Market view May 20, 2022 (OPEX)

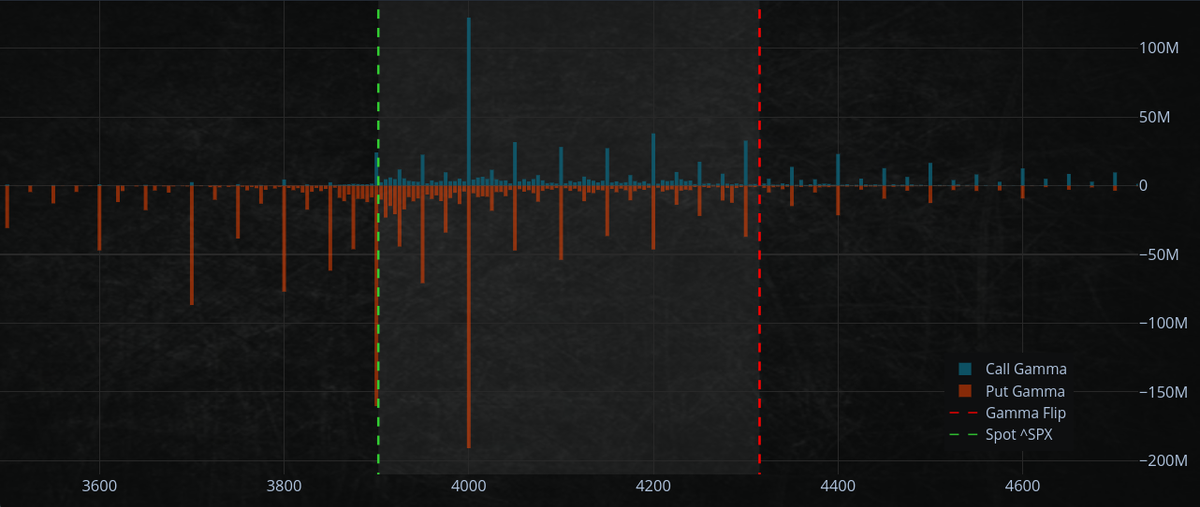

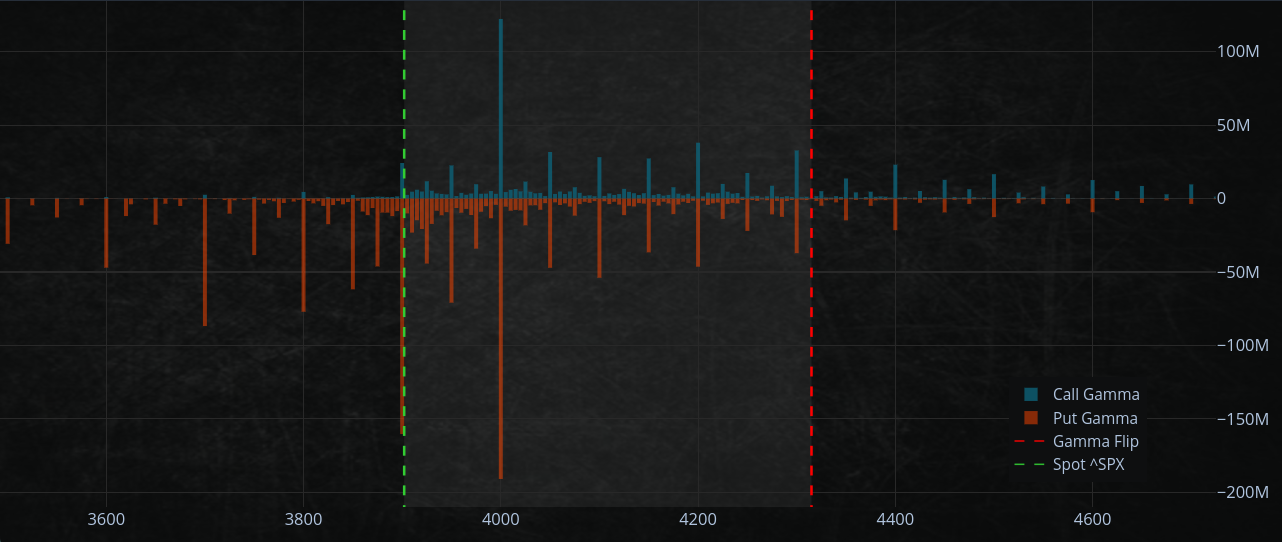

The SPX500 supported our $3,900.00 region, produced by the "strike price" with the largest net-negative gamma.

Gamma is a measure of the rate of change of an option's delta in relation to the underlying asset.

In general, the greater the gamma of an option, the greater the change in delta relative to the underlying asset.

A put option with a significant net-negative gamma will have a greater delta, making it more likely to move "in the money" when the underlying asset's price declines. That makes $3900 a crucial level of support.

If you want to learn more about options trading, I wrote a comprehensive guide/article

Also follow me on medium and turn on email notifications for par 2 of options trading

https://romanornr.medium.com/options-trading-fd4d0bffb2c5

VIX

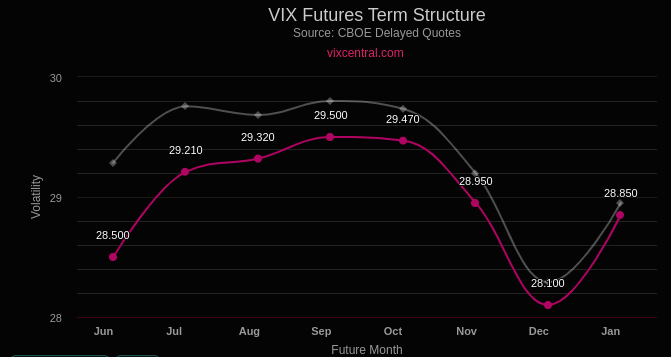

The VIX index (a measure of implied volatility) decreased by 5%.

Based on the compression of the volatility term structure, especially at the front end of the curve, delta hedging flows concerning changes in volatility (Vanna) supported today's $3900 support level.

That indicates that the VIX decreased by 5% due to a "compression" in the volatility term structure.

The decline occurred (i.e., the difference between longer-term and shorter-term volatility measures fell).

This compression was most evident near the beginning of the curve (i.e., the shortest-term measures of volatility).

Hedging flows

Delta hedging is a method traders/dealers employ to reduce the risk associated with their bets. With options trading, delta hedging is when traders/dealers buy or sell options to mitigate their underlying position's risk.

In this instance, traders purchased options to hedge against the potential of declining volatility.

The Vanna flow quantifies the change in the "delta" of an option position in response to the underlying asset price change.

In this instance, the Vanna flow was positive, indicating that the delta of the option position grew as the underlying asset price (the VIX) decreased.

Volatility

the market's volatility is beyond what is "implied." That's likely because many market participants hedged against potential losses.

When the market starts to decline, these participants can sell their hedges for a profit, which in turn suppresses the market's volatility.

Vanna

Currently, the market lacks the "Vanna fuel" that has historically supported it during times of turbulence.

This lack of support reduces the pressure on liquidity providers, which may provide an opportunity for the market to rise.

However, this window is just brief, and it is doubtful that the market will continue a rally for an extended period until the underlying situation changes.

Watch technical levels for attitude shifts among market players. If prices begin to rise, relief rallies would probably gain momentum.

Due to a major expiry, May 20 (20220) is an important day for markets.

Rallies into OPEX should be labeled "short covering" since they are prone to significant reversals.

You can subscribe to this blog and receive email notifications