Market insight, July 18, 2022

With another hotter-than-expected CPI inflation reading last week, On July 15th, it seemed that a market sell-off similar to June's was possible. However, Fed Governor Waller's suggestion that 75 basis points were more plausible than 100 basis points acted as a catalyst for dealers to bring the market to a nearly unchanged state. The 10-year US bond yield hardly increased, defying many expectations.

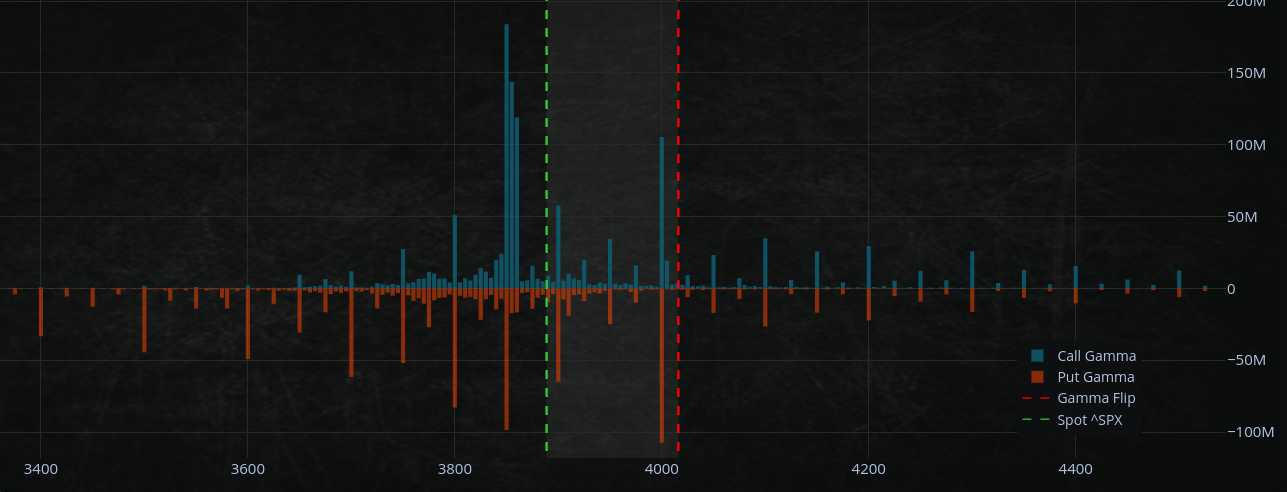

HoweverInterestingly, of intraday volatility, the market didn't fall as much as feared. Interestingly, the "zero gamma level" last week and the delta of puts expiring "out of the money" was sizeable for July 15th Option Expiration.

After expiration, there was a lot of hedging going on. New put options were being bought at a lower strike. However, since these new put options have a lower delta than the ones expiring, this resulted in net buying from the dealers.

(I didn't write on Friday due to an eye laser surgery on Thursday, so this is a small recap).

Markets are rising as investors continue to respond positively to Friday's rally, spurred by the options expiration. Also, Fed Governor Waller suggested that 75 basis points were more plausible than 100.

Ironically, it was a case of "sell the rumor, buy the news."

Basically

The recent movement of short-dated, near-the-money call options into the money has created a significant source of "negative gamma" for dealers. Speculators betting on a rebound have been proven right, and dealers are now scrambling to chase delta higher.

Right now, we're witnessing a miniature version of a gamma squeeze.

In case you forgot, the term "gamma" refers to the rate of change of an option's delta in relation to the underlying asset.

A "gamma squeeze" occurs when the gamma of a particular option (or options) becomes very large, causing the option's delta to change rapidly. That can happen when the underlying asset price moves sharply in one direction or another, causing the option to move deeper into or out of the money. There was a net result in call buying. The dealers and liquidity providers are on the other side selling those call options. When the market moves higher, the delta of those call options starts to increase. Since the dealers are short calls, their negative delta increases at a fast phase. To delta hedge, the dealers will have to buy the underlying, which causes the market price to go up more, and their call option's negative delta increases, even more, forcing them to buy even more stock. This feedback loop continues.

I assume most readers here are familiar with the GameStop and AMC gamma squeeze.

This squeeze is taking place even though overall gamma levels are still negative. This indicates that even though more options are bought than sold, the miniature version of the gamma squeeze is still causing dealers to lose money.

Current fundamental data may be weak, but it should not prevent these rallies. Positioning is low, widespread pessimistic bearish sentiment, and the Fed raises interest rates without addressing longer-term concerns. Consequently, market prices are likely to rise, producing as much capital destruction as possible for late bears.

Remember, you should be scared if everyone else is bullish but also don't be too bearish if a majority agrees that financial collapse is imminent. The strongest rallies happen in a bear market.

There has been an increase in the purchase of short-dated call options in the past week, and many of these options are now in the money.

This could create a situation where there is a limited supply of stock available (because many investors are holding onto their stock to avoid selling it at a loss), and high demand for stock (because investors with short positions are trying to buy stock to avoid being forced to buy it at a higher price to cover their short position). This imbalance could create a bear market rally.

The call options bought last week are already "in the money," and the marker makers/dealers/liquidity providers were on the other side selling these calls. They now need to delta hedge by chasing the market higher and buying the underlying.

Capital destruction for institutional traders may be greater if the market moves higher. That is because they have been in a negative gamma position for the past 6 months, meaning their positions have been losing value as the market has risen. If the market continues to rise, they will continue to lose money.

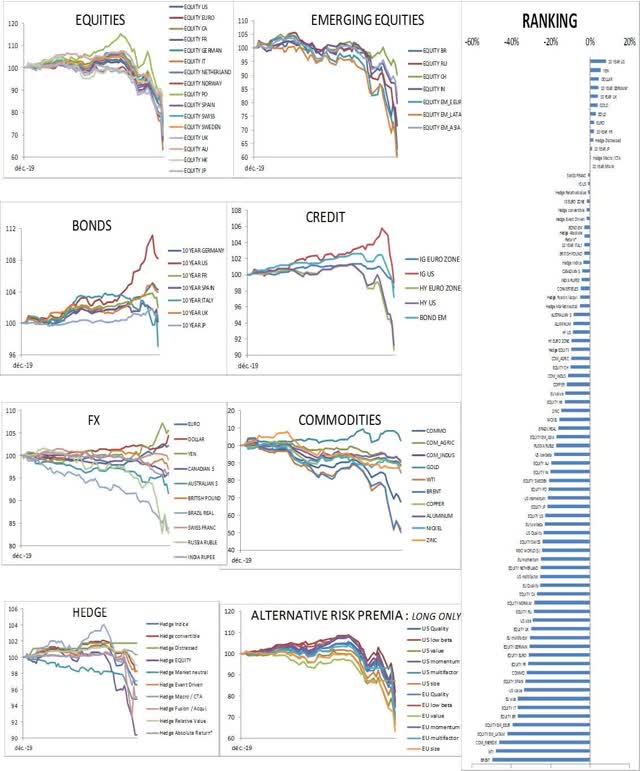

A great read

Gontran de Quillacq

Gontran de Quillacq

As long as the SPX500 stays above 3850, we can remain slightly bullish, and $4000 is resistance.

SPX500 above $3900 is a decrease in volatility.

However, SPX500 $3800 is our support, but negative gamma works both ways. We can go up easily due to negative gamma and down easily due to negative gamma as dealers chase delta.

Remember, in a negative gamma regime, dealers delta hedge their options by selling the underlying, chasing the market lower, buying high, and chasing the market higher.

I also think another AMC gamma squeeze is possible.