Duration Cracks, who cares what about my equities and crypto?

While the US equity markets had been trading "as if" the US is no longer a top-tier credit for some time, Moody's formal downgrade last Friday reinforces that perception and introduces constraints for investors bound by ratings-based mandates.

The US downgrade comes just as Congress is getting closer to approving Trump's tax cuts. These tax cuts could increase deficits and debt. The IMF has urged Washington to control its spending, saying that the current financial path is unstable.

https://www.washingtonpost.com/business/2024/06/27/imf-warning-united-states-debt/

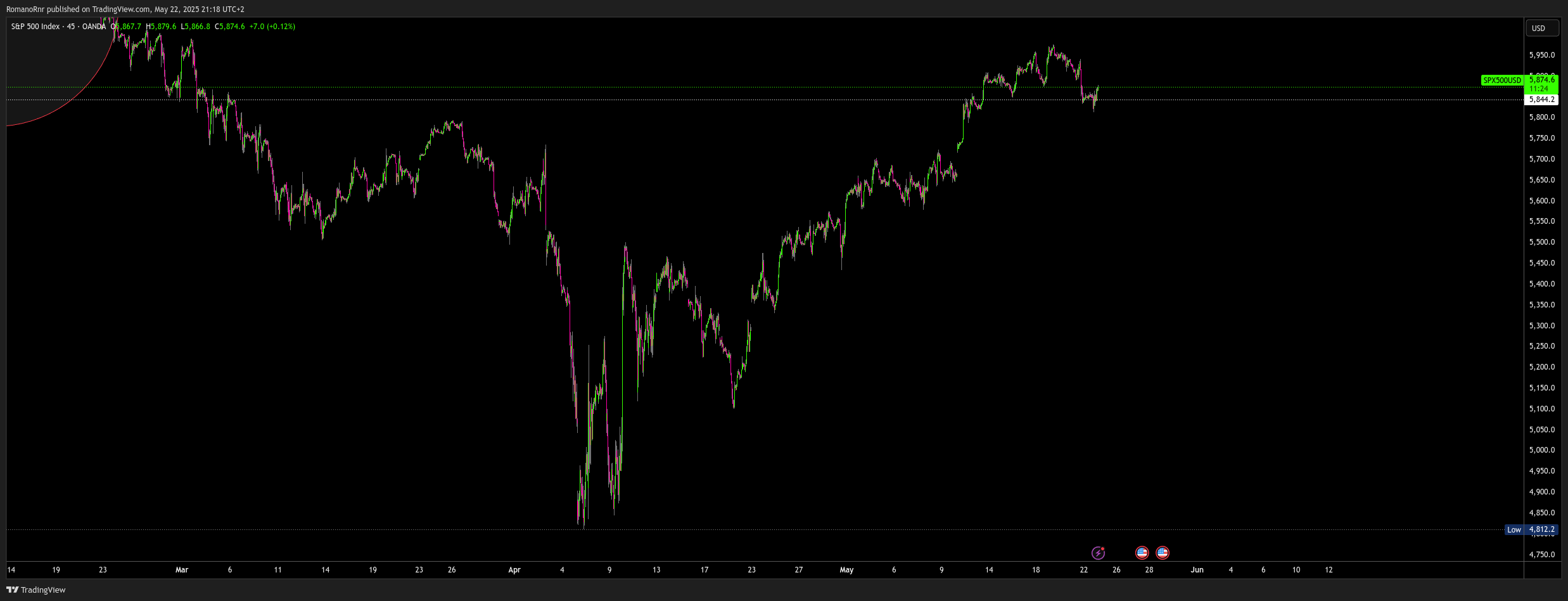

So, just as U.S. equities looked poised to break out last Friday, flirting with a squeeze dealer short gamma levels above 6000 in the SPX, the macro backdrop turned a bit hostile again.

A synchronized bleed in both the dollar and the long end of the Treasury curve is reasserting itself, exposing fragility that has been building under the surface.

One can only wonder,

is this the slow unwind of more than a decade of U.S. exceptionalism?

Years of QE-driven inflows and global over-allocation to U.S. assets are starting to reverse. As the dollar softens and Treasury yields without buyers stepping in, it's clear that the post-crisis playbook (low rates, strong dollar, and infinite foreign demand for U.S. duration) is now out of sync with reality.

We're seeing the early stages of structural repositioning, where foreign holders quietly derisking from Treasuries, exposing the long end of the curve. It's no coincidence that this comes just as the equity market was starting to press op option dealers' short-call positions, setting up for a potential meltdown. Macro dysfunction across rates, FX, and policy has returned.

The current weakness in the dollar isn't just about narrowing rate differentials or a fading U.S. growth premium relative to the rest of the world. A deeper shift is underway that ties directly into the political risk premium.

We're seeing what looks like an early-stage pivot on Trump's trade policy narrative. Tariffs are out, and FX management is back in play.

This plan B scenario is gaining traction among Asian press clippings and diplomats. South Korea confirmed that FX negotiations with the U.S. are ongoing. It's the latest in a string of signals that a future Trump administration, or even the current one, under pressure, may pursue bilateral currency arrangements rather than blanket tariffs.

Markets are starting to price this in. Demand for downside dollar protection, especially via puts on EUR, JPY, CHF, and GBP is ramping aggressively. Vol markers are showing a heavy skew toward USD weakness as investors hedge against the risk of a more interventionist FX regime.

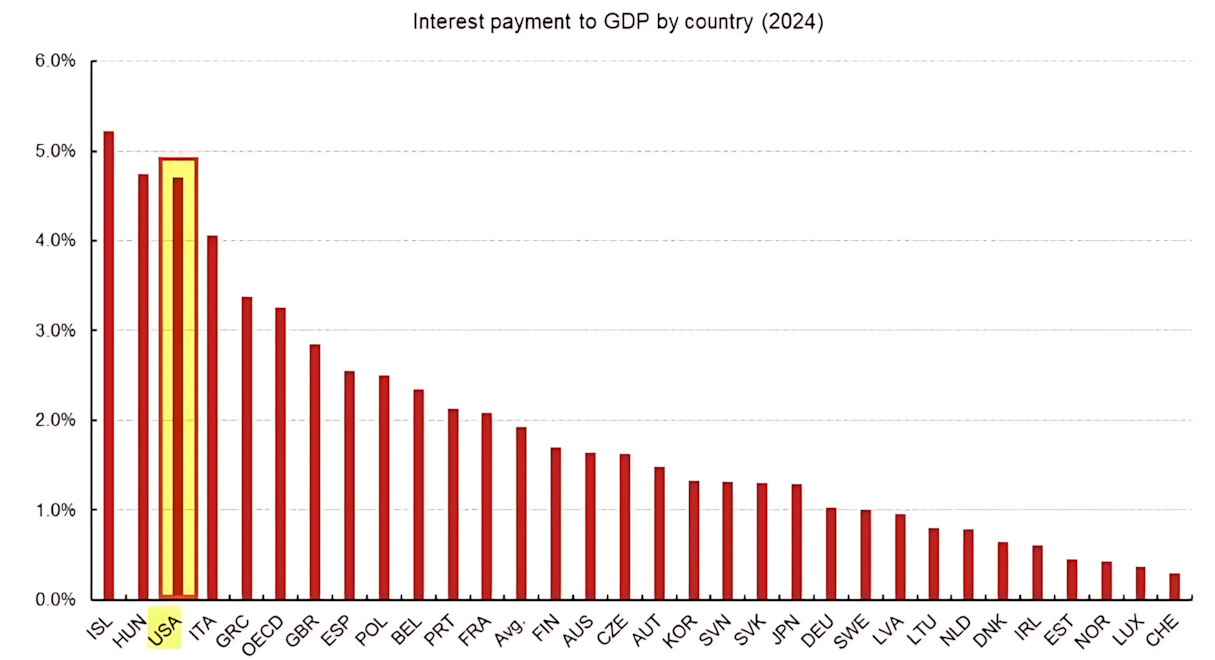

Yield curve is too flat

The U.S. yield curve is steepening, but it's not happening in a healthy, growth-driven way. Instead, it's a slow grind higher in long-end yields as markets start pricing in a harsher fiscal reality. The curve remains far too flat relative to the sheer scale of the U.S. deficit spending, and that mismatch is forcing a rebuilding of the term premium, especially in the 20- to 30-year part of the curve.

It's not about rate cuts or inflation anymore. It's about supply, fiscal sustainability, and the risk that global buyers are becoming less willing to absorb duration without a much fatter yield.

In the bond market, a 5% yield usually attracts buyers from Asia and other international investors. However, that interest seems to have disappeared. Recently, prices fell without much support, and exchange-traded funds (ETFs) showed this trend. TLT experienced outflows of $1.1 million, indicating that both retail and institutional investors are pulling back from long-term bonds.

In swaps, pressure is building. The focus has shifted to narrower spreads, with a drop to -60bps in 10-year swaps spreads now becoming more likely. The market is looking for a new price point reflecting larger deficits, less foreign investment, and increased supply.

The backdrop drives persistent demand for long-end volatility, especially in 30-year payer swapoptions and curve caps, as investors hedge against more abrupt moves in yields. The option market is showing a rising skew towards higher rates; the tail risk now lies firmly to the upside in the long-end yield.

With the U.S. fiscal outlook deteriorating and traditional buyers getting more selective, the long end of the curve is vulnerable. The term premium will come back whether markets like it or not.

Deficits

The U.S. fiscal path is bending off trend and not in a good way. Deficit spending has accelerated sharply, embedding long-term risk around inflation, debt sustainability, and upward pressure on real yields. We're now in a regime where fiscal profligacy is no longer abstract; it's a part of the price equation, pushing the term premium higher across the curve.

Yet, the economy keeps holding on.

Nominal GDP remains firm, thanks to the rare post-COVID combination of above-trend real growth and persistent inflation. The mix is keeping the Fed in limbo. Rates are restrictive, but the macro data refuses to roll over fast enough to justify cuts. The long-awaited recession still hasn't shown up, and that's forcing monetary policy to stay and hold.

A big part of that resilience is the labor market, where the scars from the pandemic still linger. After years of struggling to rehire and restaff, corporations are reluctant to cut headcount. That inertia has helped keep employment and wages relatively firm, even as profit margins start to feel the squeeze. Consumers, in turn, are still spending, sustaining what some are calling the "U.S. Consumer Miracle."

But this miracle is starting to look more like a balancing act. Corporate America is caught between sticky labor costs and waning pricing lower. If margin compression deepens, especially in a sector with little room to cut prices or raise productivity, the next phase could be layoffs.

That's the real recession trigger: not slower consumption per se, but a demand shock that follows a deterioration in earnings.

Until then, the Federal Reserve is stuck. There is too much nominal momentum to justify deep cuts, too much fiscal risk to ease financial conditions prematurely. The U.S. economy is holding, but its foundation (debt, deficits, margin) is quietly eroding.

Small note, it costs to borrow money!

“Will They, Won’t They”

On the fiscal front, the "will they, won't they" saga surrounding the House GOP budget is lurching forward. House Speaker Mike Johnson just confirmed a deal on a $40k cap for the SALT (state and local tax) deduction, one of the major sticking points in negotiations.

The streets take so far? The structure looks front-loaded and stimulative, especially with tax-cut components pulling demand forward. That bid under consumer discretionary names helped reinforce the soft-landing narrative for now.

But let's not get ahead of ourselves. The political game and maths are tight. With razor-thin margins, there's still a risk that the final bill comes out smaller or more watered down than expected.

This is especially true if leadership is forced to trim back provisions to secure the necessary votes. In that case, some of the expected "stimmy" juice could become more tricky than a flood.

Whether this fiscal impulse shows up at the scale investors are pricing is still a coin toss. Keeping an eye on headlines, the budget isn't done until it's done.

Supply pressures mount beyond the U.S.

It's not just the U.S. long end that's under pressure, this is also global. Across major economies, the long-duration trade is breaking down under the weight of structural supply and shifting policity regimes.

In Europe, the post-austerity era is officially here. Fiscal rules are being relaxed or outright scrapped, and a heavy wave of new sovereign issuance is coming. The region is now trying to reverse decades of underinvestment in defense, energy, and industrial capacity. That means more debt, more duration, and likely more upward pressure on yields, especially as the ECB is already stepping back from active bond buying.

Japan, though, is the real stress point right now. After a multi-decade period of yield compression through QE, ZIZRP, and outright BoJ ownership, the JGB market is being dragged into normalization. The ugly 20-year action earlier this week was a red flag. Lifers and domestic investors appear maxed out on duration. The BoJ's reduced purchases since July 2024 have only amplified the problem. What's left is a market with deeply impaired liquidity, structurally overweight holders, and rising rates as Japan finally exits its long deflationary funk. Inflation is sticky, wage growth is real, and the old QE-era playbook is no longer viable.

Globally, the market has been hyper-focused on recession and downside growth shocks, but the inflation story won't just die. UK CPI came in hotter than expected, Canada's print was firm, and even U.S. consumer-facing corporates like Home Depot, Lowe's, and Amer Sports are still bullish on demand trends. That's not the setup for a rally in long-duration bonds.

The common thread? The global long end is struggling to clear at current levels. There's too much supply, too little policy support, and too much residual inflation risk for duration to get traction. Demand will remain hesitant until we see a reset in yields, i.e., a proper term premium rebuild. And that’s exactly what markets are now attempting to price in.

No bid for duration but a big bid for equities from real money

With everything outlined, fiscal expansion, global supply shocks, sticky inflation, and central banks stepping away, There's just not going to be a sustained demand for long-duration assets until we find a true clearing price. That means more term premium needs to come back into the system to compensate for structural risks, such as higher debt loads, policy uncertainties, and rising geopolitical tail risk.

Despite all the macro dysfunction, one "very real money" investor has steadily accumulated long-dated, at-the-money LEAPS (call options) in spectacular size.

We're talking about multi-month, multi-billion-dollar premium deployment over $3B notional premium, translating into $8.3B in delta exposure and nearly $47m in vega.

This isn't fast money chasing gamma squeezes; this is deliberate, strategic positioning from a large institutional allocator betting on long-term upside in U.S. equities. They're showing conviction, not just on price but also on time and volatility. They're doing it against a macro backdrop that most would describe as anything but friendly.

Even in a world of rising yields, macro volatility, and fiscal noise, there's still deep-pocketed belief in the long-term resilience of U.S. equities, especially if policy loosens later this year.

THAT. Or they de-risked/sold at the bottom, only to see prices rebound 20% higher. They are now in a panic to meet their targets, so one way to catch up without deploying too much real cash is through options.

When people buy call options, the dealer on the other side is now short on that call option and has to buy the underlying stock or future to stay delta-hedged. With that happening over and over, you get this reflexive loop.

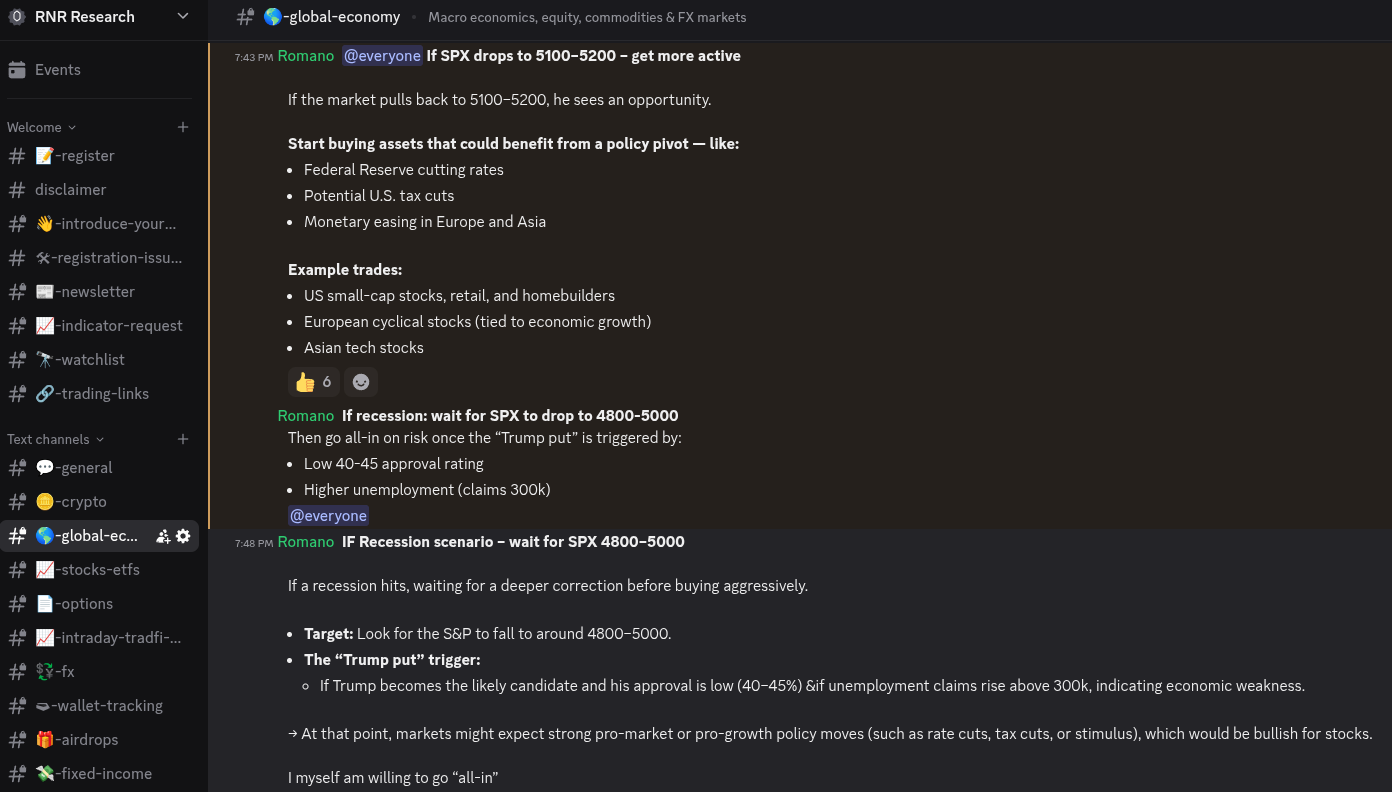

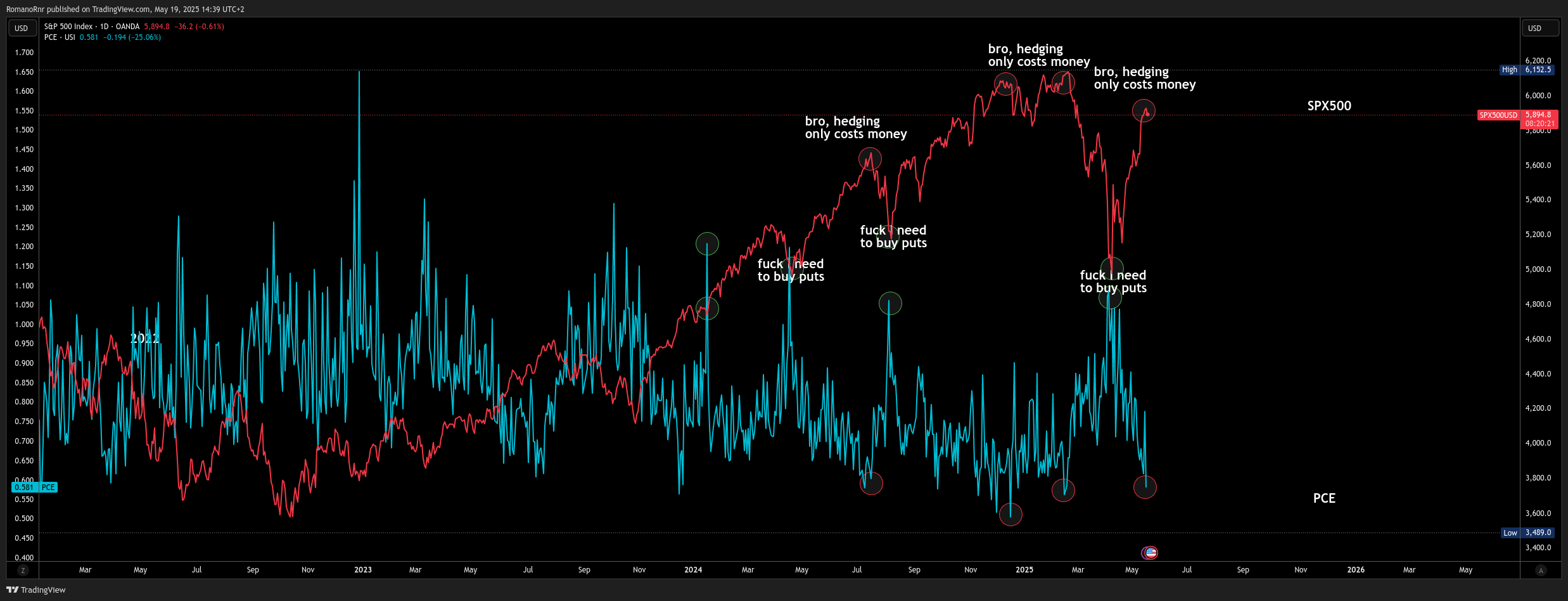

However, if you read this post back on April 6th or read our Discord, you probably bought the bottom when SPX500 fell into the 4800-5000 area.

And much more in the Discord.

Become a Premium member. Premium newsletters & Discord community access

Also, it's worth reading my previous article

On the other hand, in my eyes

Hedge when you can, not when the building is already on fire. I trimmed some of my stock positions last Friday.

I will either repurchase lower or different stocks later when I have more conviction. It's a bit dicey here. I can't help to thin that it's a bit dicey here

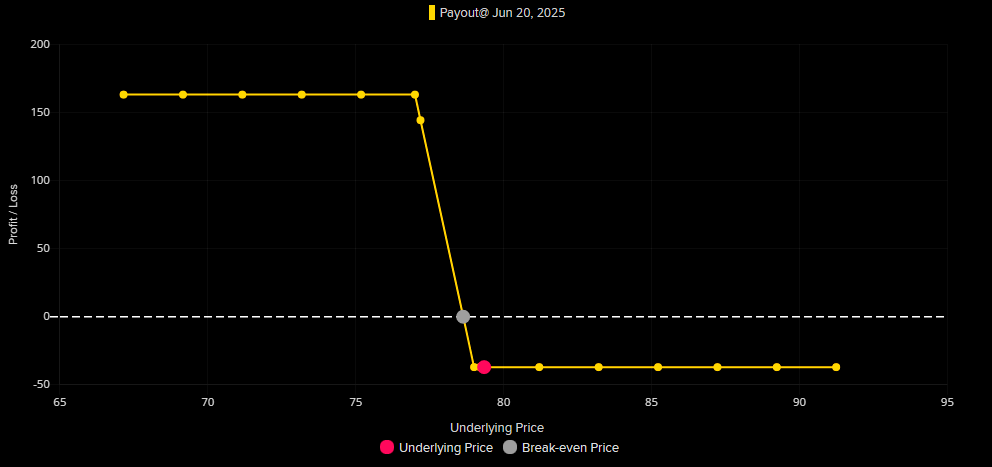

To hedge against credit risk, HYG June 79/77 put spread. I buy 79 puts and sell 77 puts expiring June 20th.

UBS’s Rebecca Cheong sees echoes of 2022’s bear-market rally in today’s move

Recent gains in Nasdaq and broader US indices have been steep and suspiciously so. Flows dominiatated by non-discretionary buyers. Systematic strategies alone contributed roughly $250 billion of buying pressure. Hedge funds were forced to chase performance as short positions got squeezed (like I mentioned earlier myself too)

According to Rebecca, there's been steady selling from retail and European real money. That divergence is a red flag.

This closely mirrors June - August 2022 rally, which ended with the S&P500 falling fresh cycle lows by October. While the macro setup is different, stronger growth and resilient corporate earnings, positioning looks stretched and the risk-reward for bulls is narrowing at these levels.

UBS Rebecca Trade idea: QQQ Put Spread Collor

- Sell the QQQ Sep 565 call (which is about +5% from current levels and year-to-date highs).

- Use those proceeds to buy a put spread: QQQ Sep 495-420 (covers a market correction from around -4% to -19%).

- Net cost: $5.21 (~1.01% of notional).

- Max payout ratio: 13.4x.

The trade caps your upside if QQQ rallies hard from here, but gives a convex payoff if we see a deeper correction into the fall. This might be true, but selling a call option can also go against you. There is a risk in taking this trade.

What about Bitcoin?!

Shitcoin play, Donald Trump coin (I do not believe in this token, I view it as worthless but I could see some positive reflexivity as degens try to rush into this again)

Stock trade

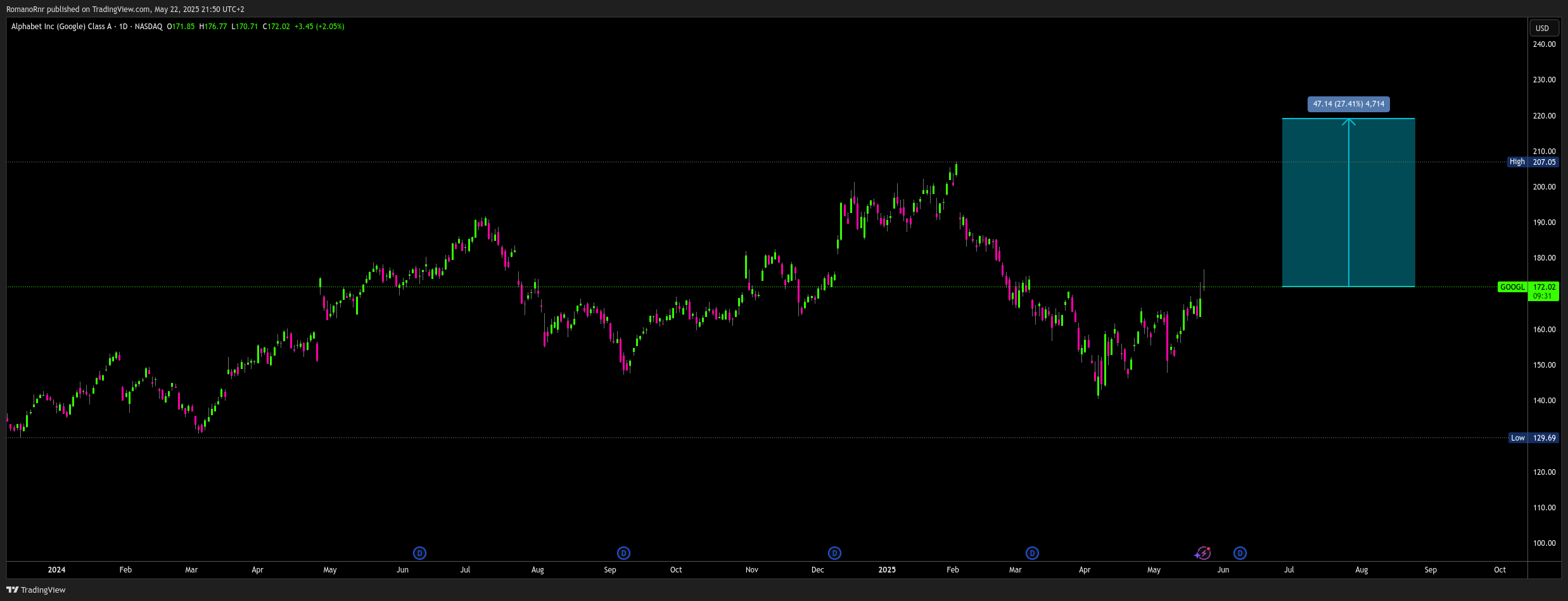

Personally, I am also buying Google shares. I could see it go to $219

Become a Premium member. Premium newsletters & Discord community access

Since Trump is imposing tariffs, here is the opposite - 50% discount forever on yearly subscription

Join Discord to get the full value out of the newsletter. There's no extra cost associated with Discord. Yes, options data, such as dark pools, options gamma, unusual flow, etc., are also included.

Besides crypto, if you cashed out a lot or are planning, I highly recommend the "stocks" and "fixed-income" channel on Discord for long-term plays and wealth-building.

That's where the real money is made with actual long-term stress-free trades.