Market view May 19, 2022

Futures for the SPX500 have fallen to $3882, up from overnight lows of $3850. This indicates that the market is down from its previous peak but up from its overnight low.

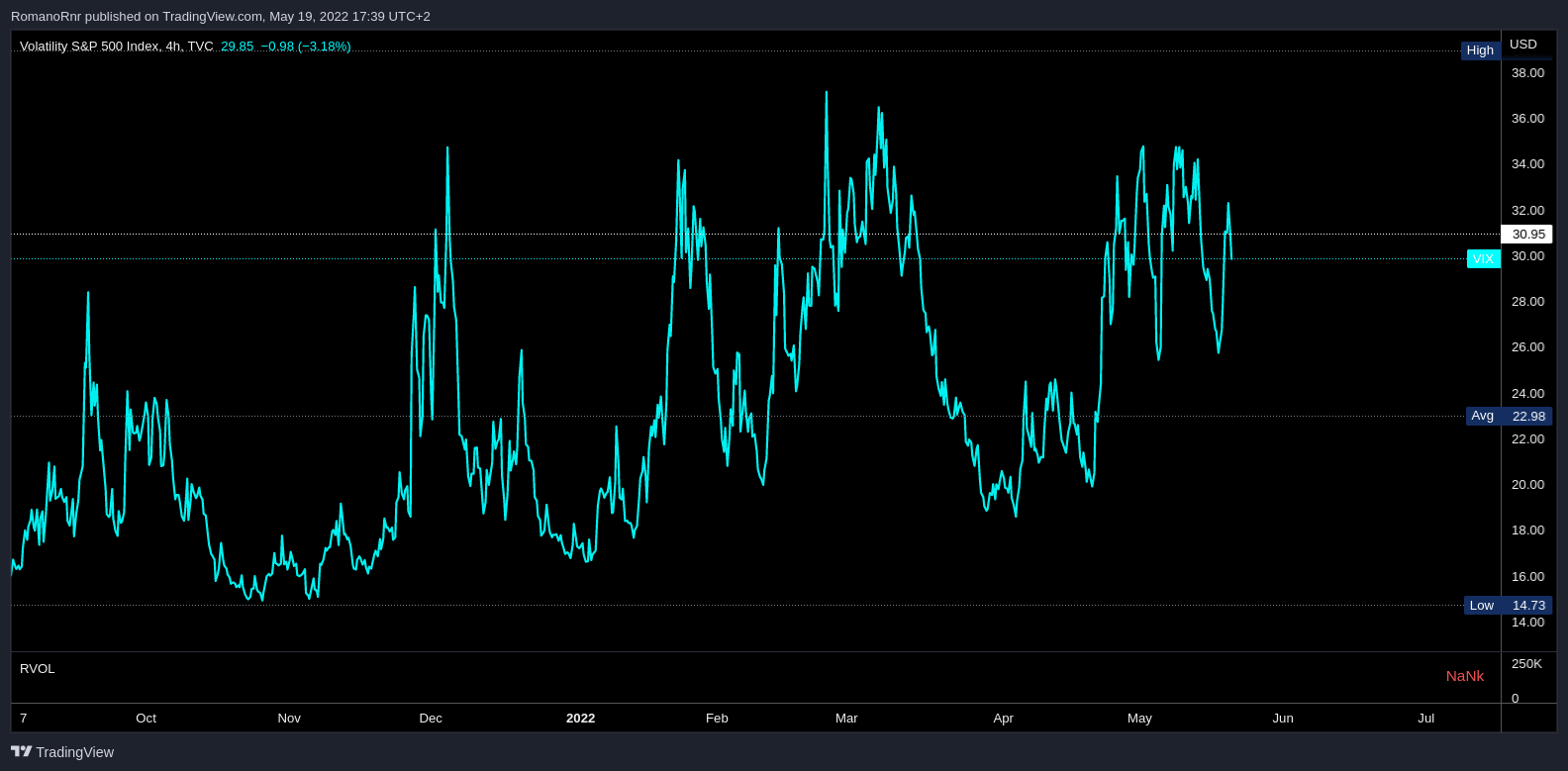

The VIX is pricing daily SPX500 changes of 2%, which indicates that there is still a great deal of unpredictability in the market, and prices may continue to vary dramatically.

Resistance for the S&P500 is at $4000.

Hedging flows

When markets go down, options hedging flows will likely sell as well. When the market falls, short-dated "put options" increase in value.

So, if large short-dated "put option" positions are 2% "out-of-the-money", they will become 2% "in-the-money".

That means that there is a risk that the options will "jump" in value, which would cause the price of the options to increase.

If you want to learn more about options trading, I wrote a comprehensive guide/article

https://romanornr.medium.com/options-trading-fd4d0bffb2c5

The short-dated "put options' increase in value would cause the stock market to drop further.

When the "put options" increase in value, it means that there is more downside protection in the market.

This increased downside protection means that investors are less likely to want to buy stocks and more likely to sell them. This selling pressure can cause the stock market to drop further.

When dealers/market makers reduce their selling or become buyers, the options flow will become the dominating factor.

That will happen when the underlying asset price falls below a particular level. At that time, sellers will be unwilling to sell further, and buyers will be more likely to enter the market.

Importantly, when "puts" are rolled down and out, the amount of support gradually changes to the left (as in lower strike prices)

Tomorrow OPEX May 20

The equity options expiration tomorrow has become more interesting due to the market decline adding more delta weight.

That means options traders have more incentive to buy back their sold options (to close out their positions) after the expiration. That could provide a relief rally into Friday/Monday.

Tomorrow equity OPEX (which is the expiration of options on stocks and ETFs) has become more interesting because the market has declined, adding more "delta weight" (the sensitivity of the option price to changes in the underlying security).

Delta notional is the total value of all the options contracts with a particular strike price.

The 5/20 expiration has a lot of put delta, which signals that there could be a relief rally (a period of upward price movement) into Friday/Monday as people who are short hedges (bets that the market will go down) cover their positions.

The June expiration is also a significant event, as it is much larger than usual.

The market is likely to rebound to the 4000 level around Friday's expiration, as there is significant resistance at that level.

However, any rally should be seen as short-covering and subject to quick reversals. A new market low is likely to occur with a quarterly OPEX and FOMC.

I might start blogging more. You can subscribe to this blog for updates if you enjoyed this post or think it's interesting enough