Market insight - Quadruple witching - June 17, 2022

Today is the day

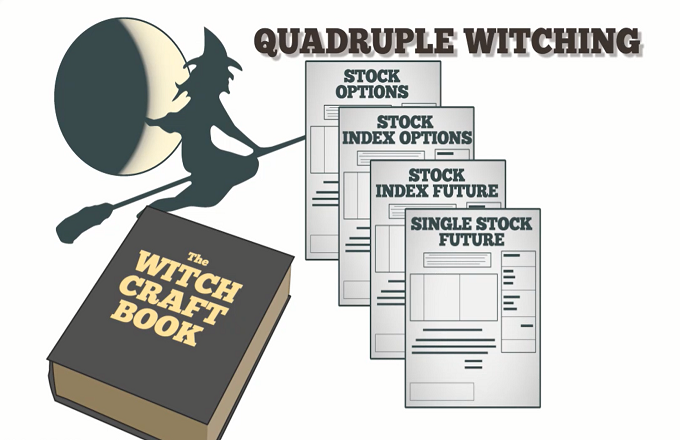

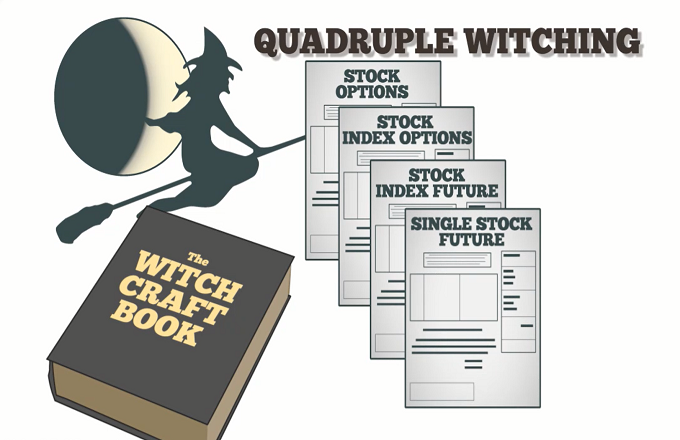

Quadruple witching/ Quad expiry

Quadruple witching/ Quad expiry is the day when four different options contracts simultaneously

There are four different types of options that can expire on quad expiry

stock options, index options, futures options, and commodity options.

All of these options contracts expire at the same time, and it's a big day for options traders.

In legend, "evil" may be underway during the witching hour. In derivatives trading, this word refers to contract expiry, frequently on a Friday at trade's end.

So on quadruple witching, listed index options, single-stock options, index futures, and stock futures expire concurrently.

During the quad expiry, traders are especially cautious because there is a lot of potential for volatility.

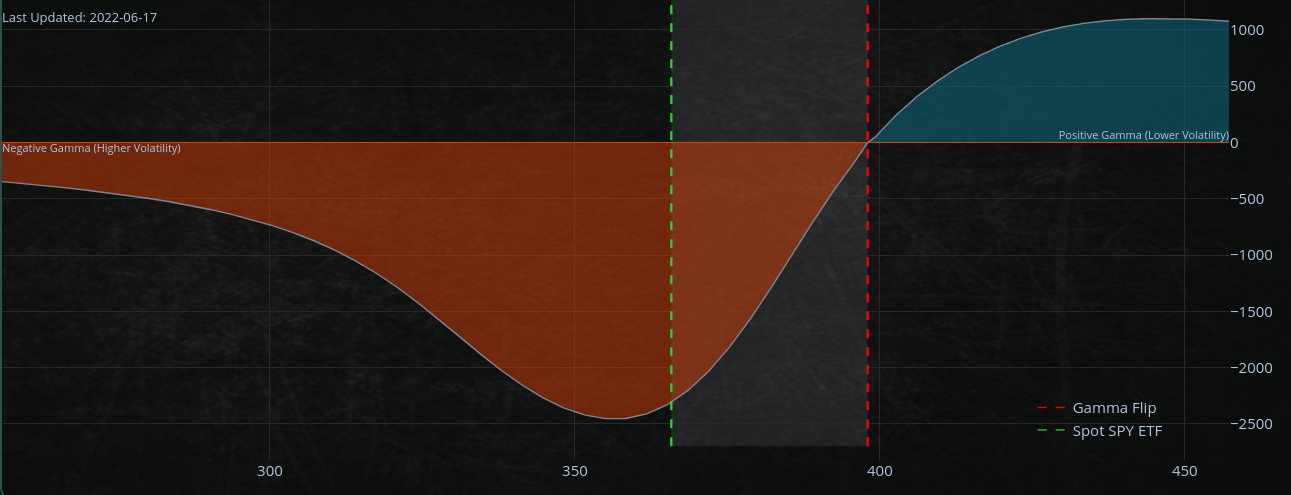

We are still in a negative gamma theratory.

On this day, options contracts that are "in the money" are usually "exercised," which means that the underlying security (like a stock) is bought or sold. Depending on whether more contracts are bought or sold, this can change the market.

Synthetic put positions

If there is more demand than supply for put options, which give the holder the right to sell the underlying at a certain price, dealers will make "synthetic put positions" to meet this demand. That means they will take a long position in the market and balance it out with a short position in the futures market.

What's a "synthetic put position"?

A synthetic put position is created when a trader buys a call option and sells an equivalent amount of the underlying. That makes a position that is effectively the same as a put option.

Dealers are using "synthetic put positions" to meet the demand for put options when there is excess demand. By creating these positions, dealers can accommodate the demand without taking on a directional bet.

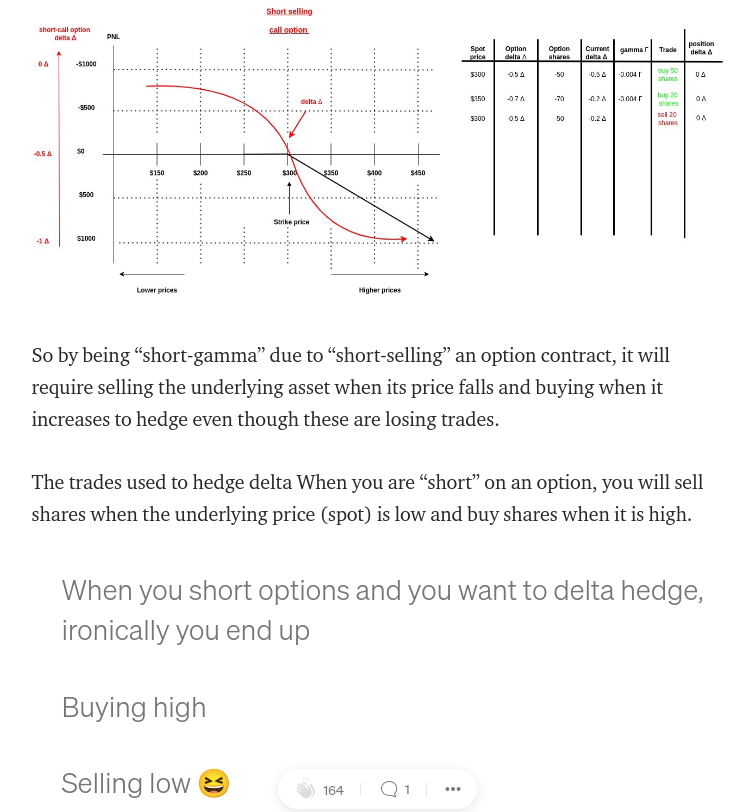

Suppose the put options move deep "into the money." In that case, the end customer/trader typically longs the market via the underlying security and shorts the market by the delta of their hedge. The delta is the amount by which the price of an option changes in response to a change in the underlying.

Example to explain it. If the delta of a put option is 0.50 and the price of the underlying market goes up by $1, the put option will go down by $0.50.

With the "synthetic put position", the dealer is effectively long on the market, so the dealer must short futures to balance out this direction trade. That means they are well protected and won't make or lose money no matter what happens to the market.

At expiry, the person who owned the put option could sell the underlying or just sell the "in-the-money" put option back to the dealer. In that scenario, the dealer will buy back futures and return to delta-neutral.

If everything else stays the same, this will put the market up because the end customer is the net buyer but because of positions that don't end today, dealers are still net short gamma. That means they must follow the market and buy more futures if the market starts to go up.

The market could go down if traders hedge more than dealers thought they would. Here is where it gets tricky because the dealers have to guess whether the traders will be happy to keep their positions or buy more put options right away to protect their positions.

The market is likely to go up because traders usually have a long position in the market through the underlying market and a short position through the put option. But there is a big left tail, which means the market is more likely than usual to go down.

A fat left tail

In this context, a fat left tail means a higher-than-usual chance that the market will go down. That is because the customer/trader usually has a long position in the market through the underlying market and a short position in the market through the put option.

So, if the market starts going down, the traders will likely buy more put options to protect their position. This can cause the market to move lower than expected, which is why the market is more likely to move lower than usual.

Gamma

We are close to the gamma trough, where gamma values are very negative.

When market participants keep buying "put options" (positive gamma, negative delta), the dealer, on the other will be stuck with the opposite trade, which is "short-put" and therefore has a positive delta and negative gamma.

Suppose prices fall more than expected. That forces dealers to hedge their bets and sell the underlying or and futures to get back to delta-neutral, making the market fall even further. We saw large investors selling their positions while individual investors were not active.

As mentioned in my options article about gamma & delta hedging

https://romanornr.medium.com/options-trading-part-3-gamma-curvature-risk-9f6dd4b3db5b

Screenshot of the article

Continuing, now I get the question a lot:

What is Negative Gamma?

Negative gamma is a measure of convexity. It is the second derivative of the price of an option with respect to the underlying asset/market price. In other words, it measures how the price of the option contract changes as the underlying market price changes.

An option contract with negative gamma ("short-puts, short-calls" and whatever strategy gives a negative gamma exposure.... like FTX MOVE contracts short. Which is basically a short-straddle

Now continuing on

Dealers will have to hedge and chase the delta by selling low as the market falls and buying high as the market moves up. Gamma works in both ways.

Dealers are positioned to profit regardless of the market's direction. Dealers/market makers/liquidity providers must hedge their current holdings as orders pour in rapidly and evaluate new order requests soon afterward. Due to large quantities of computer capacity, low latency network connections, and excellent execution, it resembles art more than a science at this point.

Nevertheless, a normal gamma chart does not provide the whole story since gamma is heavily influenced by time to expiry. Since the option's delta will be vastly different depending on whether it expires in-the-money or out-of-the-money, the option's delta is hard to calculate

SPX500 "put heavy" option market

The S&P 500 is experiencing a lot of movement. Key resistance is at $3700

Numerous customers have negative delta exposure through put options contracts with the June OPEX expiration date. These contracts are profitable if the underlying markets go down or if volatility rises.

On the other side of the transaction are liquidity providers who sold these put options to hedge their own exposure by selling put options.

Those "short-put" options carry a positive delta and constantly need to sell in the underlying market or futures to delta-hedge. When the contracts expire, the dealer doesn't have to hedge that way. In a negative gamma territory, the moves are extreme since dealers need to sell more when the market goes down and buy more when the market goes up since they have negative gamma exposure due to the put options.

We may have a relief rally Monday or Tuesday now those options expire

Is the crowd over hedged? Lot of VIX buying. However, hedge or buy insurance when you can. Not when the building is already on fire.

This could create "temporarily" a synthetic floor in the market.

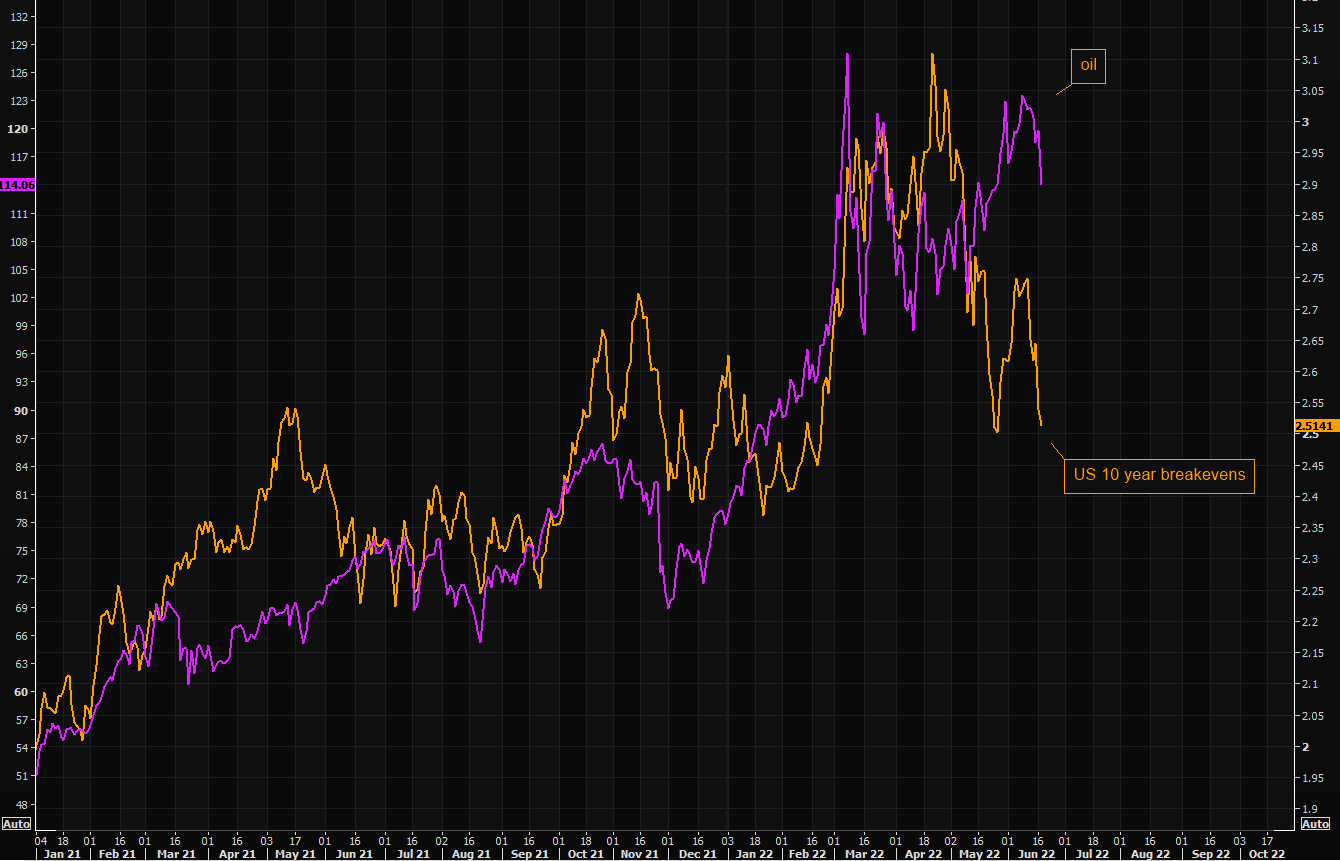

Oil vs inflation

Oil has been on the mind of the federal reserve

if oil prices are connected to inflation, and if they keep going down, it could affect the macroeconomic picture as a whole.

Since oil is a key part of making a lot of goods and services, a drop in its price can cause inflation to go down. Thuat could then have an effect on the economy as a whole.

I'm not sure, asking you the readers, does lower inflation usually means slower economic growth?

JP Morgan on rate hikes

The Federal Reserve may raise interest rates by 50 basis points at its meeting this week, which would be negative for the markets.

However, bonds are currently priced in

- 75 basis points for June

- 75 basis points for July

- 50 basis points for September

- 50 basis points for November

- 25 basis points for December

- 5 basis points for February 2023.

This suggests that the market is expecting a more hawkish stance from the Fed than what is currently being priced in.

If the Fed raises rates by 100 basis points, this will likely be negative for the equity market in the short-term.

However, the view may fade later in the week as bonds continue to sell-off.

The SPX500 is encountering heavy resistance at $3850 and I don't expect it to close above this level on June 17th.

The $3600 JPM June 30 "short put" strike downside support into June 30th

We can see the $4285 JPM June 30 "long put" strike as resistance and a "best case" scenario for a relief rally.

However, I don't have a bullish view on July, that's when we could expect prices to fall.

Remember, "don't fight the federal reserve" is a phrase used by investors to justify buying and longing at every dip. However, the federal reserve wants a "market reset."

They also said: "Not really sure how it will affect housing prices."

With the 30Y mortgage rate rising to the 2008 level, we might know where this is going

*POWELL: FOMC IS WATCHING MORTGAGE RATES, HOUSING MARKET

— zerohedge (@zerohedge) June 15, 2022

... "not really sure how it will affect housing prices"

Here's a tip pic.twitter.com/fUbT536Ww2

Do you want to see some real estate cringe? Don't worry. I got your back :)

Finally, ultimate real estate cringe.

The Big Short 2 trailer just dropped

— Wall Street Silver (@WallStreetSilv) June 16, 2022

Sound ON pic.twitter.com/fBKL4Ar6OH