Bank of Japan - YCC tweaks with greater flexibility

The dollar has been gaining strength against some other major currencies, partly due to positive economic data from the US and partly due to some weakness in the eurozone, after the European Central Bank meeting yesterday. However, one cause that has capped the dollar's upside is the lower USD/JPY exchange rate, which reflects the surprise decision by the Bank Of Japan yesterday to adjust its monetary policy framework.

So the Bank of Japan announced unexpectedly they would tweak their Yield Curve Control program. In this case, how they control their 10-year bonds yield curve; however, inflation forecasts for Japan are still hot, so not everyone decided to buy the Yen.

Yield Curve Control

Now you may wonder, what is Yield Curve Control (YCC)?

Yield Curve Control (YCC) is an unconventional monetary policy tool central banks use to influence interest rares across bonds with different maturities.

This differs from the conventional monetary policy tools, such as short-term rates, which the central bank usually manages. What it comes down to is YCC involves the central bank stepping into the bond market and buying to drive their prices up, which in turn affects the yield of these bonds.

As a quick reminder, if bond prices increase, the yield decreases. If the bond prices fall, the yield increases.

Conversely, when the central bank sells bonds, it increases the supply of those bonds, and the price goes down and drives up the yield. Through this process, a central bank can essentially set the yield on bonds with the desired maturity.

In this case, the Bank of Japan recently changed how they target the yield on their 10-year Japanese government bonds to prevent the yen from falling further down at the very least and preferably also push the yen higher relative to other currencies like the US dollar. By using YCC, the Bank of Japan is basically controlling the yen's value in the foreign exchange markets.

The effects of YCC are far-reaching and can have a major effect on everything from the value to the level of investments within the economy.

For example, when a central bank starts buying bonds to lower the yield on those bonds, they become less attractive to investors since they offer a lower return. So investors might start looking for other assets that could give them higher returns, like corporate bonds, stocks, or real estate, this shift can drive up prices in these other asset markets. It can stimulate more economic activity & investment.

In contrast, if the central bank increases yields on bonds (by selling bonds, for example), it makes those bonds more attractive and might draw investment away from other areas of the economy, potentially slowing economic activity.

Before continuing to read, subscribe to the premium newsletter. The premium package also includes full access to my Discord.

Anyways you can continue to read further. The article does NOT stop here.

What does the Bank Of Japan have to do with the US?

The Bank of Japan (BoJ) and the United States have a financial relationship because the BoJ is a massive buyer of US government bonds (a.k.a. Treasuries). This helps the US fund its debt, but it also means that what the BoJ does can greatly impact the US.

Now, the BoJ has been doing Yield Curve Control (YCC), where they buy or sell their own government bonds to control their interest rates. But let's say the BoJ stops buying its bonds via YCC and might also stop buying US bonds.

Why would they do that? If the yen's value is falling, the BoJ might want to step in and strengthen it. One way to do that is to buy up yen in the currency market. But to buy yen, they need US dollars.

And where can they get those dollars? You guessed it, by selling US government bonds. This means there would be more US bonds on the market, which can lower their prices and increase their yields (interest rates). It also means the BoJ would sell those bonds for dollars and then use those dollars to buy yen.

What's the effect of this? Well, when a lot of dollars are used to buy yen, the dollar's value could weaken. And when the dollar weakens, things priced in dollars, like oil or gold, become more expensive. That could lead to inflation - prices overall going up - which is usually not great for people's wallets.

Now, about that "leak" from the BoJ. If it's true they intentionally leaked their YCC plans, it might be a strategic move to shake things up in the market. Sometimes, market participants can get too comfy with their positions, and a bit of surprise news can catch them off guard, leading to quick changes in currency values and interest rates. Many people abuse the word, stoploss hunt but I think this was an actual stoploss hunt.

Are you a premium member of the newsletter but still didn't join Discord? (Also article does not end here)

Join Discord to get the full value out of the newsletter. There's no extra cost associated with Discord. It's included. All service ;)

Yes, options data such as dark pools, unusual flow, etc, are also included.

Why is the 10-year US treasury

For people who don't understand the importance of the 10-year US treasury

The 10-year US Treasury yield is important. When the yield on these goes up, it basically means the cost of borrowing money is getting more expensive. So, if you have a credit card, car loan, or mortgage, the interest you pay on that will likely increase.

Let's talk about the Bank of Japan (BoJ) and its potential impact. Japan holds a huge amount of US Treasuries, and any change in their behavior can send ripples across global markets.

Imagine the BoJ decided to sell off a big chunk of its Japanese Government Bonds (JGBs). This could freak out investors, and they might start selling their JGBs and US Treasuries, too, causing their prices to crash and yields (interest rates) to rise. Remember, when bond prices go down, their yields go up.

So if this mass sell-off happens, we could see the yield on the 10-year US Treasury jump above 4%, which is a significant increase. That signals to the market that borrowing costs are increasing and can make investors nervous about the economy.

Such a major shift can make the stock market jittery, too. If investors think the cost of borrowing is increasing, they might worry about companies' ability to borrow and invest, which can hurt their profits. So, they might start selling their stocks. That's why the S&P500 can drop significantly in response to such news.

The S&P500 fell 70 points after a report about the Bank of Japan was leaked, which spooked out the markets.

BOJ Tweaks YCC For "Greater Flexibility"

Now that was all yesterday; fast forward to today.

The Bank of Japan announced they will have a bit more "flexibility" with their Yield Curve Control. Which turns out isn't as hawkish as market participants feared yesterday.

S&P500 recovered 137 points today. As easy as it went up, as easy as it went up, and mostly outside of the trading hours.

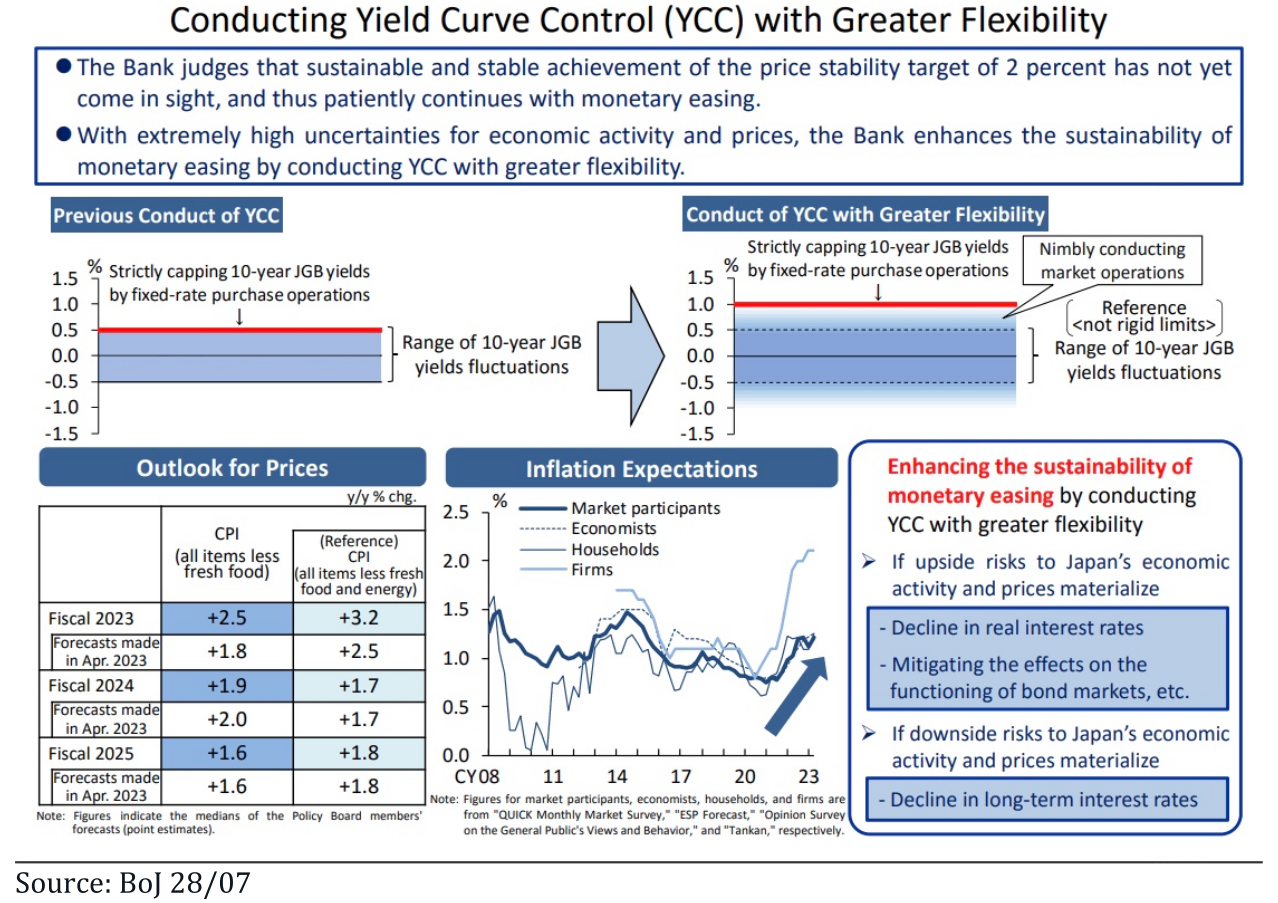

Before, they had this set target for their 10-year Japanese Government Bond (JGB) yields at 0%, but now, they're saying it's more of a guideline than a hard rule.

What's that mean? The BoJ is basically saying we're aiming for 0%, but if the yield ends up between -0.5% and +0.5%, that's fine.

Here's where it gets interesting. They're also willing to let it go as high as 1.0%. Imagine your friend saying, "Hey if you're running late, no worries. Just try to get here before 9".

If the yield of 10-year JGBs hits 1.0%, the BoJ will intervene and purchase all of them to prevent further increase in yield.

How will they do that? They will continue purchasing a significant amount of JGBs and adjust the purchase amount based on market conditions. This is quite a shift in their strategy, which has caused a stir in the markets and led to a spike in bond yields.

Here's how that looks visually

What the hell does this mean?

It's like the Bank of Japan throwing a party, and they're playing this game where they aim to toss a ring on a bottle. The bottle is their target yield for 10-year Japanese Government Bonds, which they ideally want at 0.5%. But they're saying, if they throw and it lands anywhere between 0.5% and 1.0%, that's still a win.

What it comes down to is the BOJ is too scared to go ahead with the policy normalization and shift its 10Y target to 1%, and instead, they're fine by doing a half-assed job to "test the waters" as mentioned by Zerohedge.

So this announcement is like the BOJ is testing the waters without fully diving in. It's like they're dipping their toes into the pool of policy normalization but not ready to do a cannonball just yet.

Or as Zerohedge puts it "The BOJ was too scared to go ahead with explicit policy normalization and shift its 10Y target to 1%, so it is instead doing a half-assed job by implicitly moving the target to test the waters, so to speak"

This may lead to JGB market volatility as everyone tries to figure out how far the BOJ will let things slide before they step in.

The rest of their announcement is basically a bunch of reasons they might get it wrong, like unpredictable overseas economies, commodity prices, and how firms set their wages and prices.

Implications

If the Bank of Japan (BOJ) introduces some conditions or caveats to its yield curve control (YCC) strategy, it may not have a large impact on the market immediately. That's because market participants would be uncertain about when the BOJ might step in and intervene to control bond yields.

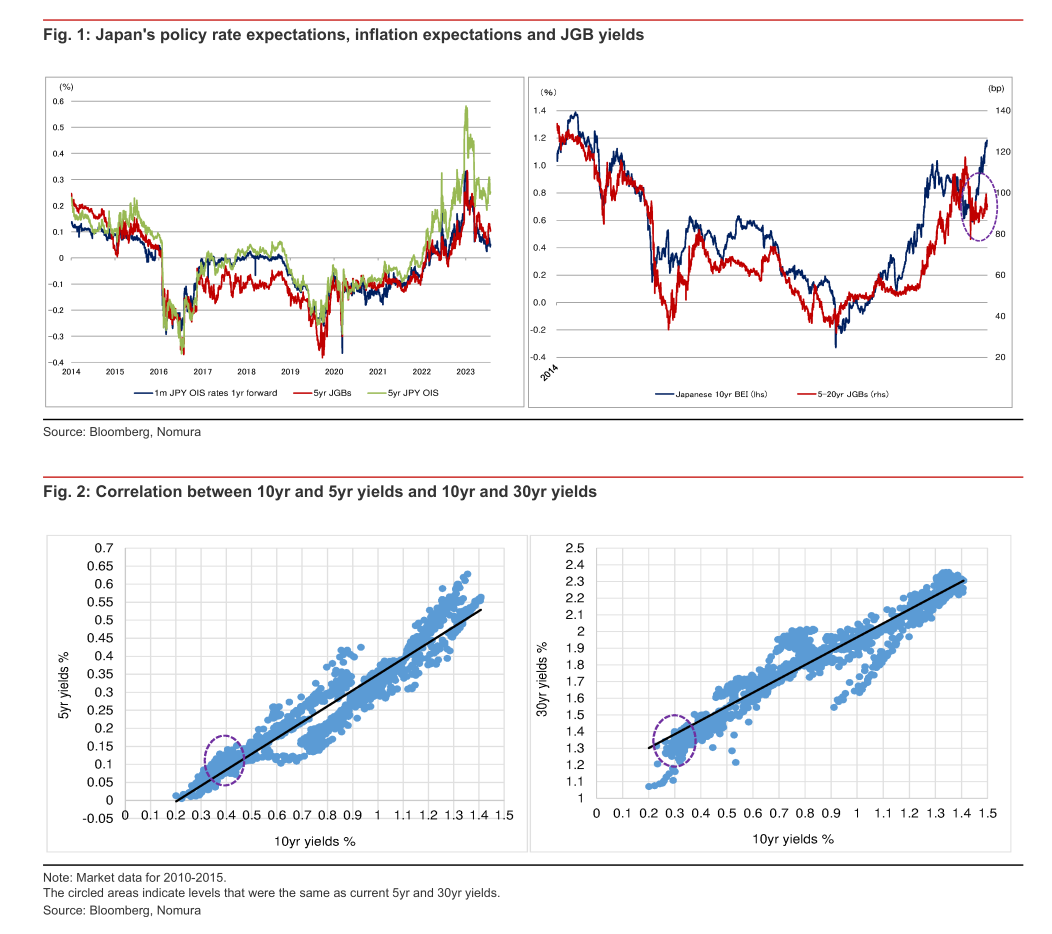

There would also be uncertainty about what might happen with bonds of different maturity lengths. If there's any change to YCC, market participants might start to think that the BOJ is preparing to increase short-term interest rates.

If wage negotiations in the spring suggest this is likely, the market might start pricing in an interest rate hike of about 0.10% to 0.20% over the coming year. If that happens, the yield on 5-year bonds could reach around 0.20%.

If 5-year bond yields rise to 0.20%, the 'fair' or expected yield for 10-year bonds could increase to between 0.60% and 0.70%.

However, this person writing the report thinks that even if the BOJ does increase the upper limit of the yield target to 0.75%, 10-year yields might only rise to between 0.50% and 0.70%.

The big question is what will happen with bonds with longer maturity dates. Initially, we might see the yield curve flatten as money starts flowing in from investors waiting for changes to YCC.

But right now, the super-long yield curve is a bit flat compared to where people expect inflation. If 5-year and 10-year yields don't rise as much as expected after the policy changes, then the super-long zone might face additional selling pressure, which could cause yields to increase.

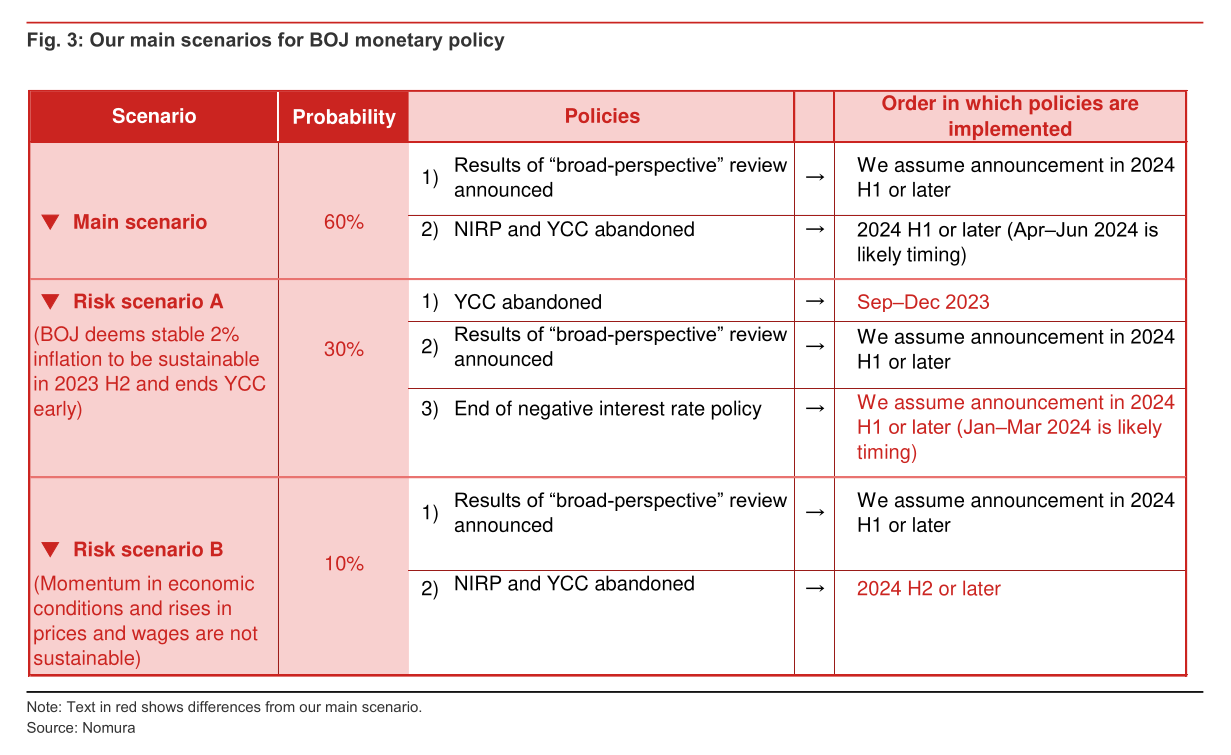

Main scenarios BOJ Monetary Policy

In the main scenario, most likely (about 60% chance), there won't be any big changes to Yield Curve Control (YCC) policy because today's announcements have already changed it.

According to Nomura, if wages increase in the spring of 2024 as they did this year, the Bank may eliminate YCC and the negative interest rate policy (NIRP) as soon as the first half of 2024. However, they do not anticipate any significant actions, such as quantitative tightening or a positive interest rate policy, during 2024.

There are two potential risk scenarios to consider. In the first scenario (A), there is a 30% likelihood that the Bank of Japan will determine that the Japanese economy is approaching stable 2% inflation faster than anticipated. In response, they may choose to discontinue Yield Curve Control (YCC) between September and December of 2023 without first announcing the outcome of a comprehensive policy review. However, even in this scenario, the end of the Negative Interest Rate Policy (NIRP) would likely be delayed until the first half of 2024, most likely occurring between January and March.

Risk scenario B is a 10% probability that the Bank of Japan will become more cautious about economic growth and inflation in the latter half of 2023. This may occur if there are unfavorable developments in other economies. If this happens, they predict that the withdrawal from YCC and NIRP will be postponed until the second half of 2024.

Bybit Trading competition

Join my Squad on Bybit for the trading competition

Join me at WSOT 2023!

https://www.bybit.com/en-US/wsot2023/squad-showdown?affiliate_id=6776&team_id=3927

ApeX DEX

Problems with KYC exchanges?

Consider ApeX DEX,, which is in my opinion, the best Decentralized Exchange there is

Instructions:

https://twitter.com/RNR_0/status/1652360705331347461

Signup: https://pro.apex.exchange/trade/BTC-USDC/register?affiliate_id=46&group_id=83

Ref code: 46

Are you looking for a Centralized exchange without KYC?

Try Bitget: https://partner.bitget.com/bg/Z9VWRV