Market insight May 25, 2022

SPX500

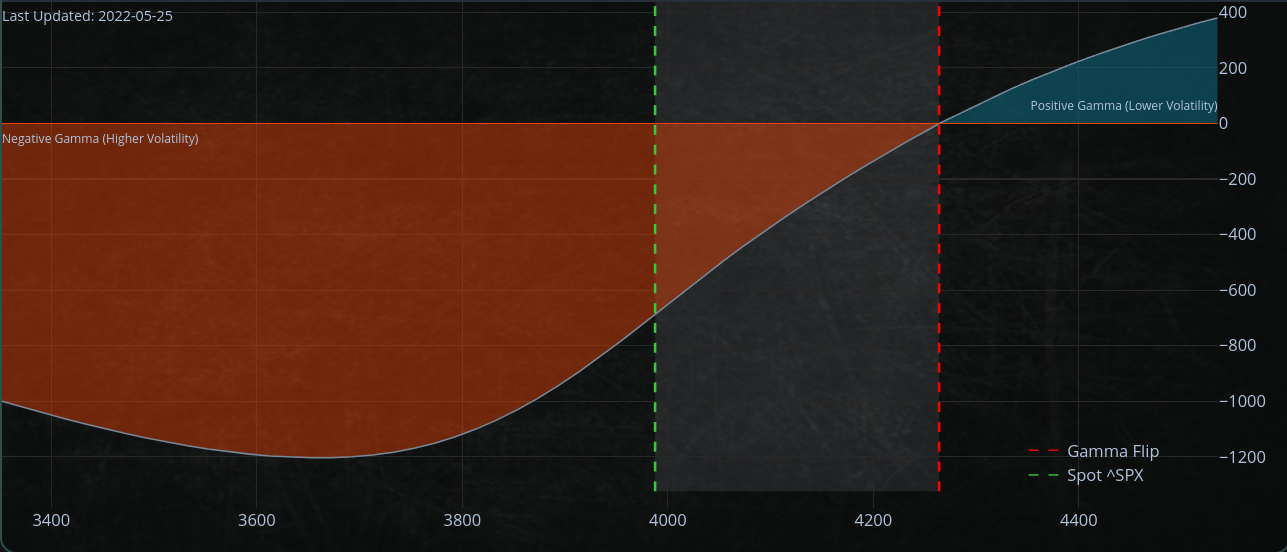

The market's low point was $3880. That was expected, with a strong bounce, as I mentioned in my previous blog post yesterday.

The elimination of put-heavy option contract exposure after the expiration of options contracts (OPEX) may create a market with less pressure to rally.

Put-heavy exposure? Yeah, allow me to explain...

Put-heavy exposure is when there are more put options contracts than call options contracts.

That can happen after the expiration of options contracts because investors betting that the market would fall may try to buy back their contracts to avoid making a loss. That can create downward pressure on the market.

But the elimination of these "put-heavy contracts" means that any rally that does occur after OPEX is likely to be due to short-covering

For example, investors who had bet that the market would decline by repurchasing their contracts to avoid suffering a loss). Therefore it may be short-lived.

Support may be in the $3700-$3800 since that's where the slope of the curve starts to flatten.

Numerous market players feel that the expiry of options contracts ("OPEX") might generate selling pressure when market makers adjust their portfolios to reflect the new delta. This selling pressure might temporarily halt any efforts at a rally.

However, any rallies that do occur during OPEX should be labeled short-covering and are therefore met with sharp reversals.

If you want to learn more about options trading, I wrote a comprehensive guide/article

https://romanornr.medium.com/options-trading-fd4d0bffb2c5

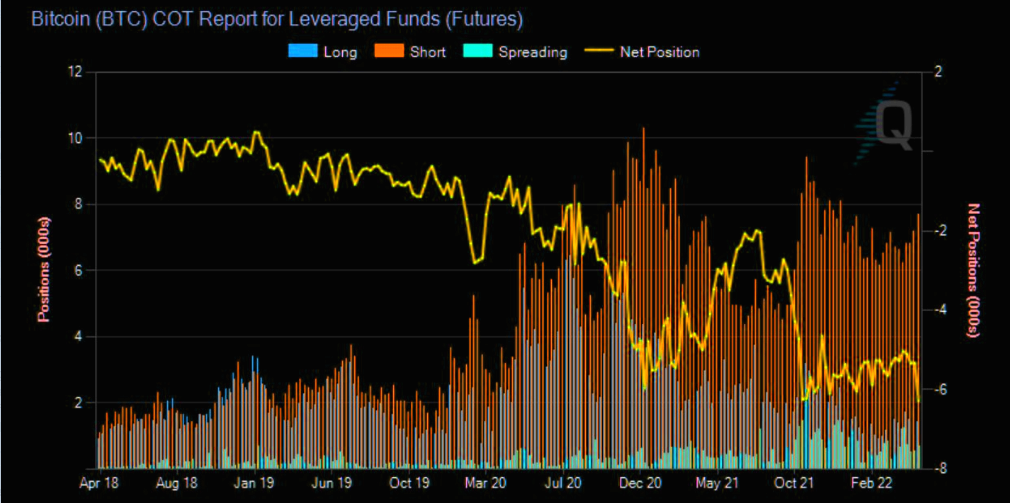

bitcoin

The CME (Chicago Mercantile Exchange) is a financial derivatives exchange where Bitcoin futures contracts trade

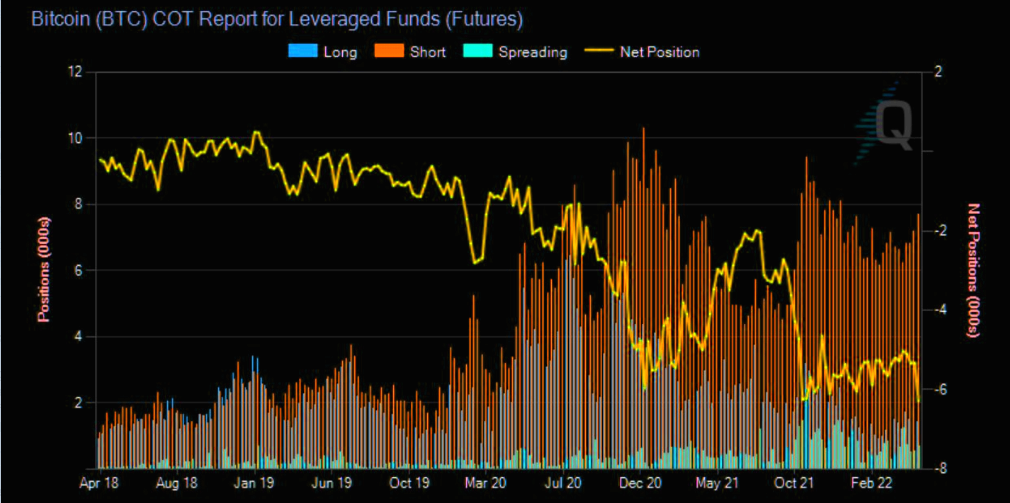

"Leveraged position net specs" refers to the net position of all leveraged traders (hedge funds and commodity trading advisors / CTAs) combined.

The all-time high in short exposure means that these traders are currently more bearish on Bitcoin than they have ever been before.

That is more extreme than the time series suggests because previous highs have coincided with higher interest rates (the "carry trade"). With interest rates now near zero, there is much less incentive to be bearish on Bitcoin?

If the Nasdaq were to reverse and start going higher from its current level, Bitcoin would likely do the same.

CME leveraged position net specs (hedge fund/CTA) have reached an all time high in short exposure. this is more extreme than the time series alone suggests because previous highs have coincided with double digit carry available. with basis now <2% views are likely directional. pic.twitter.com/oS1jLI1Un3

— bithedge (@bit_hedge) May 24, 2022

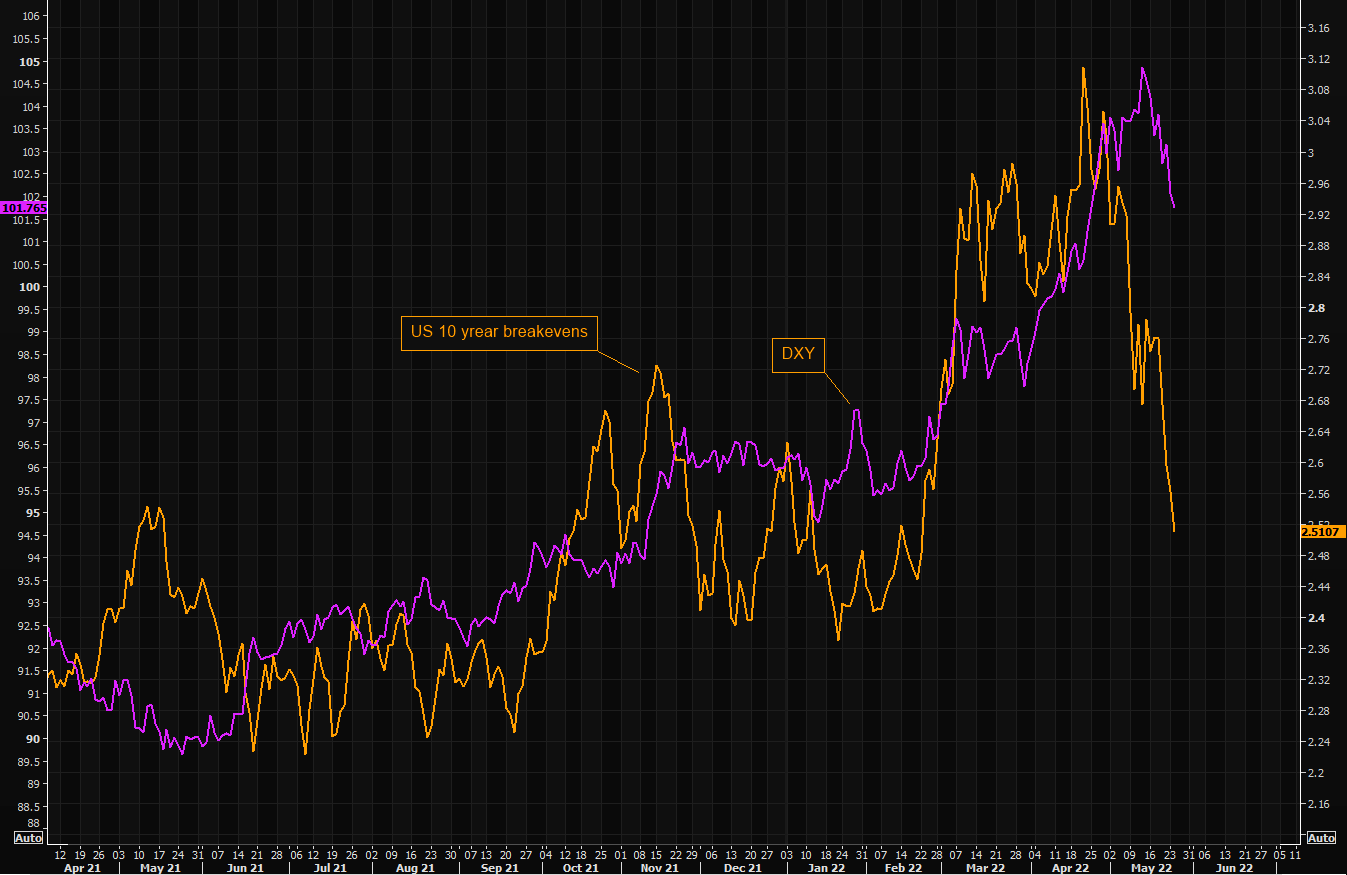

US 10-year breakeven vs. DXY

US 10-year break evens measure the market's expectation for average inflation over the next ten years. They have fallen sharply lately, meaning that the market is expecting less inflation in the future. This is likely due to concerns about the global economy, as well as oil prices.