The Invisible Hand Meets the Visible Fist: Yield Curve Control

Over the last century, there have been 14 major bull markets in US equities.

On average, those cycles have lasted just under 5 years and delivered 177% gains.

S&P500 could go over ~9000 by the end of 2027

Actually, if we project that same trajectory onto today, we arrive at a number close to 10,000 on the S&P500 within 2 or 2 and a half years.

This isn't a guarantee, as crashes, recessions, and shocks can and might happen along the way.

Even if we do see cracks, particularly in the bond markets, central banks are unlikely to just stand by. They will probably resort to yield curve control.

HELLO GEN Z Brainrotted Reader

DOES THIS FORMAT HELP WITH THE ATTENTION SPAN?

Vote yes to have text in this format next time

Anyways, back to business

What is Yield Curve Control?

Yield curve control, or YCC, is a form of monetary policy in which central banks set a target for government bond yields at certain maturities and then buy or sell bonds in whatever amount is needed to keep yields pinned at that level.

Instead of just adjusting short-term interest rates, the central bank essentially takes over part of the long end of the curve, deciding how much it will allow 10-year or 30-year borrowing costs to rise.

Japan has used this approach for years, keeping its 10-year government bond yield near zero by intervening whenever the market tries to push it higher.

The idea is that by controlling yields directly, the central bank prevents borrowing costs from spiraling, supports government financing needs, and indirectly props up risk assets like equities.

The downside is that it does undermine a "free" bond market, since prices and yields are no longer determined by supply and demand but by the central bank's decree.

If bond markets start to break under the weight of debt and rising rates, the Federal Reserve might have no choice but to follow Japan's playbook. That would remove one of the natural checks on equities' exuberance and could paradoxically help to fuel the kind of long, extended bull run we hope for.

Right now, yields on long-dated government bonds are hitting multi-decade highs across the developed world. Like ~5.6% on the UK long bond, 4.4% on France, and 3.2% on Japan, and nearly 5% on the US 30-year.

Normally, this jump in yields should terrify investors since it raises the cost of capital, pressures corporate profits, and tightens financial conditions. Stocks are not panicking. Instead, they're behaving as if they expect the central bank to intervene.

Become a Premium member. Premium newsletters & Discord community access

Price keeping operations?

Yield Curve Control, quantitative easing, or something like Operation Twist, all of which have the goal of stopping borrowing costs from rising too much or too fast.

The markets are discounting that the "invisible hand" of the free market is going to be replaced by the "visible fist" of central bank intervention.

If that happens, certain trades are going to be obvious

Long gold because yields and real rates falling make non-yielding stores of value more attractive.

Expect the stock market rally to broaden beyond big tech names into bond-sensitive sectors, such as biotech, real estate investment trusts, and small caps.

More generally, look for the same liquidity-driven surge into crypto and other hard assets that we've seen in the past easing cycles.

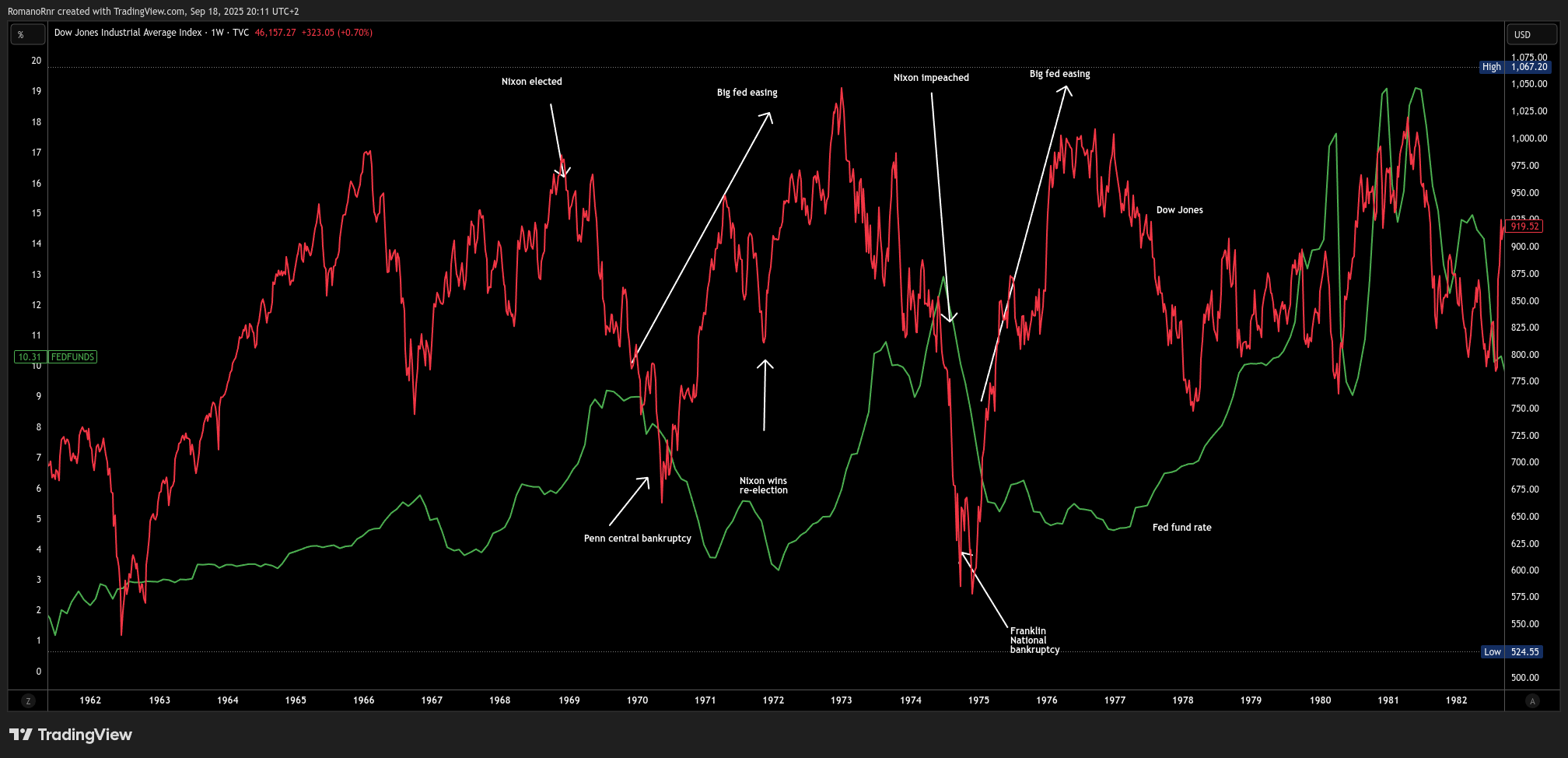

Historically, the closest precedent is the Nixon era in the early 1970s. That was a time when political pressure weighed heavily on the Fed, exchange rates were manipulated to favor domestic growth, and the White House wanted looser financial conditions to juice the economy ahead of an election.

The 1970s followed a long, stable secular expansion in both stocks and bonds during the 1950s and 1960s. Investors got used to prosperity, strong productivity, and manageable inflation.

Then came a decade of shocks that shattered that complacency. The collapse of Bretton Woods and the end of dollar-gold convertibility, oil embargoes in 1973 and again in 1979, double-digit inflation, fiscal strains such as the near bankruptcy of New York City and the UK's IMF bailout, and a credibility crisis for US institutions amid the end of the Vietnam War and the Watergate scandal.

Markets didn't simply collapse down, instead both stocks and bonds moved in wide, volatile ranges. There were sharp rallies and equally sharp reversals. A push-and-pull between political pressure to stimulate growth and inflationary forces that demanded restraints.

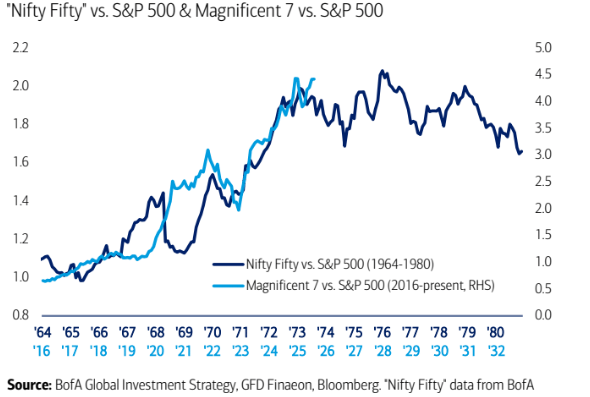

People who bet on steady buy-and-hold strategies in blue chips were often disappointed since the vaunted Nifty 50 and the early 70s eventually derated, but other asset classes thrived. Commodities boomed in the inflationary environment, real estate benefited, and smaller, cheaper companies outperformed big, overvalued growth.

The result back then was a boom in equities, the famous Nifty 50 stocks then, the mag7 today. Along with lower Treasury yields despite rising inflation pressures.

But the story didn't end there. After the initial boom, inflation came back with a vengeance, requiring harsh measures like price controls.

There's a similar script playing out now, with the potential of another wave of inflation in 2026 and with policymakers possibly resorting to outright intervention in prices to suppress it.

The right strategy is to own assets and sectors that can outpace China's industrial and technological push while avoiding those most exposed to the eventual inflation fight.

The bet is that the "visible fist" of central banks will keep risk assets supported, and that's why institutions are accumulating gold, crypto (mainly Bitcoin), and equities today.

So we were at the end of long bull markets in both bonds and equities with heavy fiscal spending, geopolitical pressures, and political incentives for central banks to err on the side of easy policy.

The risk is a replay of a "boom-and-bust" decade, defined not by one clean trend but by multiple inflection points with bursts of easing and tightening, inflation coming in waves, and policy improvisations such as price controls or yield suppression.

The winners might not be the same mega-cap darlings at the peak, but the assets that can survive and even thrive through volatility

Such as small-cap value, hard assets like gold, commodities, real estate, and Bitcoin.

Even if the Trump administration doesn’t formally announce price controls in 2025, the trend will be unmistakably greater government interference in markets for political gain.

With midterms, Trump knows that a second wave of inflation would be toxic at the ballot box, making pre-emptive interventions all but inevitable.

Expect subtle forms of price management rather than outright controls. In energy, Trump leans on deregulation and ‘drill, baby, drill’ policies, alongside Ukraine peace efforts

Energy stocks are still down 3% since the election. In healthcare, an executive order to peg US drug prices to ‘Most-Favored-Nation’ levels has dragged the sector 8% lower.

In housing, the declaration of a ‘National Housing Emergency’ aimed at boosting supply has knocked homebuilders down 2%.

Markets are essentially trading Trump politics: shorting the sectors that ‘whip inflation’ with utilities looking next in line, given Trump’s vow to cut electricity prices in half within 12 months amid AI-driven power demand and going long the sectors that ‘outpace China.’

That means national security plays, such as Big Tech, semiconductors, and aerospace & defense, are all positioned to benefit from a favorable US/China trade reset in 2026.

The trade works as long as Trump’s approval rating holds above 45%, but risks a sharp reversal if support slips below 40%."

Join Discord

Become a Premium member. Premium newsletters & Discord community access

Become a Premium member. Premium newsletters & Discord community access

50% discount forever on yearly subscription