Non-Farm Payroll Matrix - including rates, flows & macro

We all keep hearing it, and boiiii, it does get tiresome. Almost every FOMC and the latest Jackson Hole speech. So we, the central banks, and the rest of the world are now at the mercy of "data-dependent."

Is it a crime to ask: How reliable is the data?

The Atlanta Fed's Q3 GDP projection is currently holding up despite some surprises in the US. Additionally, the Dallas Fed's service survey, in contrast to its manufacturing survey (ISM), highlighted...

"Price and wage pressures have increased."

The economic indicators offer a mixed but cautiously optimistic view. On one hand, the Atlanta Federal Reserve's projection for Q3 GDP continues to hold steady, suggesting that the economy "might" be on a stable path despite some unforeseen variables.

On the other hand, the Dallas Federal Reserve's recent survey shows an increase in price and wage pressures, which diverges from the trends we've seen in its manufacturing survey. The rising costs in the service sector could be a warning sign for sticky inflation, even though GDP seems to be on a stable path.

READ TILL THE END FOR THE NON-FARM PAYROLL MATRIX

Now, it's all about "data-dependent," which refers to central banks' approach to adjusting their monetary policy based on the latest economic indicators and forecasts.

In other words, they'll tweak things such as interest rates based on what's happening with the economy and inflation, instead of just sticking to a set plan. While this makes them quick on their feet, it also makes the markets more volatile as investors don't know what to expect anymore.

The Federal Reserve raised its policy interest rate by 25 basis points to 5.25% - 5.50% in July 2023. They did this because core inflation remained elevated despite the lower headline inflation.

The Fed says they'll keep an eye on new data to determine their next moves. They're not expecting a recession in 2023, but they also admit plenty of wild cards could change things.

So, being data-dependent is a double-edged sword for the Fed.

It lets them adapt but also makes market volatility and market participants unsure.

Europe

In Europe, the European Central Bank (ECB) also hiked by 25bps in July, following a surge in core inflation exceeding 5% year-over-year. The ECN blamed the rise in inflation on temporary factors such as supply chain disruptions, higher energy prices, and base effects.

Thread

I'm expecting inflation to rebound due to the "base effect"

— Romano (@RNR_0) July 28, 2023

At the same time, I'm expecting "core inflation" to slow down

However core inflation will probably remain relatively high for the rest of the year.

Just a slow down, I don't expect the numbers to plummet.

But the European Central Bank (ECB) has also pointed out that wages are going up similarly, which could trigger a ripple effect on what people expect from inflation and how prices are set. The ECB says it will closely monitor how inflation changes, what's driving it, and how its policy moves affect things like loans and the overall economy.

China

In China, the People's Bank of China has cut rates by 25 basis points to stimulate more households and businesses borrowing since their economy is slowing down and dealing with deflation right now.

The People's Bank of China (PBOC) has also injected more liquidity into the banking system and eased some regulatory requirements for lending. The PBOC faced a challenging trade-off between supporting growth and containing financial risks, especially as China's debt level reached over 300% of GDP.

The People's Bank of China (PBOC) has reiterated its commitment to a prudent and flexible monetary policy that balances internal and external factors.

While we are talking about China, there's been a new Bloomberg shitpost which was interesting to read

Shuli Ren

Shuli Ren

Xi ideology (collapse to read)

China’s President Xi Jinping is not a big fan of social welfare. In past writings, he took pains to explain what “common prosperity,” one of his signature policies, was not: It was not egalitarianism or the rise of a welfare state. During the pandemic, when the US government wrote trillion-dollar checks to consumers, China went for trickle-down economics instead. The government’s stimulus came in the form of infrastructure spending and tax rebates to smaller businesses.

Xi has deep-rooted philosophical objections to Western-style consumption-driven growth, seeing it as wasteful and at odds with his goal of making China a world-leading industrial and technological powerhouse, reported The Wall Street Journal, citing people familiar with Beijing’s decision-making.

Everyone is a product of his time, and Xi is no exception. “Produce first, live later” was a popular slogan in the 1960s, his formative years. Back then, China was focused on the industrial sector, developing its nuclear technology for instance, while at the same time practically ignoring people’s livelihood, leaving them to struggle in slums and on food stamps. If you don’t produce something first, how can you consume later, the thinking went.

I see that deep-rooted worldview in my father, a chemical engineer by training. During a road trip to Maine in 2000, when we passed by abandoned paper and steel mills, he puzzled over how the local economy worked, and couldn’t understand that consumption begets consumption. Where was the original dollar, he kept on asking.

About that data-dependent

Predicting economic trends is no walk in the park, especially when key signs are giving mixed messages. But for analysts and central banks, spotting a game-changer is super important. To do that, they lean on a basic understanding shaped by data, which can shift as time goes on.

As Stefan Koopman asked yesterday, why do you have a job if you're not doing that?

Jackson Hole

As explained in previous newsletters, The Jackson Hole meeting is an annual symposium hosted by the Federal Reserve Bank of Kansas City, where central bankers, policymakers, academics, and economists from around the world discuss important economic issues.

The theme of the 2023 meeting was "Structural Shifts in the Global Economy" and let's just say, it showed that capitalism is going through a rough patch.

One hot topic was the idea of "global predictable unpredictability"

Basically, central bankers admitted they can't predict or control the long-term effects of huge global changes like digitalization, climate change, inequality, and geopolitical tensions. (Shocker, right?)

What's surprising is that a lot of people who usually hang on every word from central banks didn't catch that these guys are basically saying they're flying by the seat of their pants. The takeaway?

Higher for Longer

That means central bankers are ready to follow through with higher interest rates, even if it does hurt the economy, to bring inflation down to their target level of 2% and preserve their credibility.

Now there's another recent trend: "Bad news is good news.", People see bad economic data and are basically betting that the Fed will fumble, cut rates, start quantitative easing, and run the money printer at full capacity to save the economy from being hurt.

Are you a premium member of the newsletter but still didn't join Discord?

(Also article does not end here)

Join Discord to get the full value out of the newsletter. There's no extra cost associated with Discord. It's included. All service ;)

Yes, options data such as dark pools, unusual flow, etc., are also included.

closely monitor

It's cheaper than buying Friends Tech keys

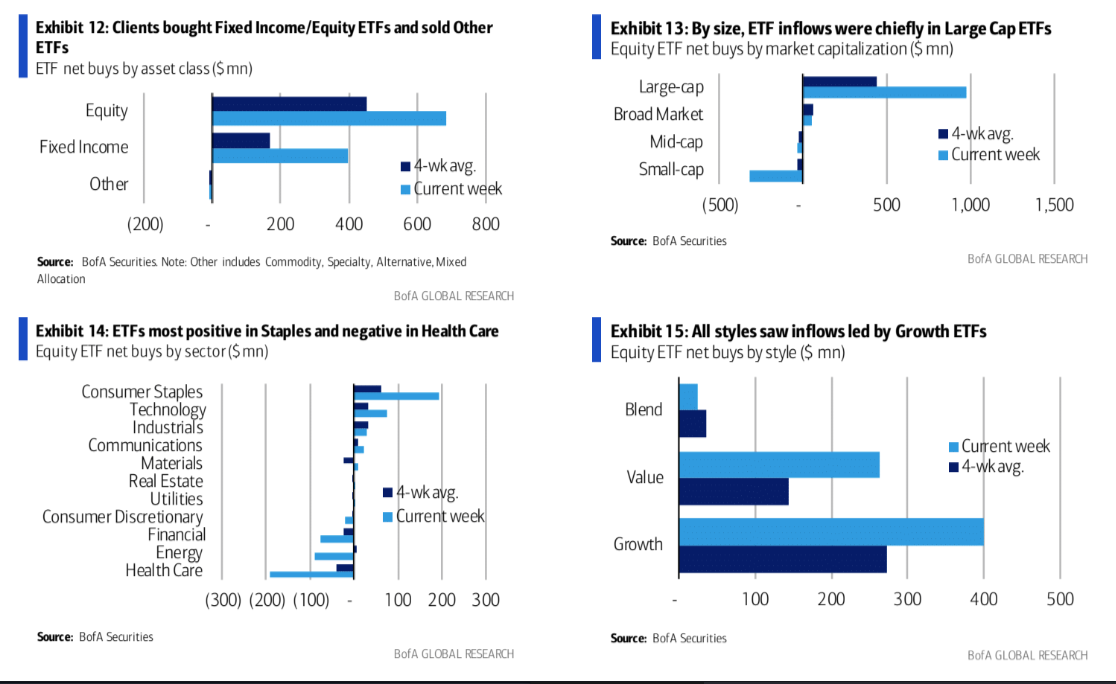

ETFs flows

shows

Rates

The US bond market is facing a lot of uncertainty as recent economic data shows weaker than expected, while the Fed is preparing to taper its asset purchases.

That has pushed down the yields on 10-year Treasure notes, which are a benchmark for global borrowing costs. Meanwhile, the eurozone market is more focused on inflation and the ECB's policy stance, which can diverge from the Fed's incoming months.

That supported the yields on 10-year German bunds (which are the main reference for European debt)

The difference in bond yields between the US and Europe is getting smaller, and that's largely because of what people think will happen with each economy and their financial rulebook, so to speak.

Now, you might ask, "How do we even track this?" Well, one way to keep tabs is by looking at real interest rates. These are the rates you get after accounting for inflation. It's like the real-world "profit" you expect for lending your money to the government. If these real rates go up, it's a sign that investors are betting on a stronger economy and stricter financial rules down the line. On the flip side, if these rates go down, people are less optimistic, expecting a weaker economy and more relaxed financial guidelines.

In the US, these real rates have been the big movers and shakers for bond yields. For example, when the US was bouncing back from COVID, these real rates shot up and dragged the regular, or "nominal," bond yields along with them. But when things got rocky again because of the Delta variant and other hiccups like supply chain issues, real rates dipped and took nominal yields down with them. As for inflation, people generally believe the Fed's got it under control for the long haul so that part's been pretty stable.

In Europe, bond yields are getting pushed around more by worries about inflation than the actual "real" rates—basically the opposite of what's happening in the US. This is because the European Central Bank (ECB) is playing it safe. They're like, "We're keeping our policy rate at zero or even lower until we hit that 2% inflation target."

So, what's the result? Market participants are kind of on edge about inflation in Europe, especially after energy prices took off like a rocket. That nervousness led to higher "expectations" of inflation, which in turn bumped up the normal, or "nominal," bond yields.

On the other hand, real rates in Europe are expected to chill out at low levels or even go negative. Why? Because investors don't see the ECB making big moves or the European economy growing anytime soon.

To understand the difference between the US and Europe, it's important to consider their real rates. Lately, the gap between the two has been getting smaller because the US rates are decreasing faster than Europe's. This could mean that investors are feeling less optimistic about the US economy, and more positive about Europe's. It also suggests that the Federal Reserve and the European Central Bank might have more similar policies than we thought.

There are many things that could affect the financial landscape in the future. These include new economic data, discussions by central banks, and political events. For example, if the US economy gets better and the Federal Reserve decides to speed up its plans, bond yields in the US might go up. This would make the gap between US and European bond yields wider. On the other hand, if inflation gets worse in Europe and the European Central Bank takes a more aggressive approach, bond yields in Europe might go up. This would make the gap between US and European bond yields narrower.

Payroll Matrix & Expectations

Yes, saving the best for last

The Non-Farm Payroll (NFP) headline for August is expected to show a cooling job market, with projections at 170,000, down from July's increase of 187,000. However, estimates vary widely, ranging from 40,000 to 230,000.

Private payrolls are forecasted to be 150,000, a decrease from the previous month's 172,000. Manufacturing employment is expected to remain flat, following a 2,000 job decline in July.

The unemployment rate is projected to hold steady at 3.5%, following an unexpected drop from 3.6% in July. Some analysts do anticipate a slight uptick back to 3.6%, which would still fall below the Federal Reserve's year-end median projection of 4.1%. Note that updated projections from the Fed are expected in September.

For wages, average monthly earnings are anticipated to ease to 0.3%, down from July's 0.4%, with forecasts varying between 0.2% and 0.4%. On an annual basis, earnings are projected to rise by 4.4%, unchanged from July, though analysts are divided with estimates ranging from 4.3% to 4.5%.

For tomorrow's employment data

- Headline Employment Increase: 168k (Goldman Sachs: 149k, Previous: 187k)

- Average Hourly Earnings (MoM): +0.3% (Goldman Sachs: +0.2%, Previous: +0.4%)

- Unemployment Rate: 3.5% (Goldman Sachs: 3.5%, Previous: 3.5%)

- Labor Force Participation Rate: 62.6% (Goldman Sachs: 62.6%, Previous: 62.6%)

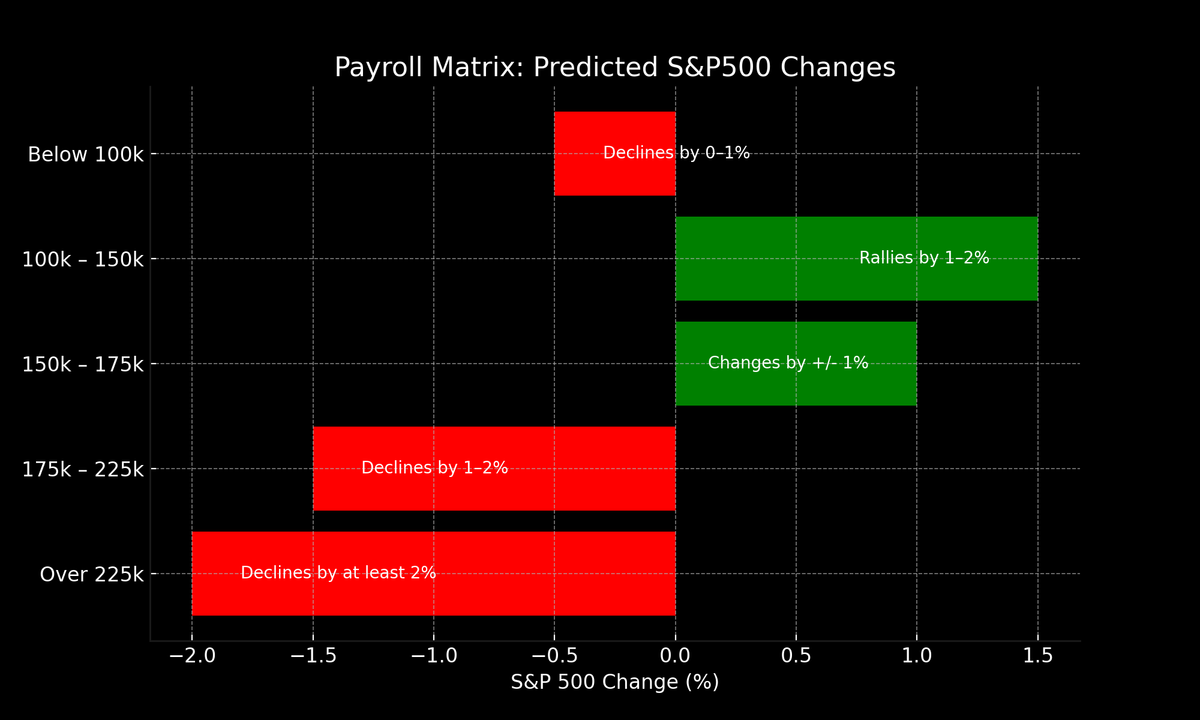

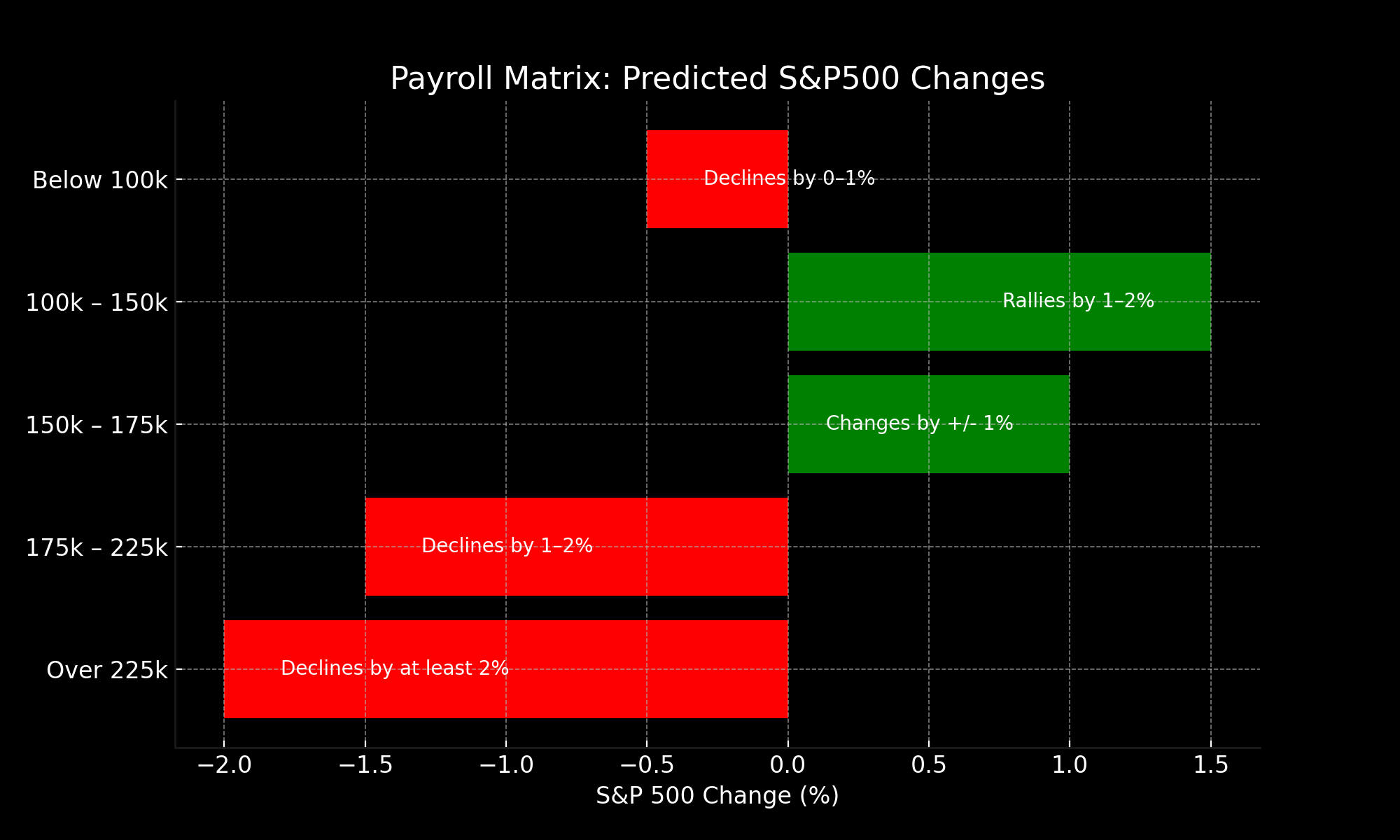

Here is the framework used to interpret tomorrow's headline employment figures in relation to potential S&P 500 movements

Goldman Payrolls Matrix:

- Over 225k: S&P 500 declines by at least 2%

- 175k – 225k: S&P 500 declines by 1–2%

- 150k – 175k: S&P 500 changes by +/- 1%

- 100k – 150k: S&P 500 rallies by 1–2%

- Below 100k: S&P 500 declines by 0–1%

So what would that mean?

- Over 225k: If more than 225,000 jobs are added, the model predicts that the S&P 500 will decline by at least 2%. This could be interpreted as a sign that the economy is overheating, possibly leading to inflation and subsequent monetary tightening.

- 175k – 225k: If between 175,000 and 225,000 jobs are added, the model predicts a 1-2% decline in the S&P 500. This is still considered strong job growth but less alarming than the >225k scenario.

- 150k – 175k: If between 150,000 and 175,000 jobs are added, the model predicts that the S&P 500 will change by +/- 1%. This suggests that the market views this level of job growth as neither too hot nor too cold.

- 100k – 150k: If between 100,000 and 150,000 jobs are added, the model predicts a 1-2% rally in the S&P 500. This could be interpreted as a sign that the economy is growing but not too fast, reducing the risk of inflation or monetary tightening.

- Below 100k: If fewer than 100,000 jobs are added, the model predicts a 0-1% decline in the S&P 500. This may indicate concerns about economic stagnation or recession.

Disclaimer: While these guidelines may be based on historical data, they are not guaranteed to predict future market behavior

Anyways, to visualize it for you

Before closing this article subscribe to the premium newsletter. The premium membership also includes full access to my Discord with more real-time updates and reports

ApeX DEX

Before continuing to read this, ByBit has made KYC mandatory as many other exchanges. Why not try out ApeX DEX? You can use your wallet or social account to use the DeX. No gas fees are required for trading & the fast trading experience is like a CEX.

Consider ApeX DEX

Instructions:

https://twitter.com/RNR_0/status/1652360705331347461

For a lifetime fee discount, check the link