Cutting Into Strength

The market expects the Fed to start easing rates, not because of a crisis, but while stocks and GDP are growing. That's rare, but hear me out.

As long as the Fed is cutting into strength, the market's instinct is to chase risk higher.

The risk-off isn't economic collapse right now, but political/event risk next spring. Remain overweight/bullish on U.S equities (especially quality/growth tech)

Don't fade this tape until you see

- Fed credibility going down the drain (i.e., inflation spike or cuts due to crisis)

- Credit stress (tech IG spreads)

Europe was the spring trade, Chinese stocks were the summer trade, and Japan would be the autumn trade

Earnings seasons and cyclical strength in Europe, stimulus and reopening in China, and valuation/corporate action, along with FX tailwinds.

Japan has been the beneficiary of reflation and currency dynamics that make exporters and corporate governance stories attractive. You can see reporting this year about Japan moving into a reflationary/reward phase

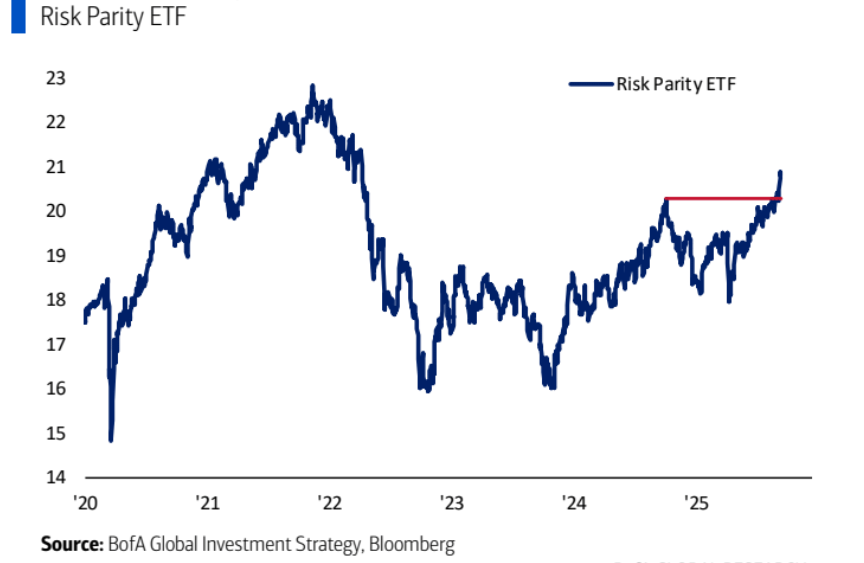

Risk Parity

This chart shows the Risk Parity ETF, which is designed to balance between stocks and bonds. When both of these asset classes are doing well at the same time, the ETF tends to go up.

In the past few years, you can see how it went up strongly in 2021, then dropped sharply when inflation went up and the Federal Reserve started hiking rates. That period was painful for both stocks and bonds, so the risk parity strategy struggled.

In 2024-2025, the ETF has climbed back and broken above its previous high from 2024. That's an important signal that makes investors believe conditions are shifting in a more favorable way. Specifically, it suggests the market thinks the Federal Reserve can begin cutting interest rates without losing credibility. Investors won't see the cuts as a sign of panic or weakness, they believe it will support the economy and re-accelerate growth even further beyond.

Markets are pricing in a "sweet spot" where inflation is no longer the dominant risk, growth is picking up again, and the Federal Reserve can ease policy in a way that benefits both equities and bonds. This is the opposite of a panic cut.

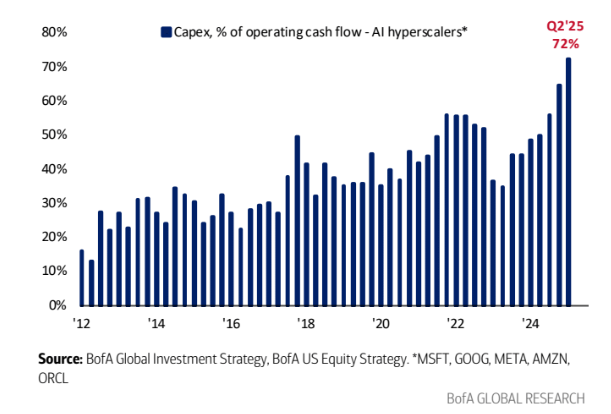

Hyperscaler

The credit markets are signaling confidence in big tech's ability to manage massive AI investments.

One of the clearest signs of how big the AI wave has become is the scale of spending by tech giants.

Microsoft, Google, Meta, Amazon, and Oracle are all pouring massive amounts of money into data centers, chips, and cloud infrastructure to get that AI demand.

In the second quarter of 2025, these hyperscalers spent ~72% of their operating cash flow on capital expenditure. To put that in perspective, just 2 years ago, the figure was closer to 35%.

So that means more than 2/3 of every dollar they generate in cash is being reinvested straight back into building out AI capacity.

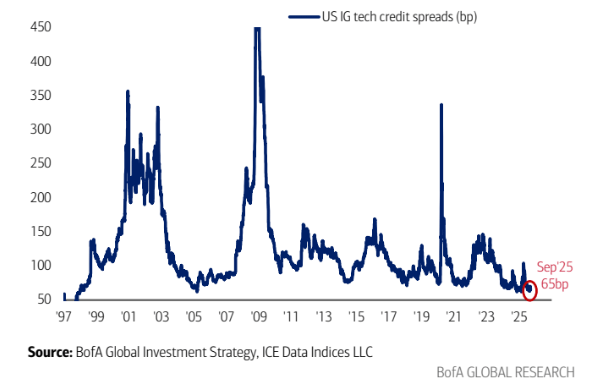

Normally, when companies double their investment spending quickly, bondholders often get worried. Investors prefer steady cash flow and small amounts of debt. If companies are burning cash on big mega projects, the extra interest they must pay to attract investors (spreads) tends to increase. A wider spread means higher borrowing costs and shows that investors see more risk.

But that's not what's happening today. The credit spread on investment-grade tech bonds is near its tightest levels since 1997, sitting at just 65 basis points in September 2025.

In other words, the bond market is relaxed. Investors are essentially saying that they trust these companies to fund massive AI investments without turning their balance sheet into a mess.

Sooooo..... on the one hand, you have a record-high capital spending that looks extreme by any historical standard.

On the other hand, you have a credit market signaling almost no fear, pricing tech debt as among the safest corporate paper around.

As long as spreads remain tight, the AI spending boom will be financed at unusually easy terms. Markets are giving hyperscalers a long leash to spend aggressively without penalty. Second, if the spreads were to widen meaningfully from here, it would be a warning sign that bond investors are starting to question the sustainability of the AI cash burn.

For now, credit markets are calm.

Hyperscalers are still generating massive free cash flows, even post-capex. They have a strong balance sheet, a high-margin business, and diversified revenue streams.

Unlike unprofitable startups and chains with near $0 revenue, these are profitable incumbents reinvesting for long-term moat expansion, not survival.

The likelihood of default is extremely low. You don't really think about Google defaulting and your Gmail being gone.

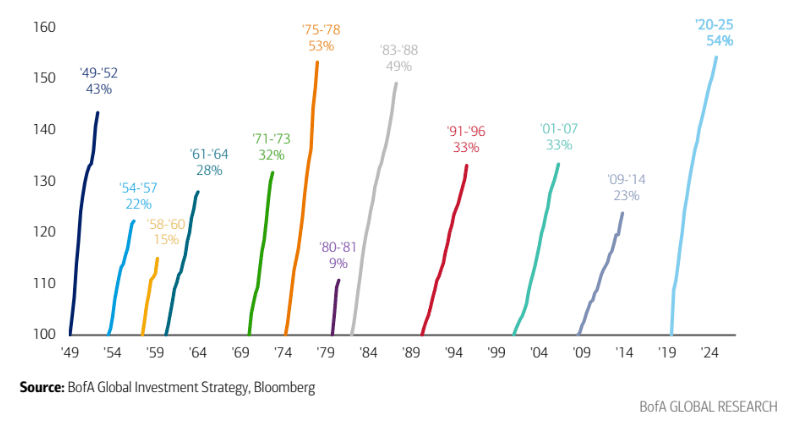

GDP growth cycle strongest since WW2

Since 2020, the U.S. economy has been on a tear. Fueled by trillions in stimulus and the post-pandemic boom. Nominal GDP up over 54% which is the fastest growth cycle since World War 2.

Thinking about what happened. Inflation went up, corporate profits ballooned, and investors piled into everything except bonds. Small caps, crypto, value stocks, and commodities.

Like all good things, it must come to an end. The government spending is cooling down, the labor market is softening, and nominal GDP is expected to downshift from 6% to around 4% annually. That's decent, but in macro terms, it's a slowdown

Historically, bond yields tend to speak when nominal GDP does, and we're likely at that point. The 10-year Treasury may have topped out, and with it, the case for "not buying bonds" starts to crack a bit.

If yields are done rising, the entire market playbook begins to flip. The hard asset trades that thrived on inflation and rate hikes may lose their shine.

Instead, long-duration assets like bonds and big tech could take that spotlight.

Is the Fed ahead of the curve?

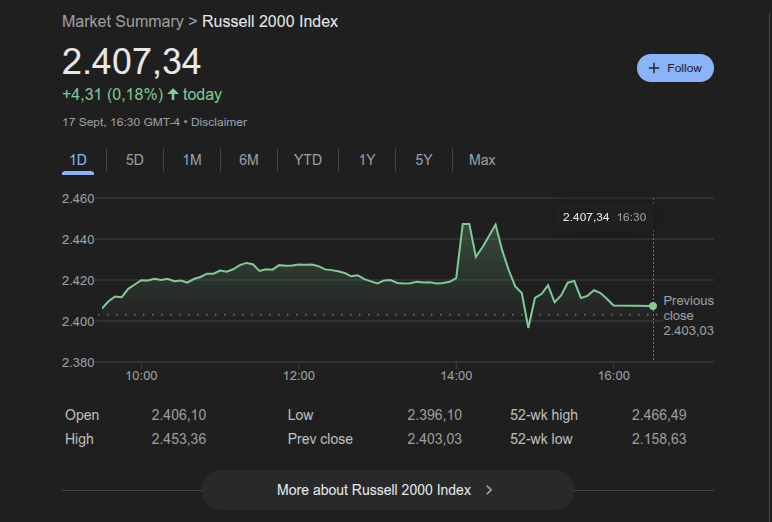

Markets are lining up for Fed rate cuts, and now investors are treating those cuts as "ahead of the curve," and that's why we've seen tighter credit spreads, bids into bank stocks, and strength across rate-sensitive equities like small caps and home builders. The market views an easier policy as a stabilizer, not a red flag.

But there's a line in the sand. If investment grade credit spreads widen past 60bps, if bank stocks BKX break below 140, or if the Russell2000 can't clear 2400, then the narrative flips.

That would mean the Fed isn't cushioning the economy but rather cutting into weakness.

The labor market is clearly softening as payrolls have averaged just 64k over the past six months, which is the weakest run since 2020. Normally, that would weigh heavily on earnings expectations, but the drag is being offset, at least for now, by a powerful K-shaped wealth effect. Equity markets delivered a massive boost to household balance sheets.

A K-shape wealth effect means that the benefits of rising asset prices aren't spread evenly, but are unevenly distributed across different groups of people, just like the diverging arms of the letter K.

Upper arm of the K: Wealthier households that already own lots of equities have seen their portfolios go up. That gives them more confidence to spend even if wages or jobs are soft.

Lower arm of the K: Lower-and middle-income households who have less exposure to equities and rely more on wages are not benefiting in the same way. For them, the labor market slowdown (fewer payroll gains, weaker income growth) hurts them directly.

Join Discord

Become a Premium member. Premium newsletters & Discord community access

Become a Premium member. Premium newsletters & Discord community access

50% discount forever on yearly subscription