Market insight, June 24, 2022

Yesterday, the equity options markets were in negative gamma territory again, the options market is signaling that downside risk is greater than upside risk.

Nonetheless, the range of strikes that are impacting the market is forming a corridor around the present level, which is analogous to a "positive gamma dynamic".

Okay, uhm this is a bit difficult to explain but I will try to break it down.

A positive gamma dynamic would be one where there is more upside potential than downside potential. In this case, the market was indicating that there is more downside potential than upside potential. However, the range of strikes (prices) influencing the market is creating a corridor around yesterday's levels, which is similar to a positive gamma dynamic in that it protects a sharp move in either direction.

So dealers/liquidity providers probably had greater exposure to the market and stand to gain more if it moves in their favor. A positive gamma dynamic, therefore, creates an environment where it is more likely for the market to make to the upside.

Rebalancing Season

Today marked the "official" beginning of rebalancing season when many investors, funds, and traders change their portfolios to reflect their desired allocations for the next year. That often leads to substantial financial inflows into certain assets.

For instance, if an investor desires a 50/50 split between stocks and bonds, and the stock market went down while bonds went up, they may sell a portion of their bonds holdings and invest the profits in equities. That results in a cash injection into the equity market.

We can expect a market inflow of around $60 - $90 billion during the next week. That might have a big effect on pricing, particularly if a substantial amount of the money flows into a small number of assets.

So

Rebalancing season

refers to the period when systematic rebalancing strategies must buy or sell assets to match target allocations. That typically occurs at the end of a quarter or year.

Why is this week especially important?

This week is especially important because a large amount of money is expected to flow into equities and out of bonds. This is because equities have underperformed bonds significantly in recent months.

What is the potential impact of this rebalancing?

The potential impact of this rebalancing is two-fold. First, it could cause significant volatility in the markets as systematic strategies buy and sell assets to match their target allocations. Second, the inflows into equities could provide a boost to the stock market at a time when it is struggling.

Systematic rebalancing strategies

will require buying or selling to match target allocations by the end of the period. That is due to large market deviations, like the Federal Reserve allowing run-off to dominate balance sheet management.

With equities sharply underperforming bonds this month, there is potential for large inflows into bonds. Depending on the source and the estimate, roughly $100B of US equities must be net purchased over the next five days.

International equities also fare well, with roughly $59B of expected inflows. Bonds should see roughly equivalent selling. This week's data releases, including Michigan Sentiment and New Home Sales, could provide more information on the economic slowdown (MTD and QTD)

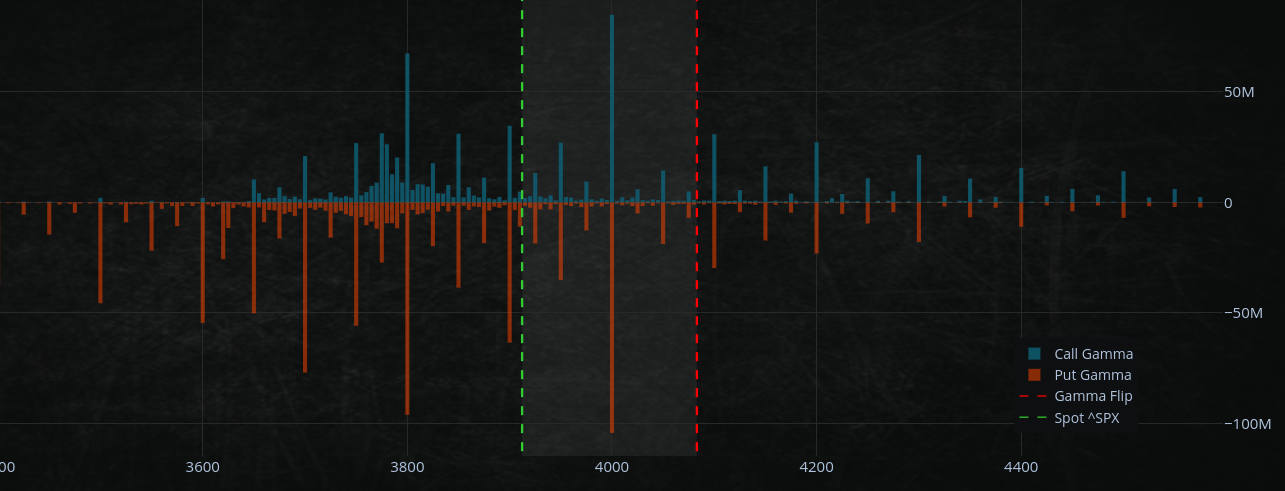

SPX500 current call open interest change

In recent days, more people have been buying calls than puts, so the $3800 strike price is becoming increasingly important. Even though prices have increased nearly 3% from their lows, this has kept volatility high. The 4000 strike is still possible and with the high expected inflows.

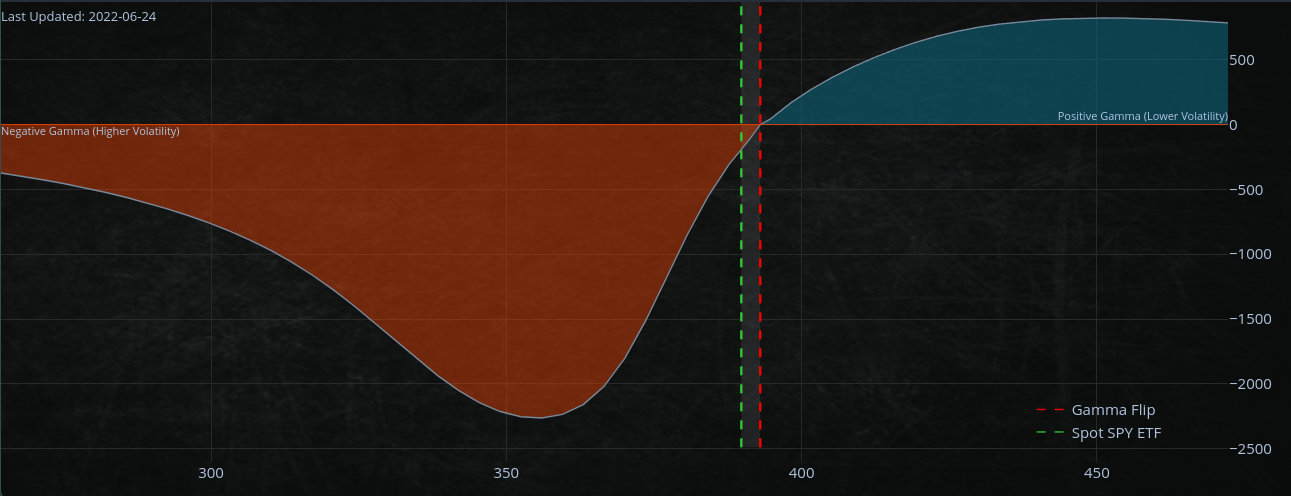

At the 3800 level, the SPX (S&P 500) is getting more volume and open interest (OI), while the SPY (SPDR S&P 500 ETF) is getting bigger at the 380 level. If you look at the data table below, you'll see that the highest gamma level for the SPX is 4000, while the highest gamma level for the SPY is 380.

That seems to be setting up a pretty clear range of $3800–$4000 for the June quarterly options expiration next Thursday (OPEX) for the SPX500.

Okay, so it seems most people don't know what I mean when I tweet about "OPEX," but let me clarify this.

OPEX or OpEx is the Options Expiration Date, the day on which the options contract expires

The SPX has more "gamma" at the $4000 level than the SPY. That means there is more pressure to buy the SPX at the $3800 level, while there is more pressure to buy the SPY at the 380 level. If the SPX breaks above $4000, it could go up more than the SPY.

The SPY's gamma level, on the other hand, is lower at $380. That means if the SPY breaks above 380, it has a greater chance of going up. Since the June quarterly OPEX is coming up next week, it may be important to keep an eye on both.

If the SPX breaks above $4000, it could go up more than the SPY. Why?

The SPX has more potential to move higher if it breaks above 4000 because it has more "gamma" at that level. Gamma is a measure of the rate of change in an option's delta in relation to changes in the underlying asset's price. In other words, it measures how much the option's delta will change if the underlying asset's price moves by a certain amount. Therefore, if the SPX has more gamma at the 4000 level than the SPY, it is more sensitive to changes in the underlying asset's price. That, in turn, means that it has more potential to move higher if the underlying asset's price (in this case, the S&P 500) breaks above 4000.

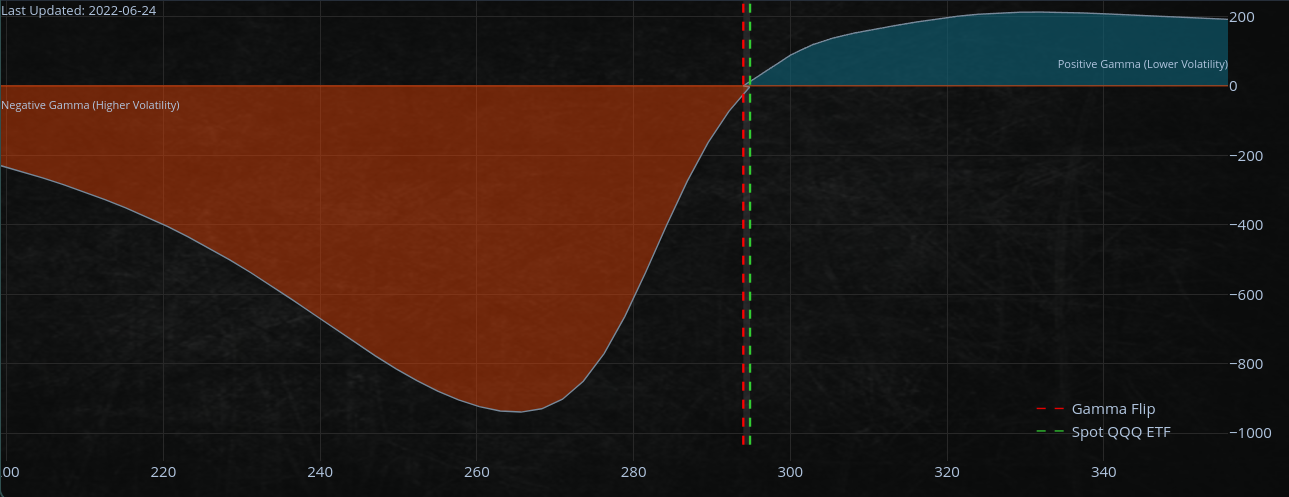

Also note QQQ short gamma

Short gamma dealers are those who sell options contracts, they have a "short-gamma" exposure.

However, in a low liquidity market, this "behavior" is magnified because there are fewer buyers and sellers, and thus the price of the option can fluctuate more wildly. That can cause problems for short gamma dealers, because they may end up having to chase delta. Short-sell when the market goes down, but buy higher if the market moves up. Creates more volatility as they need to remain delta neutral.

Poor liquidity is an ongoing issue in the markets, and it can make it difficult for investors to buy and sell assets when they want to. This can cause problems for short gamma dealers, because they may not be able to find a buyer when they want to sell an option, or they may have to sell an option at a lower price than they would like.

The implications of this are that short gamma dealers may have to adjust their strategies in a low liquidity market, in order to avoid losing money. They may need to be more selective about the options they sell, and they may need to hold on to their options for longer periods of time in order to avoid having to sell them at a loss.

What does this mean for the market?

That could mean that the market is not as efficient as it could be, because short gamma dealers are not able to operate as freely as they would like. This could also lead to more volatility in the markets, as short gamma dealers are forced to adjust their strategies.

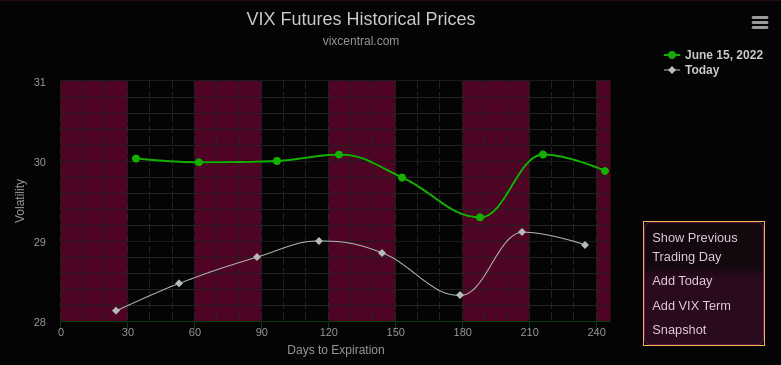

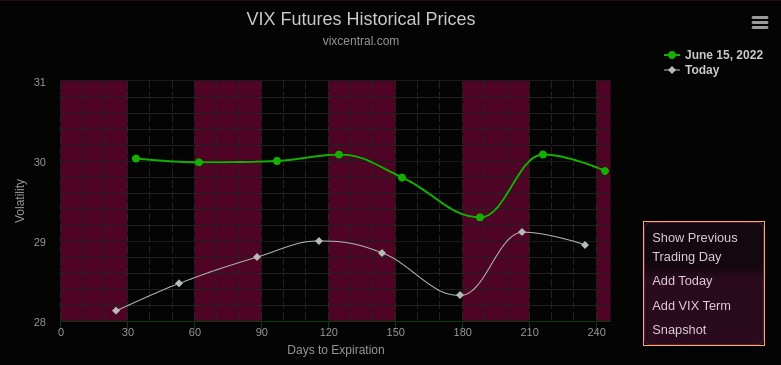

VIX

SPX500 volatility (as measured by the VIX index) has been declining recently, and if this trend continues, it could lead to higher stock prices before the end of June. That is because the VIX term structure is currently in contango, which means that longer-term VIX futures contracts are trading at higher prices than shorter-term contracts.

You can read more about contango in my latest medium post.

When equity volatility decreases, it typically leads to a flattening of the VIX term structure (i.e., the difference between longer-term and shorter-term VIX futures prices decreases). This flattening of the term structure is often associated with rising stock prices.

Continue on

Rallies into June OPEX should be labeled as "short covering" psyops and are prone to failures.

$4000 is a potential target for June 30 OPEX.

$3600 JP Morgan June 30 "short put" strike at $3620 is our support