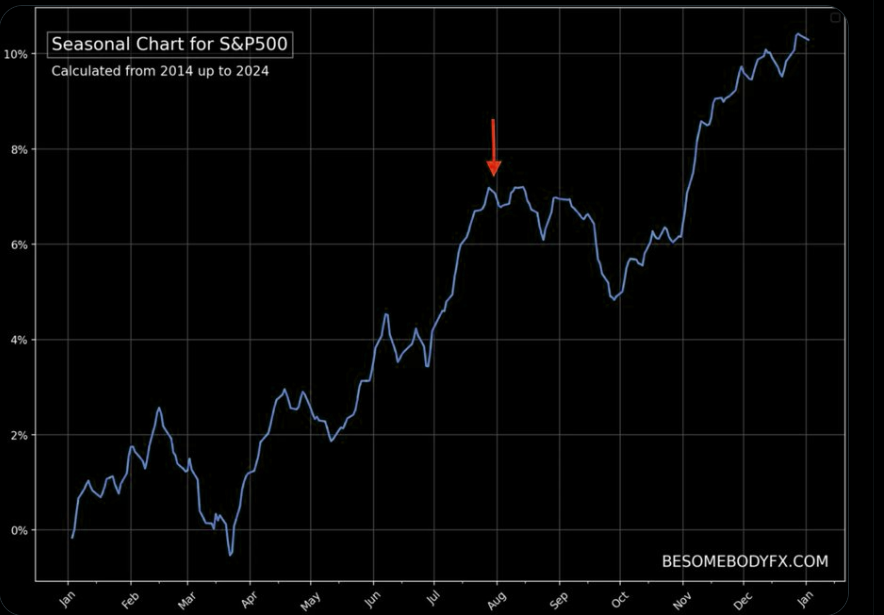

However, I do expect to buy some dips in the equity markets along the way, from a seasonality perspective. This does not have to play out, but it is worth keeping in mind.

We should not dismiss the possibility that the Trump administration might revisit agreed trade deals and keep using tariff threats as a negotiation tactic.

Watch for the announcement of the Fed’s interest rate decision on Thursday, July 31, along with commentary on the impact of tariffs, the ongoing second quarter earnings season, and announcements on AI capital expenditure, as well as further details on trade negotiations with China.

Look, we had an incredible rally, which we played out perfectly. Read this post back on April 6th, or read our Discord, you probably bought the bottom when SPX500 fell into the 4800-5000 area.

Good news is now being priced in. Markets could be vulnerable as people drop their hedges. There could be great hedges made with VIX call spreads.

If you are still underallocated, you should prepare to add exposure on potential market dips in the weeks ahead.

Load up your IBKR broker account

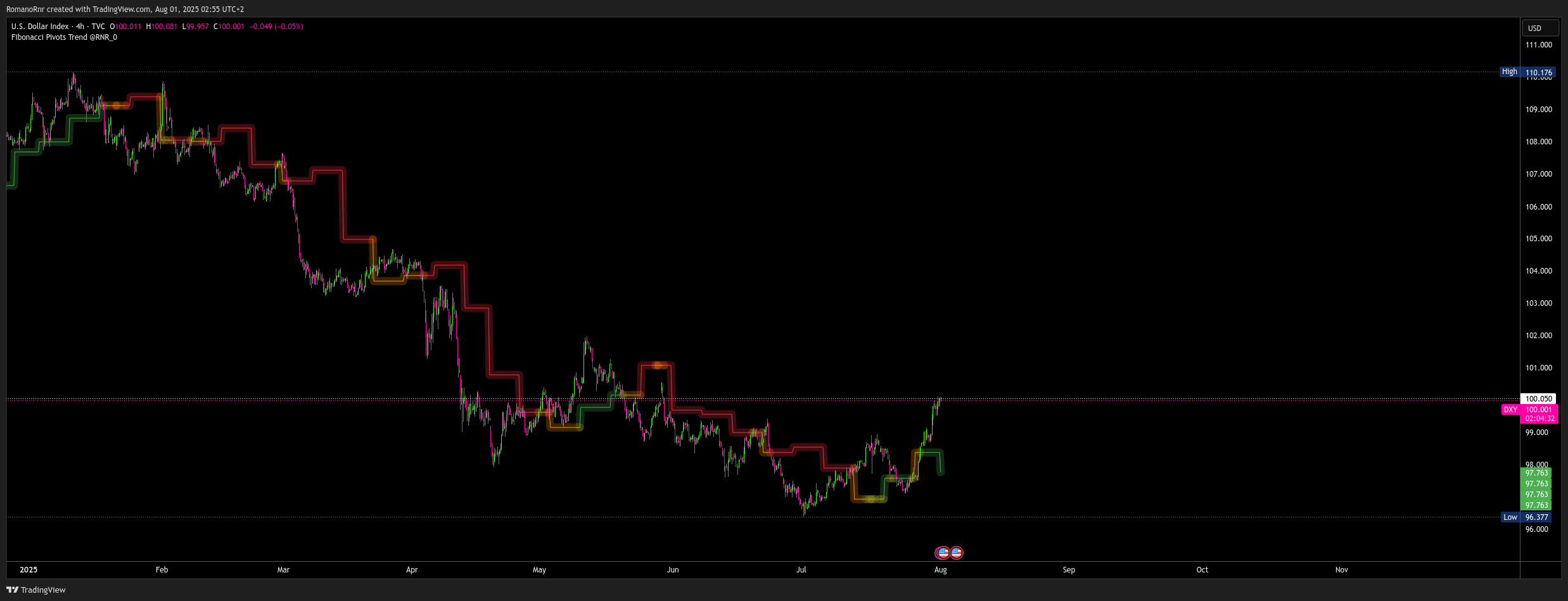

The dollar

Despite the narrative of “U.S. exceptionalism” returning (i.e., the U.S. outperforming economically), the U.S. dollar has kept weakening. If the DXY (dollar index) drops below 95, it could signal the green light for a dollar debasement trade.

Allocation to gold is a strong hedge against lingering geopolitical and political uncertainties, including potential concerns about Fed independence. I stick with my gold $3500/oz target and not ruling out the possibility of prices going higher.

Become a Premium member. Premium newsletters & Discord community access

And much more in the Discord.

Become a Premium member. Premium newsletters & Discord community access

Since Trump is imposing tariffs, here is the opposite

50% discount forever on yearly subscription

oin Discord to get the full value out of the newsletter. There's no extra cost associated with Discord. Yes, options data, such as dark pools, options gamma, unusual flow, etc., are also included.

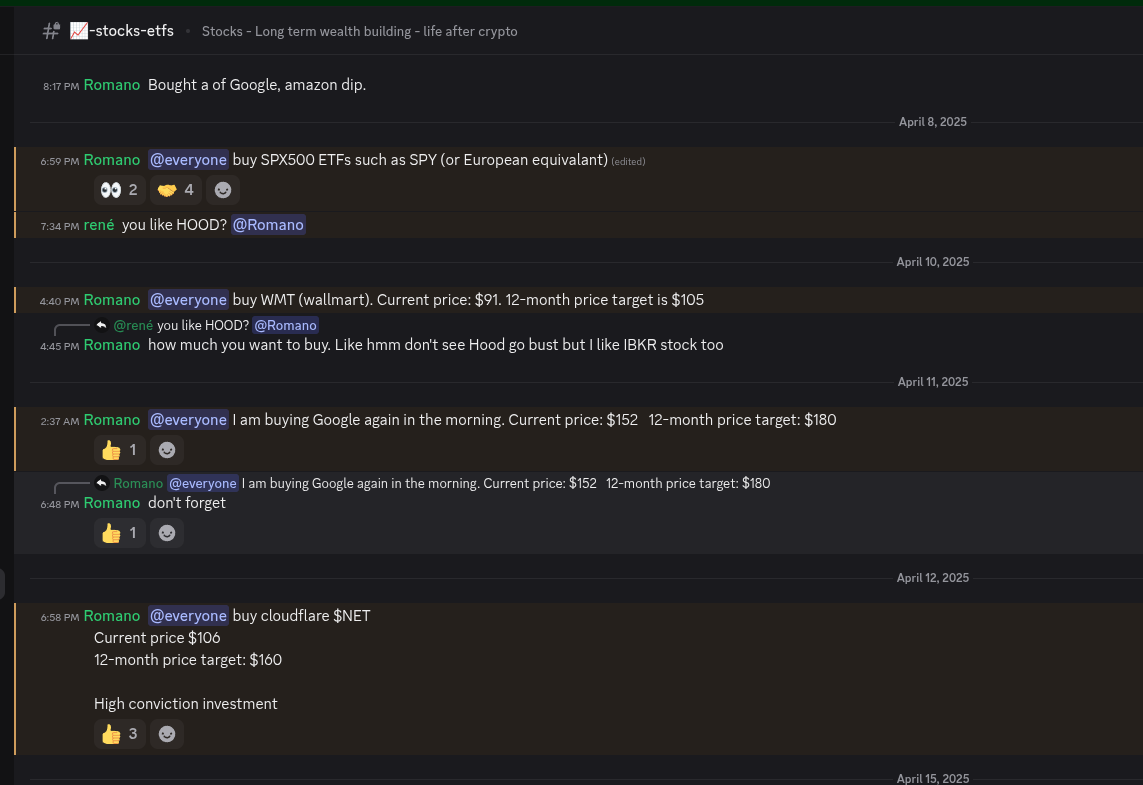

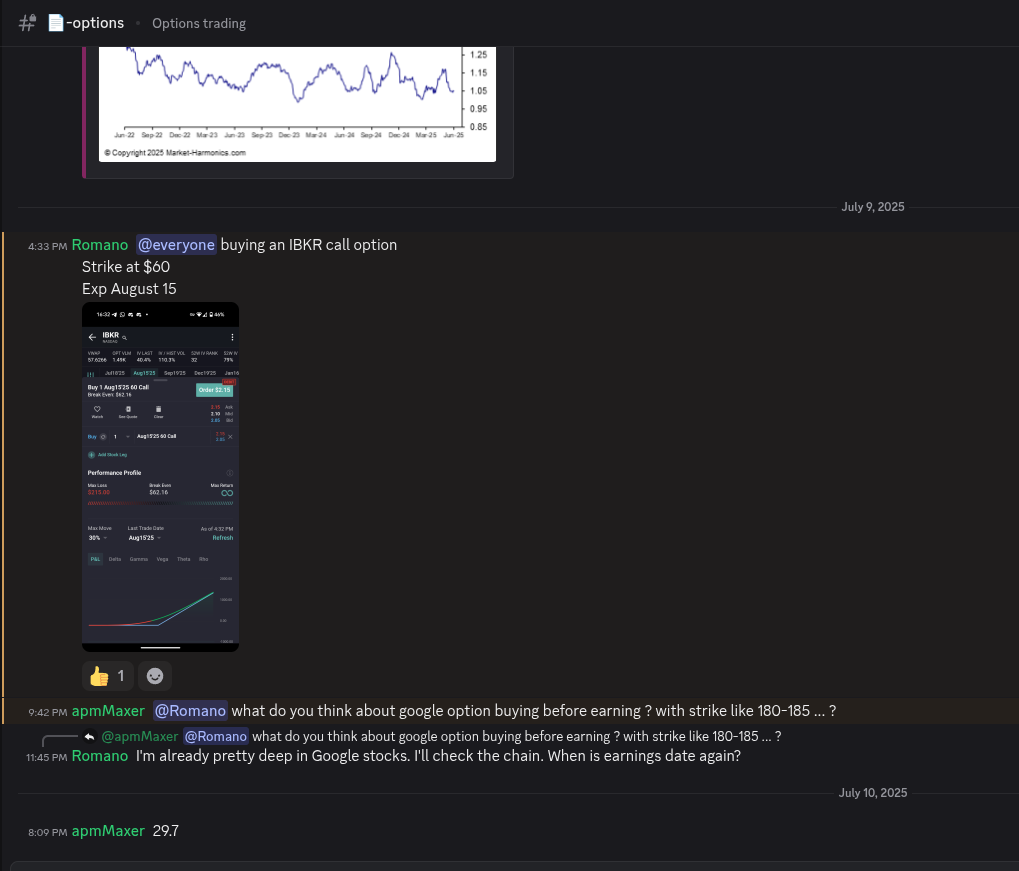

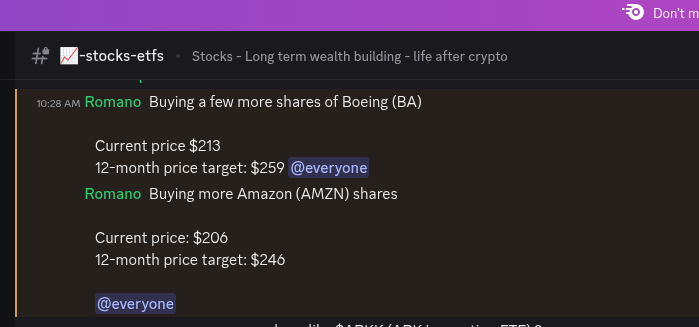

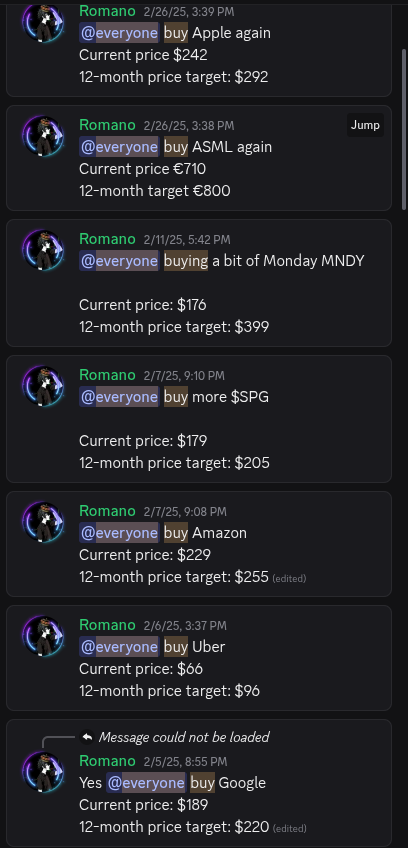

Besides crypto, if you cashed out a lot or are planning, I highly recommend the "stocks" and "fixed-income" channel on Discord for long-term plays and wealth-building.

That's where the real money is made with actual long-term stress-free trades.

One more thing

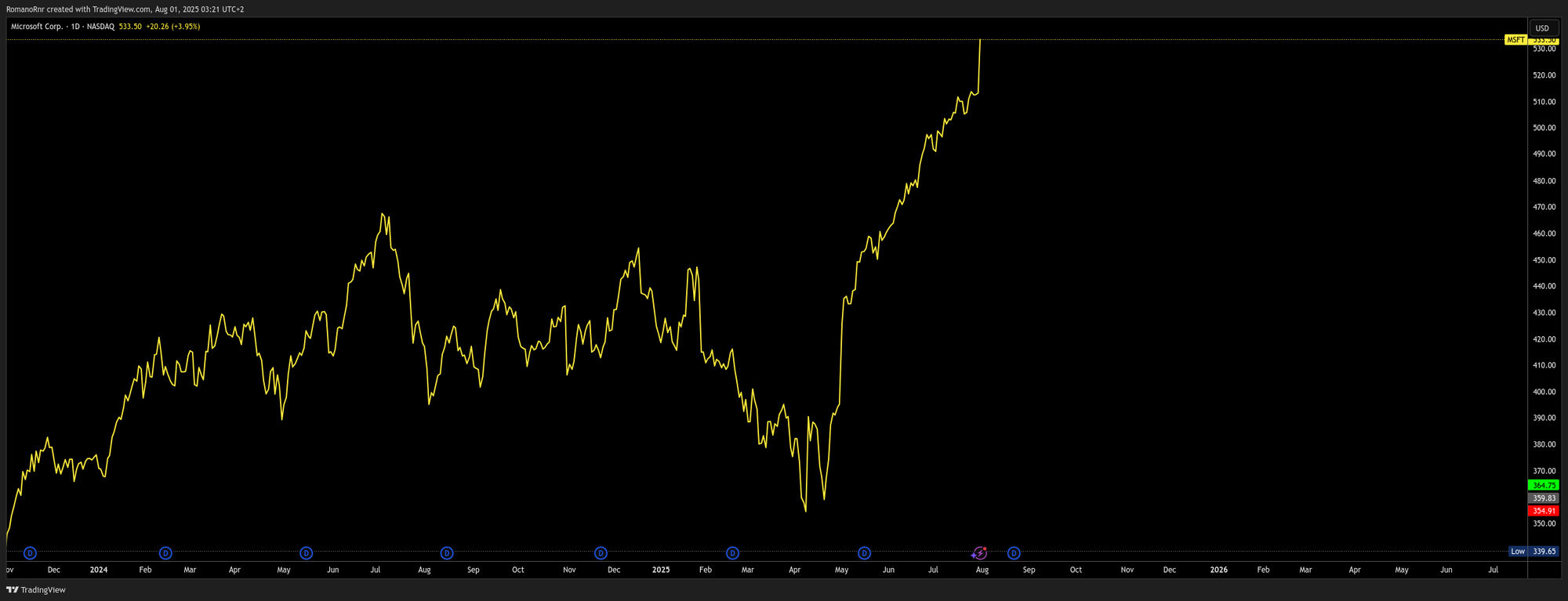

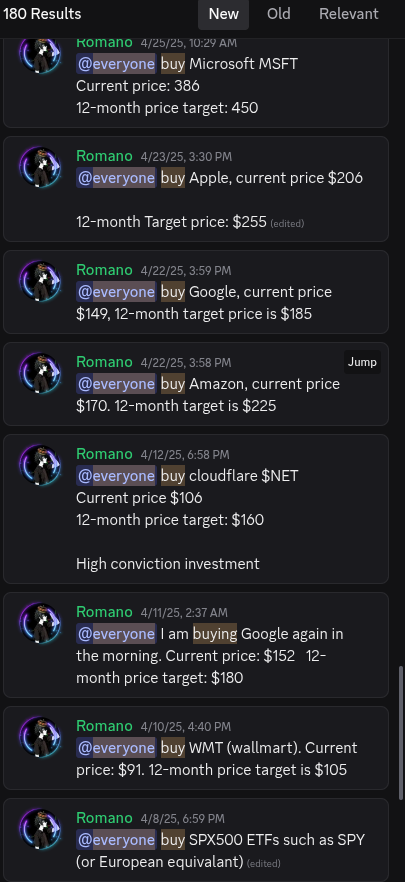

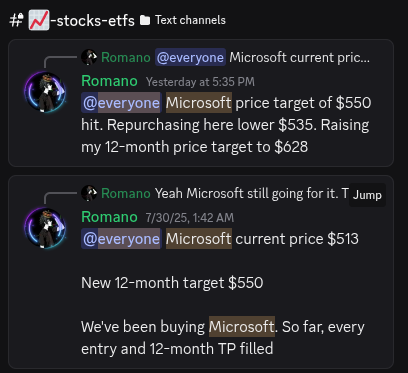

.... There's this one latest Microsoft call I made. The $513 to $550 trade worked out within 24 hours. I bought lower at at $535 gunning for $2628

I am having some second thoughts about it, the rally been a vertical one. Seems a little bit 'too perfect'