Inflation Under Control: Now What? SPX500 ATH EOY? 🚨

The NATO meeting didn't meet the expectations of most participants, except maybe Sweden. Ukraine was disappointed by the lack of a clear timeline for its membership application, even though NATO allies agreed to train Ukrainian pilots on the F16 fighter yet.

However, some NATO members seemed annoyed by Zelensky's request for more and better equipment.

The UK defense secretary said, "We're not Amazon," implying that Ukraine had a long and unrealistic wish list and asked for some "gratitude."

I guess they were trying to be funny by mentioning "Amazon" because they were having their big Prime Day sale, where people buy a lot of stuff online. But NATO is not ready to give Ukraine the Prime status they want, so it's not really a good joke.

I'm not a fan of Zelensky, but it was kind of a "dick joke" to make in public, considering Ukraine's dire situation and being put on the spot like that. Maybe they thought Zelensky would take the joke well because he's a comedian. I think they could have phrased it more professionally.

While it is likely that the limited availability of military equipment is the real cause of the frustration, the defense secretary's mention of Amazon was telling.

At the same time as the meeting was taking place was the US e-commerce giant's Prime Day sale, showing the disparity between the power dynamics of NATO states. While Ukraine is still waiting to receive an invitation to join NATO as a full member, Amazon customers increased US online sales even further.

Okay, okay, since it actually was a Prime Day sale on amazon.com, I'm not going to lie here. I guess that joke made it somewhat fire.

Things to cover:

- CPI

- Interest rates

- XRP/Ripple

- Goldman Sachs Flood thinks SPX500 new ATH EOY

- Ripple

- Reserves

- Federal Reserve Balance Sheet & Nasdaq

- Seasonality

- VIX

- Hedging risk

- SXE5

Upwards & onwards

Also, let's cover the CPI print, which happened, and I covered that in the previous newsletter.

represent

Content from the previous post. Click here to toggle

- If inflation is higher than 0.5%, it's not great news. The SPX500 could drop at least 2% (not super likely, though, only a 5% chance).

- If inflation is between 0.4% - 0.5%, the SPX500 might fall somewhere between 1% - 2% (a bit more likely, with a 10% chance).

- If inflation is between 0.3% - 0.39%, we might see the SPX500 drop anywhere from 0% - 1% (this is pretty likely, with a 30% chance).

- If inflation is between 0.2% - 0.29%, we could see the SPX500 rise slightly, from 0% to 1% (even more likely, with a 35% chance).

- If inflation is between 0.1% - 0.19%, the SPX500 will jump by at least 1% (less likely, but still possible, with a 15% chance).

- If inflation is less than 0.1%, the S&P could take off, going up at least 1.75% (but this is pretty unlikely, with only a 5% chance).

- [5% chance] Headline YoY prints 3.7% or more: This would be an uncomfortable scenario because that would imply that inflation is seriously picking up. If that's the case, we will probably see a rise in bond yields and volatility. That can follow up with a sell-off in the equities market. It wouldn't be a surprise if the Federal Reserve hikes rates by another 50 bps in July and some more hike rates later this year. The SPX500 may likely fall by around 2% or 2.5%

- [15% chance] If inflation is between 3.3 - 3.6%: That wouldn't do much to calm worries about the Federal Reserve ending rate hikes soon. Plus, rising energy prices this summer and still robust consumer spending could cast doubt on inflation forecasts. That would push the bond market to expect more rate hikes. The SPX500 may drop 1% - 1.25%

- [45% chance] If inflation is between 3.0% - 3.2%: This is what most people expect to happen, although some folks are whispering about a sub-3% inflation. This would represent a substantial decrease in inflation, supporting the narrative that inflation is slowing down. But it's unlikely to stop the Federal Reserve from raising rates by 0.25% in July. It might, however, stop further rate hikes for the rest of the year. The SPX500 might jump by 0.50% - 0.75%

- [25% chance] If inflation is between 2.8% - 2.9%: The big drop in inflation would be the largest in this cycle. Given recent trends, this could reset expectations for inflation to stay below 3%. If that happens, we could see fewer expectations for rate hikes in July. This might lead to the Fed doing another "hawkish skip," particularly if inflation normalizes before we feel the full effects of the tightening cycle. We could even see the end of the tightening cycle in late August. This would be a "Goldilocks" scenario - growth without inflation, just like in pre-COVID times. The SPX500 might jump by 1.5% - 1.75%

- [10% chance] If inflation is 2.7% or lower: This is a pretty unlikely but interesting scenario. Real-time inflation indicators suggest that headline numbers might even be below 2.5%. If this happens, we'd probably see the July rate hike taken off the table, and we might even see rate cuts in late 2023. The Fed could then focus more on full employment and financial stability, both of which would benefit from lower rates. This could lead to a bull market for both stocks and bonds. The SPX might even jump by 2.5% - 3%

The result highest probability outcomes were the actual results. It was better than the forecasts, and the SPX500 did indeed jump.

Also, EURUSD went up, as mentioned in this newsletter: https://www.romanornr.io/fx-dollar-downtrend-pause-eurusd-forecast-06-07-2023/,

The chair of the Federal Reserve, Jerome Powell, has stated that the US central bank need not rush to raise interest rates and could even skip the upcoming September meeting, citing a slowing economy and low inflation as appropriate reasons.

Yesterday, the markets were propped up by the Fed's view, which saw a reduced risk of policy mistakes. Bond yields for 3-year maturity fell, indicating lower expectations of future rate hikes. The US dollar weakened against several currencies, while the euro rose to its highest in a year, above 1.115.

However, the European Central Bank (ECB) is not expected to adopt a more dovish stance. The ECB is still expected to increase interest rates twice more, but there is less certainty. This could be due to the US inflation data, which showed a lower-than-expected increase in consumer prices. It could also be due to the draft statement from the Eurogroup, which is the meeting of the finance ministers of the eurozone countries.

The draft statement states that eurozone governments will gradually reduce budget deficits instead of providing extra spending on energy to support their economies. This move will assist the ECB in fighting inflation, which is its primary goal.

The ECB has been requesting this for some time because it believes excessive fiscal stimulus complicates its job. The Eurogroup's decision could ease some of the upward pressure on inflation in the eurozone. Still, it is unclear how much it will affect the ECB's forecasts since the draft statement does not specify when the fiscal support will end. As a result, we don't know how quickly or jointly the eurozone governments will tighten their fiscal policies. Additionally, we don't know how the ECB will react to this change in fiscal stance or whether it will adjust its own monetary policy accordingly.

The Market's Shift Towards Lower Interest Rates

The 10-year Treasury yield recently hit 4%, but the game changed when the recent CPI data showed only a 3% increase, just shy of dipping into the 2% zone.

Also, the core inflation rate, which doesn't count food and energy (since they're too volatile), dropped under 5% for the first time in like a year and a half.

This is great news for inflation. It seems to be impacting the market by leaning towards lower rates. The 10-year US Treasury yield dropped under 3.9%, and the 2-year yield is hovering around 4.70%. Also, the yield curve is un-inverted or bull-steepened, which usually happens as we near the end of a period of rate increases.

Both real yields and inflation expectations are decreasing; the 2-year breakeven rate, the market's guess at future inflation, is now below 2%. The Federal Reserve may be pleased.

Before continuing to read, subscribe to the premium newsletter. The premium package also includes full access to my Discord.

Anyways you can continue to read further. The article does NOT stop here.

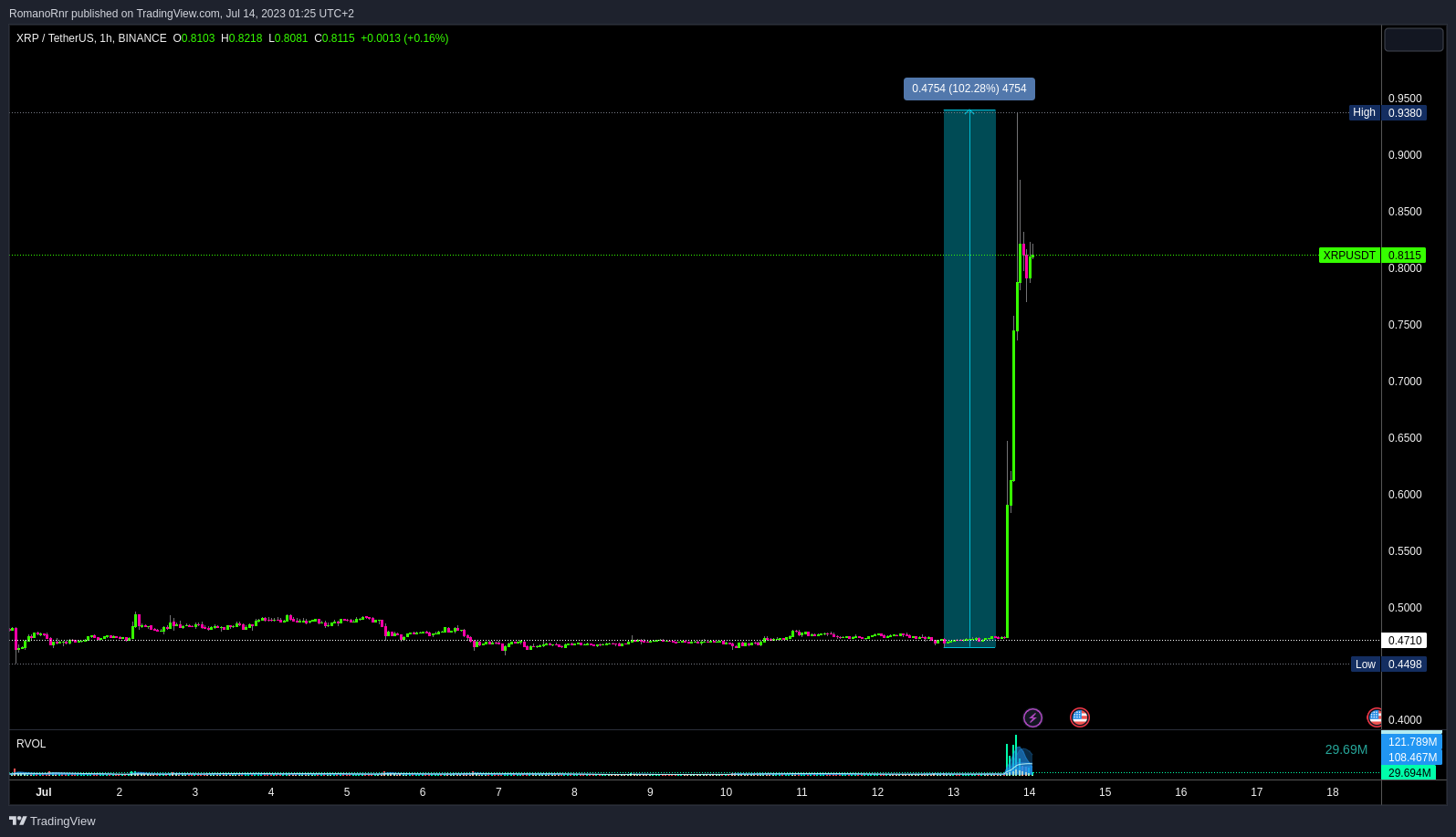

XRP/Ripple

The news broke out about the court ruling affecting the status of Ripple's XRP token, a cryptocurrency used for cross-border payments.

The ruling states that XRP is considered a security and subject to federal regulations when sold to institutional investors like hedge funds or banks.

But here's where it gets interesting - XRP is not considered a 'security' when sold to retail like you and me on exchanges or via algorithms.

This is a bit of a win for the Securities and Exchange Commission (SEC), which sued Ripple in 2020 for selling what they believed were unregistered securities and tricking investors.

This is a partial victory for the SEC, which sued Ripple in 2020 for selling unregistered securities and deceiving investors. The case will proceed to trial to determine other allegations.

Bitcoin-related stocks saw a nice bump (the term 'green shoots' is used to refer to signs of growth or recovery) after a significant headline hit the news. The headline was about Ripple, another type of cryptocurrency, which a judge ruled is considered a 'security' in institutional sales.

This ruling seemed to positively affect the market, with the GSCBBTC1 (a benchmark that tracks Bitcoin-sensitive stocks) finishing up a whopping 13.43%.

Even more striking, specific stocks soared after this news. 'COIN' (which probably refers to Coinbase, a cryptocurrency exchange) jumped a massive 25%. RIOT (Riot Blockchain, a company that invests in blockchain technologies) and MARA (Marathon Digital Holdings, a digital asset technology company) both saw a 15% increase.

Good news for Ripple that seemed to give Bitcoin, related stocks & altcoins a big boost

Do you want to know something funny?

S&P500 is trading more than 3% higher compared to March 2022, when the Federal Reserve started hiking rates

Goldman Sachs' Jon Flood suggests the S&P 500 is currently 3% higher than when the Federal Reserve began increasing interest rates in March 2022. Despite the increase in interest rates, which is generally viewed as a way to slow down economic activity and control inflation, the S&P 500 has managed to rise, indicating resilience in the market.

Multiple clients are asking Flood if the S&P 500 will reach an all-time high by year-end 2023. Flood responds positively with a "Yes," showing confidence in the market's momentum.

Corporate earnings season is approaching with relatively modest expectations. This may benefit the market, as companies could easily surpass these lower expectations, potentially boosting their stock prices and the overall S&P 500 index.

GS Flood suggests the S&P 500 could reach an all-time high despite challenges, especially if companies exceed low expectations during earnings season.

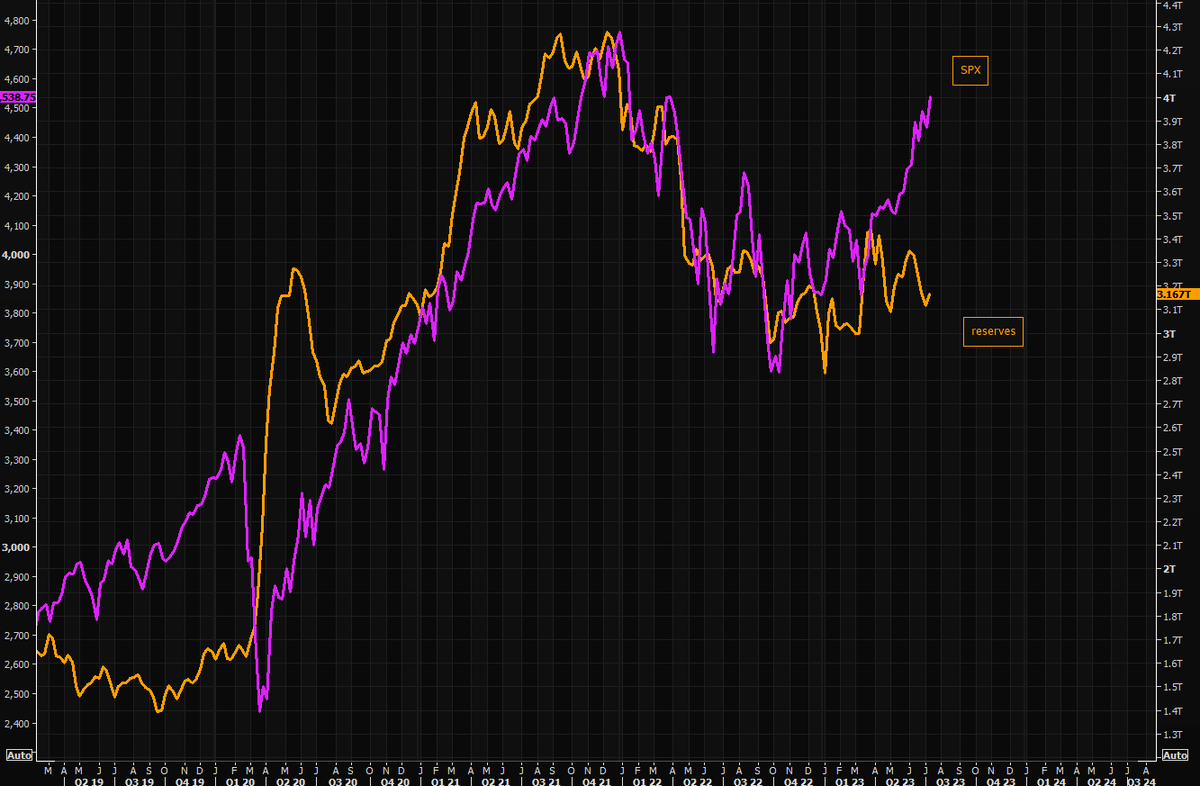

Reserves

This chart depicts the relationship between the S&P 500 and the Federal Reserve's balance sheet.

There seems to be some temporary "decoupling" ongoing. The S&P500 is no longer moving in the same direction as the Federal Reserve's balance sheet since the most recent squeeze, which has broken many relationships/correlations

Will the SPX500 mean revert? Do Reserves still matter? I guess we will figure that out soon enough.

Also, some "decoupling" Nasdaq and the Federal Reserve Balance Sheet, see graph below which is really interesting.

It seems like the NASDAQ has said, "See ya later virgins" & shot up on its own, leaving the Federal Reserve's balance sheet behind.

The gap you're referring to is the difference between the two lines on the chart. It's been ages since you've seen such a large gap in such a short time.